- The Treasury Department could issue $700 billion in T-bills within weeks of a debt-ceiling deal, draining liquidity from markets Yahoo Finance

- Treasury to run low on cash by June 8 or 9 unless debt limit raised: Goldman Sachs Fox Business

- Goldman Sachs says the US has an extra 8 days before it runs out of money to pay its bills. That could buy it more time to negotiate the debt ceiling. msnNOW

- Goldman Sachs: Treasury Cash To Dip Below Minimum By June 8-9 – Invesco QQQ Trust, Series 1 (NASDAQ:QQQ), SPDR S&P 500 (ARCA:SPY) Benzinga

- US will run out of cash ‘in less than three weeks’ – latest updates The Telegraph

- View Full Coverage on Google News

Tag Archives: Treasury

Treasury Department Releases Guidance to Boost American Clean Energy Manufacturing – Treasury

- Treasury Department Releases Guidance to Boost American Clean Energy Manufacturing Treasury

- US Treasury takes middle road on solar panels ‘Made in the USA’ Reuters

- Tax credit for clean energy raises concern from some U.S. industries The Washington Post

- Made-in-USA trackers, solar panels, inverters and more can claim 10% ‘domestic content’ adder under certain rules Solar panels must have domestic solar cells to receive the full credit. Solar Power World

- Treasury Department releases guidance on solar domestic content pv magazine USA

- View Full Coverage on Google News

Treasury Yields Hold Steady, Maintain Declines After Fed Rate Call – The Wall Street Journal

- Treasury Yields Hold Steady, Maintain Declines After Fed Rate Call The Wall Street Journal

- Treasury bond data signals deficit is quickly increasing, says Damped Springs Advisors’ Andy Constan CNBC Television

- 2-year Treasury yield slides after Fed signals potential rate hike pause CNBC

- Signs of stress start to build in markets as debt ceiling deadline looms Washington Examiner

- Debt ceiling impasse: U.S. is only a few cycles away from using legal loopholes like minting $1 trillion platinum coin to avoid default – RBC Kitco NEWS

- View Full Coverage on Google News

Treasury Secretary Says Regulators Are ‘Looking For Solutions’ To Marijuana Banking Problem As Schumer Recommits To Addressing The Issue – Marijuana Moment

- Treasury Secretary Says Regulators Are ‘Looking For Solutions’ To Marijuana Banking Problem As Schumer Recommits To Addressing The Issue Marijuana Moment

- Feds Are ‘Weaponizing’ Bank Crisis to Kill Crypto: Rep. Tom Emmer Yahoo Finance

- US lawmaker suggests Signature’s collapse was tied to instability of crypto Cointelegraph

- Former FDIC Regulator: Friendliness Toward Crypto ‘Does Not Exist’ CoinDesk

- Janet Yellen Says Regulators Seeking Solutions For Marijuana Banking, Sen. Bennet Calls Cannabis More Sta Benzinga

- View Full Coverage on Google News

LIVE: Treasury Secretary Yellen testifies before the Senate on the 2024 fiscal year budget — 3/16/23 – CNBC Television

- LIVE: Treasury Secretary Yellen testifies before the Senate on the 2024 fiscal year budget — 3/16/23 CNBC Television

- Treasury Secretary Yellen to tell Congress ‘our banking system remains sound’ Yahoo Finance

- Yellen Says U.S. Banking System ‘Remains Sound’ Amid Market Turmoil The New York Times

- Bank Crisis: Yellen Speaks To Senate; First Republic Bank Ponders Sale| Investor’s Business Daily Investor’s Business Daily

- Watch live: Treasury Secretary Janet Yellen testifies on Biden’s 2024 budget proposal The Hill

- View Full Coverage on Google News

Former Treasury officials: Overhaul will ‘severely, irreversibly’ damage economy – The Times of Israel

- Former Treasury officials: Overhaul will ‘severely, irreversibly’ damage economy The Times of Israel

- Netanyahu’s planned judicial overhaul DIVIDES Israeli military | Latest English News | WION WION

- Lapid proposes constitution for Israel to extract itself from ‘terrible crisis’ The Times of Israel

- Former AG Mandelblit bashes overhaul: ‘Collision is preferable to a bad compromise’ The Times of Israel

- Former AG Mandelblit bashes overhaul: ‘Collision preferable to bad compromise’ The Times of Israel

- View Full Coverage on Google News

Exclusive: Top U.S. Treasury official to warn UAE, Turkey over sanctions evasion

WASHINGTON, Jan 28 (Reuters) – The U.S. Treasury Department’s top sanctions official on a trip to Turkey and the Middle East next week will warn countries and businesses that they could lose U.S. market access if they do business with entities subject to U.S. curbs as Washington cracks down on Russian attempts to evade sanctions imposed over its war in Ukraine.

Brian Nelson, undersecretary for terrorism and financial intelligence, will travel to Oman, the United Arab Emirates and Turkey from Jan. 29 to Feb. 3 and meet with government officials as well as businesses and financial institutions to reiterate that Washington will continue to aggressively enforce its sanctions, a Treasury spokesperson told Reuters.

“Individuals and institutions operating in permissive jurisdictions risk potentially losing access to U.S. markets on account of doing business with sanctioned entities or not conducting appropriate due diligence,” the spokesperson said.

While in the region, Nelson will discuss Treasury’s efforts to crack down on Russian efforts to evade sanctions and export controls imposed over its brutal war against Ukraine, Iran’s destabilizing activity in the region, illicit finance risks undermining economic growth, and foreign investment.

The trip marks the latest visit to Turkey by a senior Treasury official to discuss sanctions, following a string of warnings last year by Treasury and Commerce Department officials, as Washington ramped up pressure on Ankara to ensure enforcement of U.S. curbs on Russia.

STRAINED RELATIONS

Nelson’s trip coincides with a period of strained ties between the United States and Turkey as the two NATO allies disagree over a host of issues.

Most recently, Turkey’s refusal to green-light the NATO bids of Sweden and Finland has troubled Washington, while Ankara is frustrated that its request to buy F-16 fighter jets is increasingly linked to whether the two Nordic countries can join the alliance.

Nelson will visit Ankara, the Turkish capital, and financial hub Istanbul on Feb. 2-3. He will warn businesses and banks that they should avoid transactions related to potential dual-use technology transfers, which could ultimately be used by Russia’s military, the spokesperson said.

Dual-use items can have both commercial and military applications.

Washington and its allies have imposed several rounds of sanctions targeting Moscow since the invasion, which has killed and wounded thousands and reduced Ukrainian cities to rubble.

Turkey has condemned Russia’s invasion and sent armed drones to Ukraine. At the same time, it opposes Western sanctions on Russia and has close ties with both Moscow and Kyiv, its Black Sea neighbors.

It has also ramped up trade and tourism with Russia. Some Turkish firms have purchased or sought to buy Russian assets from Western partners pulling back due to the sanctions, while others maintain large assets in the country.

But Ankara has pledged that international sanctions will not be circumvented in Turkey.

Washington is also concerned about evasion of U.S. sanctions on Iran.

The United States last month imposed sanctions on prominent Turkish businessman Sitki Ayan and his network of firms, accusing him of acting as a facilitator for oil sales and money laundering on behalf of Iran’s Revolutionary Guard Corps.

While in the United Arab Emirates, Nelson will note the “poor sanctions compliance” in the country, the spokesperson said.

Washington has imposed a series of sanctions on United Arab Emirates-based companies over Iran-related sanctions evasion and on Thursday designated a UAE-based aviation firm over support to Russian mercenary company the Wagner Group, which is fighting in Ukraine.

(This story has been corrected to change headline to UAE, Turkey, not Middle East; adds Turkey in paragraph 1)

Reporting by Daphne Psaledakis and Humeyra Pamuk

Editing by Don Durfee and Leslie Adler

Our Standards: The Thomson Reuters Trust Principles.

US hits debt ceiling, prompting Treasury to take extraordinary measures

CNN

—

The US hit the debt ceiling set by Congress on Thursday, forcing the Treasury Department to start taking extraordinary measures to keep the government paying its bills and escalating pressure on Capitol Hill to avoid a catastrophic default.

The battle lines for the high-stakes fight have already been set. Hardline Republicans, who have enormous sway in the House because of the party’s slim majority, have demanded that lifting the borrowing cap be tied to spending reductions. The White House countered that it will not offer any concessions or negotiate on raising the debt ceiling. And with the solution to the debt ceiling drama squarely in lawmakers’ hands, fears are growing that the partisan brinksmanship could result in the nation defaulting on its debt for the first time ever – or coming dangerously close to doing so.

Treasury Secretary Janet Yellen wrote a letter to House Speaker Kevin McCarthy Thursday, informing him that the nation’s outstanding debt is at its statutory limit of $31.4 trillion and that the agency will implement extraordinary measures so it doesn’t default on its debt, which would have enormous consequences on the US economy, global financial stability and many Americans. She said the measures would expire on June 5.

This buys Congress some time – but how long the extraordinary measures can last is subject to “considerable uncertainty,” she wrote, stressing that it’s a challenge to forecast how many financial obligations the federal government must pay and how much revenue it will take in months into the future.

“I respectfully urge Congress to act promptly to protect the full faith and credit of the United States,” she wrote.

The announcement follows the warning Yellen sent last week about the approaching debt limit and the temporary Band-aid of the extraordinary measures.

But her missive has failed to spark bipartisan discussion so far. Instead, both Republicans and Democrats reaffirmed their rigid positions over the past week.

National Economic Council Director Brian Deese on Thursday repeatedly called on Congress to meet the United States’ obligations by raising the debt limit, warning against “economic chaos” that could ensue should Congress fail to do so.

“This is about economic stability versus economic chaos,” Deese told Kaitlan Collins on “CNN This Morning,” calling it Congress’ “basic, fundamental obligation.”

He added, “Even just the specter that the United States might not honor its obligations does damage to the economy.”

McCarthy must walk a fine line since any member can call for a motion to vacate the speaker’s chair, one of several concessions he made to gain the top post after 15 rounds of voting earlier this month.

For now, he is leaning on using the debt ceiling crisis to cut spending and balance the US budget. On Tuesday, McCarthy rejected Democratic calls for a clean debt ceiling increase without any conditions attached – something Congress has done time and again, including under then-President Donald Trump. The speaker told reporters on Capitol Hill that the Biden administration should begin to negotiate ahead of this summer, when the US could default.

“Why wouldn’t we sit down and change this behavior so that we would put ourselves on a more fiscally strong position?” McCarthy said.

President Joe Biden and McCarthy have not yet spoken Thursday about the debt limit, according to an official familiar with the dynamic.

Hard-right GOP Rep. Andy Biggs went even further in a tweet on Tuesday, writing, “We cannot raise the debt ceiling. Democrats have carelessly spent our taxpayer money and devalued our currency. They’ve made their bed, so they must lie in it.”

The White House on Wednesday blasted the Arizona Republican’s “stunning and unacceptable position” and once again rejected calls to reduce spending as part of a debt ceiling deal.

While there were no meetings with congressional leadership to announce at this time, White House press secretary Karine Jean-Pierre told reporters that the administration has been reaching out “to all members, from both sides of the aisle,” but, “there will not be any negotiations over the debt ceiling– we will not do that, it is their constitutional duty.”

The debt ceiling, which is the maximum amount the federal government is able to borrow to finance obligations that lawmakers and presidents have already approved, was last raised in December 2021. Created more than a century ago, it has become a way for Congress to restrict the growth of borrowing – turning it into a political football in recent decades.

Increasing the cap does not authorize new spending commitments.

Treasury will start using two extraordinary measures to allow it to temporarily continue financing the federal government’s operations, Yellen wrote on Thursday. They are mainly behind-the-scenes accounting maneuvers.

As part of the debt issuance suspension period, the agency will begin to sell existing investments and suspending reinvestments of the Civil Service Retirement and Disability Fund and the Postal Service Retiree Health Benefits Fund. Also, it will suspend the reinvestment of a government securities fund of the Federal Employees Retirement System Thrift Savings Plan.

These funds are invested in special-issue Treasury securities, which count against the debt limit. Treasury’s actions would reduce the amount of outstanding debt subject to the limit and temporarily allow it to continue paying the government’s bills on time and in full.

No federal retirees or employees will be affected, and the funds will be made whole once the impasse ends, Yellen wrote.

As part of his concessions, McCarthy promised to pass a proposal by the end of March telling Treasury which payments should be prioritized if the debt ceiling is breached, GOP Rep. Chip Roy confirmed to CNN last week.

Roy, a Texas Republican who is one of the key players in the standoff over McCarthy’s speakership, cautioned that the contours of the proposal are still being worked out, noting there are several different versions of a payment prioritization plan circulating inside the House GOP.

But choosing to pay one set of obligations over another could spark legal challenges, as well as political and ethical quandaries. For instance, lawmakers would have to decide which to pay first – Social Security monthly payments to the tens of millions of senior citizens and Americans with disabilities, salaries of federal workers and the military or the interest on US debt to a multitude of investors, many of them foreign.

Treasury Secretary Yellen predicts major inflation cooldown in 2023

New York

CNN

—

Treasury Secretary Janet Yellen is striking a cautiously optimistic tone about 2023, predicting a major inflation cooldown and stressing that a recession isn’t required to get prices back under control.

“I believe by the end of next year you will see much lower inflation, if there’s not an unanticipated shock,” Yellen told CBS’s “60 Minutes” in an interview that aired on Sunday.

Yellen cited plunging gas prices — AAA said Monday the national average is down by 52 cents per gallon in the past month — tumbling shipping costs and shortening delivery lags.

“I hope that it will be short-lived,” Yellen said of the current period of high inflation. “We learned a lot of lessons from the high inflation we experienced in the 1970s. And we’re all aware that it’s critically important that inflation be brought under control and not become endemic to our economy. And we’re making sure that won’t happen.”

Yellen, like many economists and even the Federal Reserve, has previously been overly optimistic about inflation. She admitted earlier this year that she was “wrong” about the path of inflation, telling CNN’s Wolf Blitzer in June that she “didn’t — at the time — fully understand” the “large shocks to the economy” that would come from Russia’s war in Ukraine.

The comments come after Friday’s hotter-than-expected wholesale inflation report, which showed producer prices increased in November at the slowest annual pace in 18 months.

The more closely watched consumer inflation report due out on Tuesday this week is expected to show a similar cooldown of consumer prices.

The Federal Reserve is widely expected to deliver a seventh-straight interest rate hike on Wednesday, though investors are betting the US central bank will slow the pace of rate increases from three-quarters of a point to half a point. The Fed’s aggressive rate hikes have driven up borrowing costs — credit card rates are at record highs — and raised fears of a recession.

Yellen conceded a recession is possible in the months ahead — though the former Fed chair emphasized that one isn’t required to tame inflation.

“There’s a risk of a recession,” Yellen said. “But it certainly isn’t, in my view, something that is necessary to bring inflation down.”

Like other Biden administration officials, Yellen argued the economy is in the midst of a healthy transition from blockbuster growth to something more sustainable.

“We had a very rapid recovery from the pandemic. Economic growth was very high,” Yellen said. “To bring inflation down and because almost anyone who wants a job has a job, growth has to slow.”

Yellen said the US economy is at or near full employment, meaning it’s “not necessary” for rapid growth to get people back to work.

The Treasury secretary said she tries to instill a sense of compassion and urgency into policymaking by stressing to her staff that real people are suffering.

Yellen recalled how in 2009 when millions of people were out of work in the middle of the Great Recession, she reminded her staff at the San Francisco Federal Reserve, where she was president from 2004-2010, that there are real people behind labor market statistics and economists need to worry about their wellbeing.

“I think I said, ‘They’re f***people,’” Yellen said. “I wanted people that worked for me to take seriously the harm and misery that was being experienced by all too many Americans.”

Drop in 10-Year Treasury Yield & Mortgage Rates Is Just Another Bear-Market Rally. Longer Uptrend in Yields Is Intact, with Higher Highs and Higher Lows

“Nothing goes to heck in a straight line.” That’s how functional markets adjust to a new reality: Higher inflation, higher rates.

By Wolf Richter for WOLF STREET.

There has been a lot of discussion and handwringing and Fed-pivot fantasizing about the drop of the 10-year Treasury yield from 4.25% at the end of October to 3.51% at the close on Friday. That’s a 74-basis-point drop. In percentage terms, the yield dropped by 17%. A drop in yield means a rise in prices of these securities. So this drop in yields represents a rally in prices.

But here is the thing: During the summer bear-market rally, the 10-year yield dropped by 25%, from 3.49% to 2.60%. Before then, there were a few smaller bear-market rallies. But the biggest bear-market rally during this bond bear market was from April 2021 to August 2021, when the yield dropped by 30%, from 1.70% to 1.19%.

The 10-year yield closed at 0.52% on August 4, 2020, which marked the end of the 39-year bond bull market. Since then, the 10-year yield has risen sharply, with big surges followed by smaller retracements, followed by big surges, followed by smaller retracements, etc., adhering to the Wolf Street dictum that “Nothing Goes to Heck in a Straight Line.” The 10-year yield, as it went up, marked higher highs and higher lows each time. And the current bear-market rally fits in nicely, and they yield could drop further, and it would still fit in nicely:

Back in August 2020, the 10-year yield hit the low of 0.52% – after months of widespread propaganda by bond- and hedge-fund kings, queens, and gurus in the social media, on CNBC, and Bloomberg that the Fed would push interest rates into the negative, just like central banks had done in Europe and Japan.

This was an effort to manipulate people into buying a 10-year security with nearly no yield, thereby driving yields down further, and prices up further, to make said kings, queens, and gurus a lot of money.

Whoever ended up buying 10-year maturities at the time got a really bad deal because that marked the bottom of the 39-year bond bull market, during which the 10-year yield had descended from 15.8% in September 1981 to 0.52% in August 2020 – and not in a straight line – on declining inflation and declining interest rates, with some big wobbles in between, and since 2008, fueled by money-printing and interest rate repression.

But now we have the fastest Fed rate hikes in 40 years, and the Fed’s fastest QT ever, having unwound $381 billion in six months.

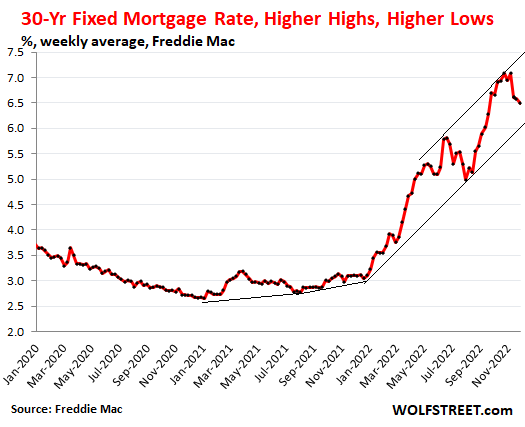

Mortgage rates followed a similar pattern. The 30-year fixed mortgage rate began the rise in early 2021, from a low of 2.65%. But also not in a straight line. By April 2021, it had reached 3.18%, and then it retraced to 2.78% by June 2021. By the end of December 2021, it was back at 3.11%.

And then as the Fed ended QE, and then raised rates, and then embarked on QT, mortgage rates surged – interrupted by big bear-market rallies, most notably the summer bear-market rally when the average 30-year fixed mortgage rate dropped by 14%, from 5.8% to 4.99%, only to surge again to 7.08% at the end of October. As of Freddie Mac’s index released on December 1, the rate has retraced some of that surge, dropping to 6.49%. This represents an 8.3% drop in the average mortgage rates.

Since early 2021, we still have an unbroken uptrend of the 30-year fixed mortgage rate, marked by higher highs and higher lows, and a further drop would still fit in nicely into the overall uptrend:

The trend is your friend. There has been a huge amount of Fed-pivot mongering and rate-cut mongering and the-Fed-will-restart-QE-soon mongering, etc. All this is part of the normal game of how markets are adjusting to new realities, with each side pushing in its own direction, thereby pushing markets up and down in a volatile manner. But this is how functional markets adjust to new realities. Adjustments don’t happen all at once. And if they do, it’s a truly spooky affair. And they don’t adjust in predictable straight lines either. They go about it over time in their rough and tumble way, but ultimately, they get there.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()