Junk bonds still in la-la-land as investors chase yield – risks be damned.

By Wolf Richter for WOLF STREET.

The bond market settled down on Friday. And that was a good thing for the crybabies on Wall Street that had started to hyperventilate on Thursday, when the Treasury 10-year yield, after rising for months, and accelerating over the past two weeks, had spiked to 1.52%, having tripled since August.

By Thursday, all kinds of complex leveraged trades had been coming apart, and forced selling had set in. By historical standards, and given the inflation pressures now underway, those yields even on Thursday were still astonishingly low. But Wall Street had a cow, for sure.

On Friday, the Treasury 10-year yield dropped 8 basis points, part of the 14-basis-point spike on Thursday, and closed at 1.44%, still higher than where it had been a year ago on February 21, 2020.

Yields rise because bond prices fall, producing a world of hurt – reflected in bond funds focused on long-dated Treasury bonds, such as the iShares 20 Plus Year Treasury Bond ETF [TLT]; its price is down about 16% from early August, after the 3.3% relief-bounce on Friday.

The Fed approves.

The governors of the Federal Reserve have been speaking in one voice on the rise in Treasury yields: It’s a good sign, a sign of rising inflation expectations and a sign of economic growth. That is the mantra they keep repeating.

Fed Chair Jerome Powell called the surge in Treasury yields “a statement of confidence.”

Kansas City Fed president Esther George said on Thursday: “Much of this increase likely reflects growing optimism in the strength of the recovery and could be viewed as an encouraging sign of increasing growth expectations.”

St. Louis Fed president James Bullard, one of the most passionate doves, said on Thursday: “With growth prospects improving and inflation expectations rising, the concordant rise in the 10-year Treasury yield is appropriate.” Investors demanding higher yields to offset higher inflation expectations “would be a welcome development.”

They’re all singing from the same page: They’re dovish on QE and low rates. But they’re going to let long-term rates rise, which is starting to tamp down on some of the ridiculous froth in the financial markets and the housing market.

Those Fed pronouncements on Thursday morning in support of higher long-term yields – when the markets were clamoring for the opposite, more QE but focused on long maturities to bring down long-term yields – probably also helped unnerving Wall Street.

But on Friday, the mini-panic settled back down, and that’s good because a real panic could change the Fed’s attitude.

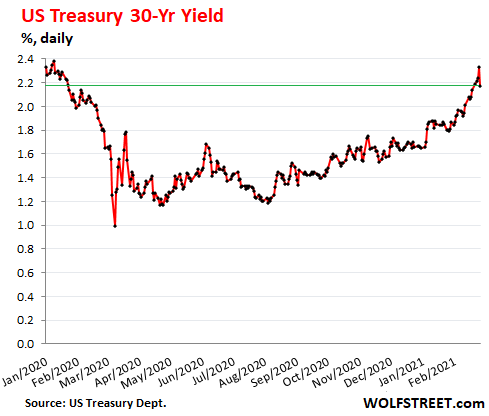

The 30-year yield on Friday dropped by 16 basis points, to 2.17%, erasing the jump of the prior three days. It’s now where it had been on January 23 last year:

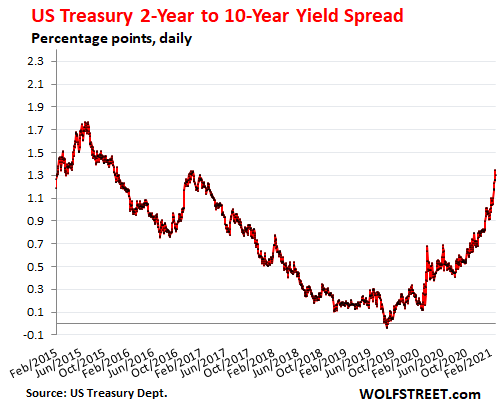

The yield curve as measured by the difference between the 2-year yield and the 10-year yield had been steepening sharply, with the 2-year yield glued in place, and with the 10-year yield taking off. On Friday, the spread between the two narrowed to 1.30 percentage points, from Thursday’s 1.35 percentage points, still making for the steepest yield curve by this measure since December 2016.

In August 2019, the yield curve by this measure briefly “inverted” when the 10-year yield dropped below the 2-year yield, turning the spread negative. The yield curve has steepened ever since in a very rough-and-tumble manner:

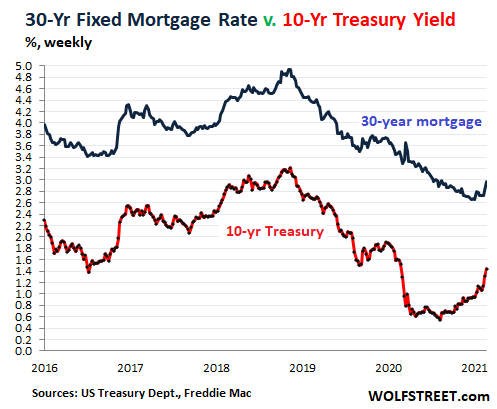

And mortgage rates finally started to follow.

The average 30-year fixed mortgage rate rose to 2.97% during the week ended Wednesday, as reported by Freddie Mac on Thursday. This does not yet include the moves on Thursday and Friday.

The 30-year mortgage rate normally tracks the 10-year yield fairly closely. But in 2020, they disconnected. When the 10-year yield started rising in August, the mortgage market just ignored it, and mortgage rates continued dropping from record low to record low until early January, whipping the housing market into super froth.

But then in early January, mortgage rates started climbing and have now risen by 32 basis points in less than two months — though they remain historically low.

Note the disconnect in 2020 between the weekly Treasury 10-year yield (red) and Freddy Mac’s weekly measure of the average 30-year fixed mortgage rate (blue):

In this incredibly frothy and overpriced bubble housing market, higher mortgage rates are eventually going to cause some second thoughts.

And that too appears to be smiled upon approvingly by the Fed. They’re not blind. They see what is going on in the housing market – what risks are piling up with this type of house price inflation. They just cannot say it out loud. But they can let long-term yields rise.

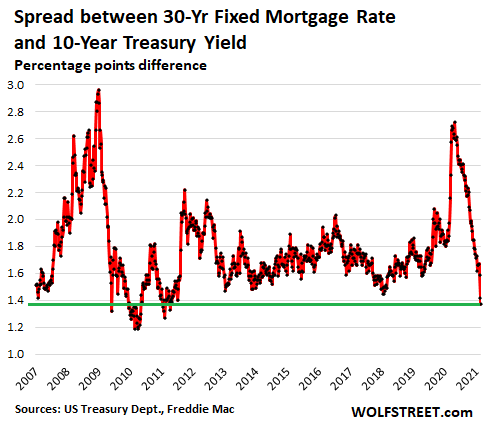

Mortgage rates have some catching up to do. The spread between the average 30-year fixed mortgage rate and the 10-year yield has been narrowing steadily since the March craziness, and at 1.37 percentage points, is the narrowest since April 2011.

The spread always reverts from extreme lows, such as this, toward the mean. It can do so in two ways, by mortgage rates rising faster than Treasury yields, or by mortgage rates falling more slowly than Treasury yields.

High-grade corporate bonds starting to feel the pain.

Yields have risen and prices have fallen across the investment grade spectrum of corporate bonds, though yields remain very low by historic measures:

AA-rated bonds yielded on average 1.81%, according to the ICE BofA AA US Corporate Index, up from the record low of 1.33% in early August (my cheat sheet for corporate bond ratings).

BBB-rated Bonds – just above junk bonds – came out of their torpor over the past two months, with the average yield climbing to 2.39%, according to the ICE BofA BBB US Corporate Index, up from the record low of 2.06% at the end of December. They, like mortgage rates had continued to fall through 2020, despite rising Treasury yields.

Junk bonds still in la-la-land, with yields near record lows.

BB-rated bonds – the highest-rated junk bonds – came out their torpor just over the past two weeks, and the average yield rose to 3.45%, according to the ICE BofA AA US Corporate Index, up from the record low in mid-February of 3.20%.

The average yield of CCC-rated bonds – at the riskiest end of the junk spectrum with a considerable chance of default – has barely ticked up from record lows in mid-February (7.17%) and now hovers at 7.27%. In March, the yield had shot up to 20%. During the Financial Crisis, it had spiked north of 40%.

The Fed smiles upon its creation.

The fact that the highest risk bonds still sport yields that are near record lows is a soothing sign for the Fed. It means that financial conditions are still extremely easy. All kinds of high-risk companies with crushed revenues and huge losses – think cruise lines with near zero revenues and losses out the wazoo – can fund their cash-burn by issuing large amounts of new bonds to over-eager yield-chasing investors, no problem.

So far this year, companies issued $84 billion in junk bonds, according to Bloomberg. At this pace, the first quarter will be the biggest in junk bond issuance ever. There is huge demand for junk bonds due to their higher yields – risks be damned. The yield chase is on in full force. And the overall junk bond market has ballooned to over $1.6 trillion.

For the Fed, this is one of many signs that credit markets are still super-frothy, even if Treasury yields have risen from record lows to still historically low levels. While it vowed to continue QE and not raise rates for a “while,” it’s also telling the markets in a unified voice that rising long term Treasury yields are a sign that the Fed’s monetary policies are working as intended. And those higher long-term yields are taking some of the froth off the markets, including eventually the housing market – and I don’t think that this is an unintentional side effect.

From crisis to crisis, and even when there’s no crisis. Read… Fed’s QE: Assets Hit $7.6 Trillion. Long-Term Treasury Yields Spike Nevertheless, Wall Street Crybabies Squeal for More QE

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()