- United Airlines passenger says people were ‘praying’ on flight that plunged to within 800 feet of Pacific Fox Business

- NTSB to investigate San Francisco-bound United Airlines 777 after nosediving from Maui’s Kahului Airport toward Pacific Ocean WPVI-TV

- United pilots retrained after plane nosedived to just 775 feet above Pacific Ocean, airline says New York Post

- United Airlines Passenger Recounts Moment Plane Almost Crashed Into Pacific Ocean on Its Way to SFO NBC Bay Area

- Off The News: A ‘very serious’ descent during flight Honolulu Star-Advertiser

- View Full Coverage on Google News

Tag Archives: plunged

DocuSign Stock Plunged on Soft Outlook

Shares of

DocuSign Inc.

DOCU -20.10%

fell 20% Friday, wiping out the stock’s pandemic-era gains, after the e-signature software maker released softer-than-expected guidance for its fiscal 2023.

The company said Thursday evening that it expects full-year revenue to be between $2.47 billion to $2.48 billion, lower than the $2.61 billion that analysts surveyed by FactSet had been expecting.

The company also said it expects subscription revenue growth to slow, forecasting a range of $2.39 billion to $2.41 billion.

Billings, which reflect new-customer sales, subscription renewals and add-on sales for existing customers, are expected to come in between $2.71 billion and $2.73 billion, also a substantial slowdown from 2021.

The company warned in December that its growth would likely be hampered as people returned to more normalized working and buying patterns as the pandemic faded. The company said at the time that it would invest in increasing its sales efforts, increase marketing spending and spend more on product innovation.

DocuSign fits into a category of companies that made working from home easier to manage and benefitted as businesses adapted to remote and paperless environments. But its business has taken a hit as the pandemic fades and more offices begin calling their employees back to in-person work.

Its share price tripled in 2020, but fell almost 32% last year. Shares closed Friday at $75.01 and are down 51% so far this year.

DocuSign CEO Dan Springer discussed the e-signature company in March 2019.

Photo:

David Paul Morris/Bloomberg News

Despite the forecasted slowdown, Chief Executive Officer

Dan Springer

said the company’s digital-signature business will continue to grow.

“As people begin to return to the office, they are not returning to paper,” Mr. Springer said. “eSignature and the broader Agreement Cloud will only continue to gain prominence in the evolving Anywhere Economy.”

The worse-than-expected guidance came even as DocuSign topped analysts’ expectations for revenue in the fiscal fourth quarter. The company reported adjusted earnings of 48 cents a share on revenue of $580.8 million. Analysts were expecting adjusted earnings of 48 cents a share on revenue of $562 million.

DocuSign also said its board has authorized it to buy back $200 million worth of shares. At the same time, the company said Chief Revenue Officer Loren Alhadeff intends to resign.

Still, analysts at Oppenheimer on Friday removed their $250 price target on the stock and downgraded DocuSign to perform from outperform.

“The guidance shows that the challenges seen then with respect to sales execution and resetting post-Covid consumption patterns remain near- to medium-term headwinds,” the analysts wrote.

Write to Will Feuer at will.feuer@wsj.com

Copyright ©2022 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

Deaths of mom and son, 2, who plunged from third level of Petco Park was murder-suicide, cops say

‘But she was happy’: Family of mom who plunged to her death with two-year-old son from third level of San Diego’s Petco Park disputes cops’ finding that it was murder-suicide

- San Diego cops say deaths of Raquel Wilkins and son Denzel was murder-suicide

- Raquel, 40, and Denzel, 2, plunged to their deaths on September 25 last year

- Their deaths occurred as thousands of baseball fans were heading inside for a Padres MLB game at Petco Park

- Police said on Tuesday that after combing video footage and obtaining evidence related to the case, they determined that Wilkins’ cause of death was suicide, and her son’s was homicide

- But a lawyer for the family disputes the findings, alleging a cover-up by the city

- Dan Gilleon said the deaths were a tragic accident and multiple witnesses said she appeared ‘happy’ and was laughing before falling over the railing

The death of a mother and her two-year-old son who fell from San Diego’s Petco Park has been ruled a murder-suicide – but a lawyer for the family disputes the finding and says that the city is trying to shield itself from a lawsuit.

Raquel Wilkins, 40, a regional lead at California Virtue Academy and a former chemistry teacher at Durant High School and her son Denzel Browning-Wilkins, 20, plunged to their deaths from the third level of the baseball stadium at 4.11pm on September 25 last year.

Their deaths occurred as thousands of baseball fans were heading inside for a Padres MLB game.

Police said on Wednesday that after combing video footage and obtaining evidence related to the case, they determined that Wilkins’ cause of death was suicide, and her son’s was homicide. They have refused to release the evidence they obtained during the investigation to Wilkins’ family.

Dan Gilleon, an attorney for Wilkins’ family, has disputed the findings and said the deaths were a tragic accident and the city is trying to shield itself from being sued. Multiple witnesses have said she appeared ‘happy’ and was laughing before falling over the railing.

San Diego police have today classified the death of Raquel Wilkins (right) as a suicide, and the death of her two-year-old son Denzel (left) as a homicide

However, Dan Gilleon, an attorney for Wilkins’ family, has disputed the findings about Raquel and Denzel (pictured), alleging the murder-suicide classification is a cover-up, citing witnesses who described the 40-year-old as ‘happy’ on the day

In a text sent to The Associated Press, Gilleon said: ‘The city doesn’t want to explain why it concluded that a young mother would kill her only child at an event where witnesses said she was happy.

‘To me, the city is acting like any other defendant in a lawsuit: blame the victim, especially if they are not able to defend themselves.’

A man, who did not want to be identified, told the San Diego Union-Tribune at the time that his wife witnessed the tragedy and saw the toddler appear to fall first and his mother tumble over while trying to grab him.

Another witness told Fox News that both victims and a man were seated at the table next to her on the concourse of the stadium. She said that at one point, the man was standing next to the woman who was ‘jumping on the bench of the table closest to the railing, holding the baby in her arms’.

‘She seemed happy, laughing. She lost her balance and fell off the bench. I remarked to my son, ‘Oh my gosh, she almost fell.’

About 30 seconds to a minute later, Wilkins and her son plunged to their deaths after she lost her balance, according to the witness.

In a statement released back in September, the San Diego Padres said: ‘We are deeply saddened by the loss of life at Petco Park last evening. Our thoughts and prayers are with the family of those involved.’

The mother and son plunged to their deaths from the third level of the baseball stadium at 4.11pm on September 25 last year

In a statement issued by the San Diego Police Department said: ‘The detectives conducted a thorough and comprehensive investigation that included dozens of interviews, reviewing of available video footage, and collecting background information to determine what led to the deaths.’

The determinations were made in consultation with the San Diego County Medical Examiner, police said.

Why Cryptocurrencies Like Ethereum, Cardano, Shiba Inu, and Cosmos Plunged Today

What happened

The weekend continues to be a rough time for cryptocurrency holders. The stock market closes on Saturday and Sunday, but digital assets trade 24 hours, 7 days a week and Saturday has repeatedly been a down day for the cryptocurrency market over the past month.

There were drops across the cryptocurrency industry today but a few were more notable than others. Ethereum (CRYPTO:ETH) continues its slide, falling 5.1% in the last 24 hours as of 4:20 p.m. ET. The value of Ethereum has fallen 17% in the past week and 31% over the past 30 days, hitting the dreaded $3,000 price in afternoon trading today before recovering slightly.

Cardano (CRYPTO:ADA) fell 5.5% over the last 24 hours, Shiba Inu (CRYPTO:SHIB) is down 5.9%, and Cosmos (CRYPTO:ATOM) is down 13.7%. These are all known as altcoins and are typically more volatile than their larger crypto rivals, but these are big drops no matter how you look at it.

Image source: Getty Images.

So what

The sharp drop in cryptocurrency values started at about 11:00 a.m. ET and lasted for about two hours before stabilizing. Given the fact that it’s a weekend and there’s not a lot of news and cryptocurrencies were selling off across the board, this looks like a short-term trading phenomenon.

One factor to look at is the number of digital asset trading accounts being liquidated due to hitting margin limits, which is another way of saying an exchange forced a cryptocurrency holder to sell in order to make sure debts are paid off. According to Coinglass.com, $273 million of crypto accounts that they follow were liquidated over the last 24 hours. Surprisingly, $71.9 million of that was in Ethereum with just $53.6 million in Bitcoin (CRYPTO:BTC) even though Bitcoin has a much larger market cap. These forced sales may be why Ethereum dropped so much, and related cryptocurrencies that are also building utility followed suit.

Liquidation data can tell us a lot about the short-term moves of cryptocurrencies. For example, on December 2 and 3 of 2021, there were $636 million and $1.58 billion of long (a position that’s profitable if an asset’s price goes up) positions liquidated, causing the market to tumble. Today, only $211 million of positions have been liquidated so far, but in the last three days $1.24 billion of long positions have been liquidated, so there’s definitely downward pressure.

All investment markets are trying to work through confusing economic data right now as well. Omicron is sweeping across the world, potentially negatively impacting the economy. We are also seeing inflation and the Federal Reserve in the U.S. talking about raising rates in 2022, which could also slow the economy. These fears have hurt growth stocks recently and cryptocurrencies are generally correlated with growth stocks, so they’re falling as well.

Now what

Volatility is common in cryptocurrencies but for most of the last two years, the trend in prices was going up. Now, we’re seeing volatility work against investors and prices are falling quickly.

The drop may last for a while as speculators and leveraged traders are pushed out of the market. But there are hundreds of millions of dollars being invested in building real utility for cryptocurrencies whether that’s in finance, fashion, payments, or other areas, and long-term that’s why I’m bullish on the industry. That said, it’s going to be a bumpy ride and I’m prepared for prices to drop further before they get better.

This article represents the opinion of the writer, who may disagree with the “official” recommendation position of a Motley Fool premium advisory service. We’re motley! Questioning an investing thesis — even one of our own — helps us all think critically about investing and make decisions that help us become smarter, happier, and richer.

After Months of Daylight, Antarctica Is About to Be Plunged Into 2 Minutes of Night

The Sun hasn’t set in Antarctica since October. Earth’s southernmost continent is currently experiencing a long summer’s day, one that stretches from mid-October until early April.

But on Saturday December 4, darkness will sweep across the ice of West Antarctica. The Moon will pass directly in front of the Sun, blocking its light and producing a total solar eclipse.

The path of totality crosses the Argentine, British and Chilean Antarctic Territories (which consist of overlapping regions), as well as the unclaimed territory known as Marie Byrd Land. Areas along the path will experience almost 2 minutes of darkness in the otherwise months-long stretch of daylight.

Meanwhile, the southern tips of South America, Africa, Australia and New Zealand will see a fairly minor partial eclipse. For South America and Africa, the eclipse will be in the early morning; for Australia and New Zealand it will happen as the Sun is setting.

The Moon’s goodnight kiss

As the Sun sinks towards the horizon the Moon will appear to kiss the top-left of the Sun. Of all Australia’s capital cities, Hobart will see the largest eclipse, but even so only 11 percent of the Sun’s area will be covered. For Melbourne, this drops to just 2 percent, while in Canberra it’s hardly visible – the Sun is crossing the horizon as a tiny eclipse occurs.

It’s a similar situation in New Zealand. Invercargill will see 4 percent of the Sun obscured by the Moon, with the Moon passing by the Sun’s left side. But move further north to Queenstown and the eclipse is barely visible for the setting Sun.

In fact, if you weren’t aware of it, you wouldn’t even know the eclipse was happening. It’s not until about 80 percent or more of the Sun is obscured before we notice any change in daylight.

Star light, star bright

Solar eclipses are one astronomical event that require special care to observe. Most importantly, never look at the Sun directly – even when it’s low on the horizon.

Be sure to protect your eyes by using specially designed eclipse glasses. These glasses also allow you to see any sunspots that might be active. The Sun is currently moving from a quiet phase to an active one, as part of a cycle that repeats every 11 years. You can check websites such as Spaceweather to see what’s happening on the Sun’s surface right now.

Normally, the projection method is a great way to observe solar eclipses. This involves making a small hole in the bottom of a plastic cup or piece of cardboard. Then, with your back to the Sun, hold the cup so the sunlight passes through the hole onto a flat surface such as a piece of paper or a wall, projecting an image of the Sun on the surface.

But because this is such a minor eclipse and it will happen at sunset in eastern Australia, it may be hard to focus the Sun’s image in this way.

The rarity of totality

Solar eclipses are relatively rare experiences, because the Moon’s orbit is tilted by 5 degrees relative to Earth’s orbit around the Sun, so they don’t quite move in the same plane. However, roughly every six months the orbits align to produce a pair of eclipses – a lunar eclipse at Full Moon, followed by a solar eclipse at New Moon (as we are experiencing now), or vice versa.

Lunar eclipses are seen by more people because everyone on the night side of the Earth during a lunar eclipse will see the event. Solar eclipses happen just as often, but they are seen by far fewer people because the shadow created by the Moon passing in front of the Sun covers a much smaller fraction of the Earth.

Furthermore, partial solar eclipses are difficult to observe and they pale in comparison to the experience of a total solar eclipse. While total solar eclipses happen roughly every 18 months being able to see totality is rarer still.

The Moon’s shadow as it crosses the Earth is only 100-260 km (60-160 miles) wide, and you have to be located within that narrow path to see the totally eclipsed Sun. This is why eclipse-chasers travel the world to be in the right place at the right time. But when totality occurs in a remote location like Antarctica it’ll be mainly the penguins who get to see it.

The next total solar eclipse visible from Australia will happen in April 2023. The band of totality will just clip Australia near Exmouth at the tip of the North West Cape in Western Australia.

But many more Aussies and New Zealanders will get to see a total solar eclipse on July 22 2028. Totality will stretch across Australia, from the top of WA down through New South Wales, passing directly over Sydney. It will also cross the South Island of New Zealand, passing through Queenstown and Dunedin.![]()

Tanya Hill, Honorary Fellow of the University of Melbourne and Senior Curator (Astronomy), Museums Victoria.

This article is republished from The Conversation under a Creative Commons license. Read the original article.

Dollar’s Purchasing Power Plunged at Constant Speed

Now it’s new vehicles, restaurants, energy. Game of Whac-A-Mole as some price spikes slow while others begin. But it’s a lot worse than it seems.

By Wolf Richter for WOLF STREET.

The Consumer Price Index (CPI) jumped 0.5% in July from June, after having jumped 0.9% in June, 0.6% in May, for a three-month annualized rate – the three-month momentum – of 8.1%. Year-over-year, CPI jumped 5.4%, same pace as in June, and the fastest since June 2008 (5.6%), all of which had been the fastest since January 1991, according to data released by the Bureau of Labor Statistics today.

The CPI without the volatile food and energy components (“core CPI”) rose by 0.3% for the month and by 4.3% year-over-year.

The CPI measures the loss of the purchasing power – well, part of the loss of the purchasing power, as we’ll see in a moment – of the consumer dollar and thereby the purchasing power of labor. In July, this purchasing power dropped another 0.5% for the month, and for the past three months annualized, it dropped by 8.6% – “Honey, where did my big raise go?”

CPI vastly understates one-third of its components: housing cost.

Homeownership costs and rents account for 31% of CPI. These are the largest categories, the most important categories, but they hardly budged despite exploding housing costs and thereby suppressed the CPI.

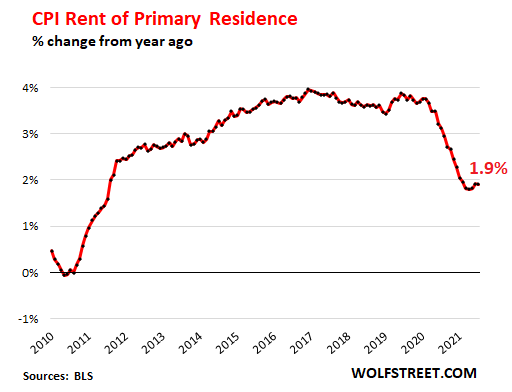

“Rent of primary residence,” which weighs 7.6% in the overall CPI, ticked up just 1.9% year-over-year despite the chaos going on in the rental market, as many cities experienced double-digit rent increases, while others experienced declines. Every month this year, it nudged up 0.2% from the prior month as if nothing had happened. This is the CPI for rent, which has dropped from the 4% range in 2019 to 1.9%:

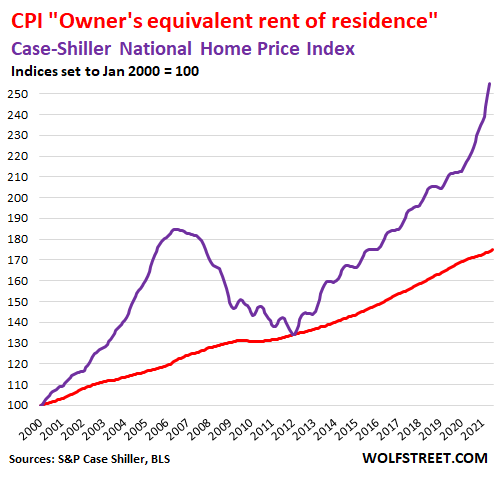

“Owners’ equivalent rent of residences” – the component that tracks the costs of homeownership and weighs 23.6% in the overall CPI – rose just 2.4% year-over-year despite the historic price explosion in the housing market.

The CPI’s homeownership component doesn’t track actual home-price inflation, but it is based on surveys that ask what homeowners think their home might rent for and is therefore a measure of rent as seen by the homeowner.

Meanwhile, back at the ranch, the national median price of existing homes spiked by 23.4% year-over-year, according to the National Association of Realtors.

The Case-Shiller Home Price Index, which tracks the price changes of the same house and is therefore a measure of house price inflation, spiked by 16.6% year-over year, the most in the data going back to 1987 (purple line). And yet, the measure for the costs of homeownership by the BLS barely budged (red line):

Energy costs spiked 23.8% year-over-year.

Energy accounts for 7.2% of the overall CPI. The spike was driven by gasoline, a surprise to no one who has filled up a tank of gas recently, which jumped 41.8% year-over-year. Natural gas jumped 19% year-over-year. The CPI for electricity service to the home rose 4.0% year-over-year.

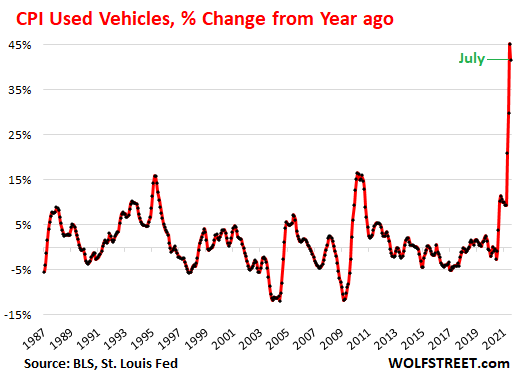

Durable Goods inflation spiked 14.3% year-over-year, along with June the biggest since at least 1957.

The crazy new and used vehicle prices drove, so to speak, the spike in the CPI for durable goods. Other items in this category are appliances, consumer electronics, furniture, tools, bicycles, sports equipment, etc. The CPI for durable goods spiked by 14.3% year-over-year, after having spiked by 14.6% in June, both of which were the biggest jumps in the data going back to 1957.

The CPI for used vehicles jumped by 0.8% in July, but given the crazy spike that began last summer, July’s jump was a lot smaller than the jump in July last year. And on a year-over-year basis – due to this base effect – it spiked a tad less than in June, but by a still mind-bending 41.7%. Not much comfort yet for used vehicle shoppers, but price resistance has finally started to crop up and a portion of this crazy price spike is going to unwind:

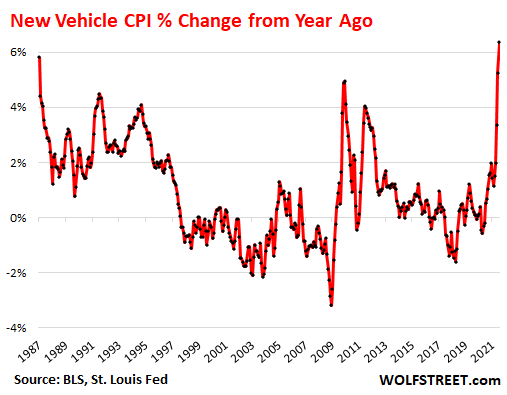

New Vehicle CPI spikes the most since 1982, even as the used vehicle CPI’s spike is slowing. This is the game of inflation Whac-A-Mole, where one price spike here is replaced by another price spike there.

The CPI for new cars and trucks jumped by 1.5% in July, the third month in a row of these types of price spikes, the biggest since the cash-for-clunkers program during the Great Recession. This brought the year-over-year spike to 6.4%, the fastest since January 1982. But as we’ll see in a moment that price spike is understated by “hedonic quality adjustments.”

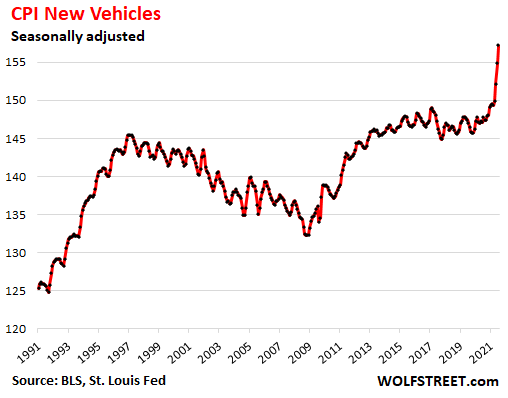

“Hedonic quality adjustments” suppress the CPIs for new & used vehicles. The BLS uses “hedonic quality adjustments” to account for improvements in vehicles over the years. For example, the estimated added costs of the decades-long transition from a four-speed automatic transmission to a 10-speed electronically controlled transmission are removed from the CPI at every step along the way. For an illustration what that means, here is my real-world F-150 and Camry price index compared to this CPI for new vehicles going back to 1989.

In theory, CPI measures price changes of the same item over time; and any improvements change the item, which then boils down to a price increase based on an improvement rather than just the loss of the purchasing power of the dollar. In theory, this makes sense.

In practice, these hedonic quality adjustments have been aggressively applied to push down the CPI, and thereby suppress the appearance of inflation. Under-reporting the loss of the purchasing power of the dollar is a convenient political thing, an effort to keep workers in the dark about the purchasing power of their labor.

The effect can be seen in the new vehicle CPI as an index, which shows that new vehicle prices fell in the years after hedonic quality adjustments took effect, and that in 2019, you could have bought a Camry or an F-150 for the same price as in 2000, which is of course a total farce. It’s only the recent spike that outran the hedonic quality adjustments, but it too will eventually be reeled in by them.

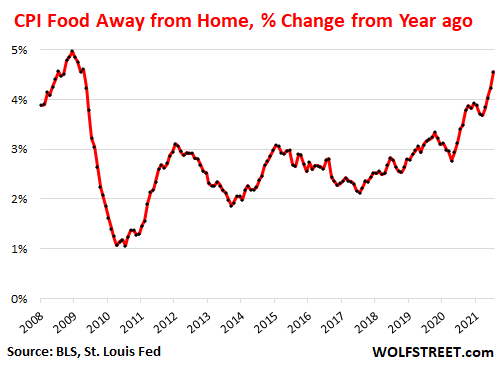

Restaurant prices are next in the inflation Whac-a-Mole.

Everyone who has been eating out or has followed the announcements by the fast-food chains knows that this has been happening, and it is now working itself ever so gradually into the CPI for “Food away from home,” which jumped by 0.8% in July from June, after having jumped 0.7% in June and 0.6% in May. Year-over-year, the index is up 4.6%, the most since 2009. But this is just the beginning.

Restaurants, struggling to hire workers, have increased their wages, and they also face increases in the costs of commodities, ingredients, and services they use, and they face higher operating costs due to the pandemic, and they’ve begun to pass those costs on to consumers:

This loss of purchasing power is “permanent.”

Only a period of deflation – with prices across the board actually dropping – would recuperate the purchasing power of the dollar. But that won’t be allowed. In my lifetime, there were only a few quarters of deflation. The rest of the time, it was either inflation or rampant inflation. And now, after a period of inflation, we’ve got rampant inflation. As the first chart above shows, the loss of purchasing power isn’t “transitory” or “temporary” but rock-solid permanent. What is transitory is the pace of the future losses of purchasing power.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Watch as our sponsor, Classic Metal Roofing Systems, discusses the benefits of using products they manufacture.

Product information is available at Classic Metal Roofing Systems, manufacturer of beautiful metal roofs.

Tesla sold 32,968 China-made vehicles in July, local sales plunged m/m

A Tesla car pictured at a charging point in Beijing, China, April 13, 2018. REUTERS/Thomas Peter/File Photo

BEIJING, Aug 10 (Reuters) – U.S. electric vehicle maker Tesla Inc (TSLA.O) sold 32,968 China-made vehicles in July, including 24,347 for export, the China Passenger Car Association (CPCA) said on Tuesday.

Local sales of China-made vehicles plunged 69% to 8,621 cars from 28,138 in June. Tesla’s sales in the first month of each quarter are usually lower than the following two months.

The company, which makes Model 3 sedans and Model Y sport-utility vehicles in Shanghai, sold 33,155 China-made vehicles in June.

Last month, Tesla introduced a cheaper version of the Model Y in China, where it faces increased scrutiny from both regulators and the public and growing competition from local rivals. It also lowered the starting price for Model 3 sedans.

China’s BYD sold 50,387 electric vehicles last month, while General Motors Co’s (GM.N) China joint venture with SAIC Motor (600104.SS) delivered 27,347 units.

CPCA also said China sold 1.52 million passenger cars in July, down 6.4% from a year earlier.

Reporting by Yilei Sun and Brenda Goh

Editing by Louise Heavens and Mark Potter

Our Standards: The Thomson Reuters Trust Principles.

AMC Entertainment Q4 Sales Plunged 90%, Losses Ballooned Amid Pandemic; CEO Adam Aron Cites “Most Challenging Market Conditions” In 100 Years

TipRanks

Raymond James: These 3 Stocks Are Poised to Surge by at Least 50%

In a recent note on the state of the stock markets, Raymond James equity strategist Tavis McCourt points out a series of policy factors that are playing a role in the current market volatility; the situation is more complex, perhaps, than most of us have been willing to admit. McCourt notes permutations of the SLR rule, political dynamics on the Senate Banking Committee, and the regulatory atmosphere towards potential capital return are all influencing the Fed’s moves and the market reactions. “We believe the Fed will do everything they can to ensure orderly trading in US Treasuries and does not want to see the volatility and liquidity concerns that have occurred in the last week/over the course of the pandemic. We also believe that the Fed is not interested in having a spike in yields as Treasury seeks to finance the next round of stimulus,” McCourt opined. The strategist added, “While the SLR conversation is a political and market issue for the Fed, we believe that any Treasury and/or equity market sell-off tied to the debate is transitory and overblown. We are more focused on the improving economic environment, vaccine distribution, and reflation.” Bearing this in mind, our focus turned to three stocks backed by Raymond James, with the firm’s analysts noting that each could soar over 50% from current levels. Running the tickers through TipRanks’ database, we found out that the rest of the Street is also on board, as each boasts a Moderate or Strong Buy consensus rating. Orasure Technologies (OSUR) We’ll start in the medical industry, a field that has seen gains through the pandemic year. Orasure, through its subsidiaries, is a producer of medical diagnostic tests, and is known for developing rapid test kits for HIV, HEP-C, and Ebola. In the past year, the company created over 150 jobs at its Bethlehem, Pennsylvania facilities as part of an effort to develop fast, at-home, COVID test kits. The company’s product line has a wide range of uses, and is marketed to clinical labs, hospitals, physician practices, and public health agencies world-wide. As can be imagined, Orasure has seen a quick recovery from a 1H20 revenue dip followed by strong gains. Q4 top-line revenues hit $62.9 million, for a 27% year-over-year gain. This was driven by product and services revenues, which grew 28% to reach $60.4 million. EPS was positive, at 3 cents per share, which was a good turnaround from negative results in the first half of the year – but was down 25% from 4Q19. For the full year, Orasure reported $172 million in net revenues, an 11% yoy gain. Of this total, $50 million came from sales of oral fluid collection devices (mouth swabs) for COVID-19 test kits. In addition, the company reported continued progress on its COVID-19 rapid antigen test, and plans to submit prescription self-tests and professional-grade tests for EUA (Emergency Use Authorization) by the FDA by the end of the first quarter. Analyst Andrew Cooper, in his coverage on the stock for Raymond James, saw plenty to like, ticking off the factors by the numbers: “What we liked: 1) Almost every revenue result. Orasure topped consensus sales estimates by 10%… 2) Concrete antigen EUA submission timeline. There is no misunderstanding an expected submission this month, with studies completed and only more administrative type work remaining… 3) More capacity expansion. Existing capacity timelines are on track, but management now intends to add another 50M of annual antigen capacity…” To this end, Cooper puts a $16 price target on the stock, implying a 52% one-year upside, and rates OSUR an Outperform (i.e. Buy). (To watch Cooper’s track record, click here) A solid reputation in the field, and clear path forward are sure to attract positive sentiment – and three Wall Street analysts have put Buy ratings on Orasure, making the analyst consensus a Strong Buy. Shares are priced at $10.49, and the $18.67 average price target is even more bullish than Coopers, suggesting a 78% upside for the next 12 months. (See OSUR stock analysis on TipRanks) Sol-Gel Technologies (SLGL) Sticking to the medical field, we’ll switch focus to a clinical stage pharmaceutical company. Sol-Gel is a biopharma with an interesting niche, developing topical medications for the treatment of skin diseases. The company’s pipeline includes two proprietary formulations based on benzoyl peroxide, both creams: Epsolay, which is a treatment for papulopustular rosacea, and Twyneo, a treatment for acne. Both medications had their NDAs (New Drug Applications) filed with the FDA, and final approval decision is expected in April and August of this year, respectively. Sol-Gel has, in addition, three other drug candidates in early stages of the pipeline process. Two are still in the research phase, while SGT-210 is in Phase I trial, with results due in 1H21. SGT-210 is a potential treatment for palmoplantar keratoderma, a thickening of the skin on the palms of the hands and feet which is sometimes seen as a symptom of several rare conditions. Furthermore, Sol-Gel is working in collaboration with Perrigo as the US manufacturer of generic labels of that company’s brand-name products. In 2020, the two companies signed four agreements, and now have 12 total collaboration projects. Among the fans is Raymond James analyst Elliot Wilbur who writes, “Given the large market opportunity in key pipeline products, coupled with recent acceptance of NDA submissions, we maintain our Strong Buy rating on SLGL shares, as we remain optimistic surrounding near-term growth prospects and financial positioning.” The Strong Buy rating comes with a $23 price target, suggesting SLGL has room to grow an impressive 156% in the year ahead. (To watch Wilbur’s track record, click here) Small-cap biopharmas don’t always get a lot of analyst attention – they tend to fly under the radar. However, there are two reviews on file here and both are to Buy, making the consensus rating a Moderate Buy. SLGL shares are priced at $9, with an average price target of $22 indicating a runway toward ~145% upside for 2021. (See SLGL stock analysis on TipRanks) PAE (PAE) Let’s switch gears, and look at government support services. It’s no secret that governments are huge users of contract service companies, and PAE is a major provider of contract services for US government and defense agencies. PAE has operations on every continent and in 60 countries, providing a range of services, including analysis and training, intelligence, infrastructure operations, management and maintenance, logistic and material support, and information optimization. Until recently, PAE was a privately held company, but in February last year it was merged with Gores Holdings III in a SPAC transaction. The transaction brought PAE shares onto the NASDAQ exchange on February 10, 2020. 2021 has started with some changes in PAE’s contracts with the US government. At the end of January, the company lost a bid to renew a $125 million contract it had held with Customs and Border Patrol since 2009 – but earlier that same month, PAE was awarded a $3.3. billion contract with the US State Department. The contract with State involve consular operations at diplomatic facilities in 120 countries. 5-star analyst Brian Gesuale, in his coverage of PAE for Raymond James, notes the change in contracts, and does not believe it should trouble PAE. “PAE’s qualified pipeline still sits around $40B and pending awards north of $6B, which when combined with the company’s 2020 recompete win rate of 93% provides us confidence that CBP contract can be adequately replaced,” Gesuale commented. Turning to specifics on the State contract, Gesuale adds, “…this contract win could add upwards to $110 to $125 million of high-margin annual revenue to the 2022 model. Overall our estimates are going higher, and we continue to view PAE as one of the more compelling opportunities in the Government IT Services space. While we expect the group will face decelerating fundamentals and a potentially meaningful re-rating lower from near historically high valuations PAE should fare differently as it accelerates organic growth…” In line with these comments, the analyst puts an Outperform (i.e. Buy) rating on the stock, and his $15 price target implies a 77% one-year upside. (To watch Gesuale’s track record, click here) PAE stock has a resounding “yes” on Wall Street. TipRanks analytics show that out of 3 analysts, all 3 are bullish. The average price target of $12.67 shows a potential upside of about 50%. (See PAE stock analysis on TipRanks) To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights. Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Trump business revenues plunged during pandemic, final disclosure reveals

Former President Donald Trump’s business empire lost significant revenue during the pandemic, as the virus and the failed response to it cost his own interests money, according to a financial disclosure document released after he left office Wednesday.

Most of his core golf and hotel properties saw steep declines as the virus and lockdown restrictions kept consumers home and suspended discretionary travel.

Compared to his disclosure from the year prior, revenues at the Trump National Doral Miami golf course in Florida declined from $77 million to $44 million. Trump’s Turnberry golf club in Scotland saw revenues fall from $25 million to just under $10 million.

Revenues also declined from $40.5 million to $15 million at Trump’s hotel at the leased Old Post Office location in Washington, D.C.

Total revenue fell at the Trump International Hotel & Tower Chicago hotel-condo last year, with hotel management fees tumbling from nearly $2 million to about half a million, and condo management fees rising slightly.

Business increased in some red state locations, such as his golf club in Charlotte, North Carolina, where revenues rose from $12 million to $13 million. Revenues at Mar-a-Lago, his private club in Florida and new residence, rose $3 million.

But overall, the net impact was negative, with Trump’s declared revenue falling from a reported $445 million to $278 million.

The Trump Organization did not immediately respond to an NBC News request for comment.

The documents detail the buying and selling of various bonds and exchange traded funds during 2020 as the S&P 500 index gyrated from 2,800 points at the beginning of the year, fell nearly 20 percent as the virus lockdowns and layoffs hit, then recovered to around 3,700 on Jan. 15, the day Trump signed the document.

The disclosure shows active loans at several banks, some of which, including Deutsche and Professional, have sworn off doing future business with Trump.

The documents show one financial institution, Investors Savings Bank, extending for one year the term of a loan set to expire in 2020 — at a slightly higher interest rate. The mortgage was for between $5 million and $25 million for Trump Park Avenue. The bank did not immediately respond to a request for comment.

The document is a 79-page final glimpse of Trump’s reported finances as he returns to life as a private citizen and grapples with how to capitalize on his altered brand, post-presidency.

It also provides details about several gifts Trump and his family accepted last year. They include a $25,000 “bronze statue depicting flag raising over Iwo Jima” from a Denver-based veterans association, a Mac Pro from Apple CEO Tim Cook, and a $500 customized golf club from Dennis Muilenburg, the disgraced former CEO of Boeing.