- This city never slept. But with China tightening its grip, is the party over? CNN

- China Accuses US of Encouraging Provocations in South China Sea Bloomberg

- China Coordinator Mark B. Lambert’s Meeting with the People’s Republic of China (PRC) Ministry of Foreign Affairs Director-General for Boundary and Ocean Affairs Hong Liang – United States Department of State Department of State

- US, Chinese diplomats meet to discuss maritime issues including South China Sea South China Morning Post

- China and Southeast Asia nations vow to conclude a nonaggression pact faster as sea crises escalate The Washington Post

- View Full Coverage on Google News

Tag Archives: tightening

Jeff Bezos’ Blue Origin is a ‘work-from-work’ company, says leaked email tightening office mandate – New York Post

- Jeff Bezos’ Blue Origin is a ‘work-from-work’ company, says leaked email tightening office mandate New York Post

- An Amazon exec says it’s time for workers to ‘disagree and commit’ to an office return: ‘I don’t have data to back it up, but I know it’s better’ Fortune

- Blue Origin tells staff to catch next rocket back to their desks The Register

- Blue Origin Tightens RTO Policy, Saying It’s ‘Work-From-Work’ Company Business Insider

- Amazon Exec Says He Has ‘No Data’ to Support Return-to-Office Mandate Business Insider

- View Full Coverage on Google News

Biden administration finalizes new rule tightening regulations on gun stabilizing braces

The Biden administration has finalized a new rule to tighten restrictions on stabilizing braces for firearms that can convert pistols into rifles.

The Justice Department said in a release on Friday that it submitted its rule to the Federal Register, clarifying that manufacturers, dealers and individuals must comply with laws regulating rifles when they use stabilizing braces to convert pistols to rifles with a barrel of less than 16 inches, which are known as short-barreled rifles.

The release states that Attorney General Merrick Garland directed the Bureau of Alcohol, Tobacco, Firearms and Explosives (ATF) to address stabilizing braces in April 2021.

“Almost a century ago, Congress determined that short-barreled rifles must be subject to heightened requirements,” Garland said in the release. “Today’s rule makes clear that firearm manufacturers, dealers, and individuals cannot evade these important public safety protections simply by adding accessories to pistols that transform them into short-barreled rifles.”

The release states the National Firearms Act has placed certain restrictions on short-barreled rifles since the 1930s because they are easier to conceal than long-barreled rifles and have more destructive power than traditional handguns.

The increased requirements include background checks for all transfers and additional taxation.

“This rule enhances public safety and prevents people from circumventing the laws Congress passed almost a century ago,” ATF Director Steven Dettelbach said. “In the days of Al Capone, Congress said back then that short-barreled rifles and sawed-off shotguns should be subjected to greater legal requirements than most other guns.”

But Dettelbach said the stabilizing braces are designed to attach to a pistol to convert it to a short-barreled rifle to be fired from the shoulder.

The release states that the rule allows a 120-day period for manufacturers, dealers and individuals to register any existing short-barreled rifles covered by the rule tax-free. They can also remove the stabilizing brace to restore the firearm to be a pistol, or turn over the converted short-barreled rifles to the ATF.

The release notes that stabilizing braces are not banned under the rule, only that certain restrictions must apply when they are used to convert the pistols.

The Justice Department initially proposed the rule in June 2021, and the ATF received more than 237,000 comments during the 90-day public comment period.

The rule will go into effect on the date that the Federal Register publishes it, which Reuters reported will likely be next week.

U.S. labor market shrugs off recession fears; keeps Fed on tightening path

WASHINGTON, Dec 2 (Reuters) – U.S. employers hired more workers than expected in November and increased wages, shrugging off mounting worries of a recession, but that will probably not stop the Federal Reserve from slowing the pace of its interest rate hikes starting this month.

Despite the strong job growth, some details of the Labor Department’s closely watched employment report on Friday were a bit weak, which economists said could be flagging upcoming labor market weakness. Household employment decreased for a second straight month. About 186,000 people left the labor force, keeping the unemployment rate unchanged at 3.7%.

Labor market tightness and strength keeps the Fed on its monetary policy tightening path at least through the first half of 2023, and could raise its policy rate to a higher level where it could stay for sometime. It also underscores the economy’s resilience heading into was is expected to be a tough year.

“November’s labor market report was clearly bad news for the Fed’s war on inflation,” said Jan Groen, chief U.S. macro strategist at TD Securities in New York. “The Fed has no other choice than to remain in tightening mode for the near future, with 50 basis points hikes in December and February.”

Nonfarm payrolls increased by 263,000 jobs last month. Data for October was revised higher to show payrolls rising 284,000 instead of 261,000 as previously reported. Monthly job growth of 100,000 is needed to keep pace with growth in the labor force.

Economists polled by Reuters had forecast payrolls increasing 200,000. Estimates ranged from 133,000 to 270,000. Employment growth has averaged 392,000 per month this year compared with 562,000 in 2021.

Hiring remains strong despite announcements of thousands of job cuts by technology companies, including Twitter, Amazon (AMZN.O) and Meta (META.O), the parent of Facebook.

Economists say these companies are right-sizing after over-hiring during the COVID-19 pandemic, noting that small firms remain desperate for workers.

There were 10.3 million job openings at the end of October, with 1.7 openings for every unemployed person, many of them in the leisure and hospitality as well as healthcare and social assistance industries.

The gains in employment last month were led by the leisure and hospitality sector, which added 88,000 jobs, most of them at restaurants and bars. Leisure and hospitality employment remains down 980,000 from its pre-pandemic level.

There were 45,000 jobs added in healthcare, while government payrolls increased 42,000. Construction employment increased by 20,000 jobs despite the housing market turmoil, while manufacturing added 14,000 jobs.

But retail trade employment fell by 30,000 jobs, with most of the losses in general merchandise stores. Transportation and warehousing payrolls decreased by 15,000 jobs. Temporary help jobs, a segment normally considered a harbinger of future hiring, decreased by 17,200.

“The labor market might encounter some bumps in the road next year, but it’s heading into 2023 cruising,” said Nick Bunker, head of economic research at the Indeed Hiring Lab.

Fed Chair Jerome Powell said on Wednesday the U.S. central bank could scale back the pace of its rate hikes “as soon as December.” The Fed has raised its policy rate by 375 basis points this year from near zero to a 3.75%-4.00% range in the fastest rate-hiking cycle since the 1980s.

Policymakers meet on Dec. 13 and 14. Attention now shifts to November’s consumer price data due on Dec. 13.

Stocks on Wall Street fell. The dollar rose against a basket of currencies. U.S. Treasury prices were lower.

WAGES ACCELERATE

With the labor market still tight, average hourly earnings increased 0.6% after advancing 0.5% in October. That raised the annual increase in wages to 5.1% from 4.9% in October. Wage growth peaked at 5.6% in March.

The broad wage gains suggest that the moderation in inflation, evident in October data, will be gradual. Economists said this also raised concerns about a wage-price spiral that could keep service prices rising outside the shelter component. Fed officials have shied away from calling a price-wage spiral.

“The broad-based nature of the increase and its consistency with other data on wages makes us think that around 5% average hourly earnings growth is not an aberration,” said Andrew Hollenhorst, chief U.S. economist at Citigroup in New York.

Strong wage gains are helping to drive consumer spending, which surged in October, leading economists to believe that an anticipated recession next year would be short and shallow. But there are some signs of weakness emerging in the labor market.

Household employment decreased by 138,000 jobs, the second straight monthly decline. Though household employment tends to be volatile as it is drawn from a smaller sample compared to nonfarm payrolls, economists said the divergence between these two measures was important to watch.

“The household survey may be better in capturing turning points in the labor market than the payroll survey, since the payroll survey is unable to adequately capture activity in opening and closing firms while the household survey can,” said Sophia Koropeckyj, a senior economist at Moody’s Analytics in West Chester, Pennsylvania.

Others, however, argued nonfarm payrolls were a better gauge and expected household employment to converge with payrolls.

The participation rate, or the proportion of working-age Americans who have a job or are looking for one, slipped to 62.1% from 62.2% in October. Some of the decrease in household employment and participation was likely because of illness, with 1.6 million people saying they were absent from work because they were sick, up 265,000 from October.

The participation rate for Americans 55 years and older fell, possibly reflecting retirements. The employment-to-population ratio dipped to 59.9% from 60.0% in October.

Reporting by Lucia Mutikani; Editing by Chizu Nomiyama and Andrea Ricci

Our Standards: The Thomson Reuters Trust Principles.

Why ‘quantitative tightening’ is the wild card that could sink the stock market

Quantitative monetary easing is credited for juicing stock market returns and boosting other speculative asset values by flooding markets with liquidity as the Federal Reserve snapped up trillions of dollars in bonds during both the 2008 financial crisis and the 2020 coronavirus pandemic in particular. Investors and policy makers may be underestimating what happens as the tide goes out.

“I don’t know if the Fed or anybody else truly understands the impact of QT just yet,” said Aidan Garrib, head of global macro strategy and research at Montreal-based PGM Global, in a phone interview.

The Fed, in fact, began slowly shrinking its balance sheet — a process known as quantitative tightening, or QT — earlier this year. Now it’s accelerating the process, as planned, and it’s making some market watchers nervous.

A lack of historical experience around the process is raising the uncertainty level. Meanwhile, research that increasingly credits quantitative easing, or QE, with giving asset prices a lift logically points to the potential for QT to do the opposite.

Since 2010, QE has explained about 50% of the movement in market price-to-earnings multiples, said Savita Subramanian, equity and quant strategist at Bank of America, in an Aug. 15 research note (see chart below).

BofA U.S. Equity & Quant Strategy

“Based on the strong linear relationship between QE and S&P 500 returns from 2010 to 2019, QT through 2023 would translate into a 7 percentage-point drop in the S&P 500 from here,” she wrote.

Archive: How much of the stock market’s rise is due to QE? Here’s an estimate

In quantitative easing, a central bank creates credit that’s used to buy securities on the open market. Purchases of long-dated bonds are intended to drive down yields, which is seen enhancing appetite for risky assets as investors look elsewhere for higher returns. QE creates new reserves on bank balance sheets. The added cushion gives banks, which must hold reserves in line with regulations, more room to lend or to finance trading activity by hedge funds and other financial market participants, further enhancing market liquidity.

The way to think about the relationship between QE and equities is to note that as central banks undertake QE, it raises forward earnings expectations. That, in turn, lowers the equity risk premium, which is the extra return investors demand to hold risky equities over safe Treasurys, noted PGM Global’s Garrib. Investors are willing to venture further out on the risk curve, he said, which explains the surge in earnings-free “dream stocks” and other highly speculative assets amid the QE flood as the economy and stock market recovered from the pandemic in 2021.

However, with the economy recovering and inflation rising the Fed began shrinking its balance sheet in June, and is doubling the pace in September to its maximum rate of $95 billion per month. This will be accomplished by letting $60 billion of Treasurys and $35 billion of mortgage backed securities roll off the balance sheet without reinvestment. At that pace, the balance sheet could shrink by $1 trillion in a year.

The unwinding of the Fed’s balance sheet that began in 2017 after the economy had long recovered from the 2008-2009 crisis was supposed to be as exciting as “watching paint dry,” then-Federal Reserve Chairwoman Janet Yellen said at the time. It was a ho-hum affair until the fall of 2019, when the Fed had to inject cash into malfunctioning money markets. QE then resumed in 2020 in response to the COVID-19 pandemic.

More economists and analysts have been ringing alarm bells over the possibility of a repeat of the 2019 liquidity crunch.

“If the past repeats, the shrinking of the central bank’s balance sheet is not likely to be an entirely benign process and will require careful monitoring of the banking sector’s on-and off-balance sheet demandable liabilities,” warned Raghuram Rajan, former governor of the Reserve Bank of India and former chief economist at the International Monetary Fund, and other researchers in a paper presented at the Kansas City Fed’s annual symposium in Jackson Hole, Wyoming, last month.

Hedge-fund giant Bridgewater Associates in June warned that QT was contributing to a “liquidity hole” in the bond market.

The slow pace of the wind-down so far and the composition of the balance-sheet reduction have muted the effect of QT so far, but that’s set to change, Garrib said.

He noted that QT is usually described in the context of the asset side of the Fed’s balance sheet, but it’s the liability side that matters to financial markets. And so far, reductions in Fed liabilities have been concentrated in the Treasury General Account, or TGA, which effectively serves as the government’s checking account.

That’s actually served to improve market liquidity he explained, as it means the government has been spending money to pay for goods and services. It won’t last.

The Treasury plans to increase debt issuance in coming months, which will boost the size of the TGA. The Fed will actively redeem T-bills when coupon maturities aren’t sufficient to meet their monthly balance sheet reductions as part of QT, Garrib said.

The Treasury will be effectively taking money out of economy and putting it into the government’s checking account — a net drag — as it issues more debt. That will put more pressure on the private sector to absorb those Treasurys, which means less money to put into other assets, he said.

The worry for stock-market investors is that high inflation means the Fed won’t have the ability to pivot on a dime as it did during past periods of market stress, said Garrib, who argued that the tightening by the Fed and other major central banks could set up the stock market for a test of the June lows in a drop that could go “significantly below” those levels.

The main takeaway, he said, is “don’t fight the Fed on the way up and don’t fight the Fed on the way down.”

Stocks ended higher on Friday, with the Dow Jones Industrial Average

DJIA,

+1.19%,

S&P 500

SPX,

+1.53%

and Nasdaq Composite

COMP,

+2.11%

snapping a three-week run of weekly losses.

The highlight of the week ahead will likely come on Tuesday, with the release of the August consumer-price index, which will be parsed for signs inflation is heading back down.

A ‘firestorm’ of hawkish Fed speculation erupts following strong U.S. inflation reading

How hawkish will the Federal Reserve be this year?

At the moment, Wall Street economists seem to be telling their clients “more hawkish than we thought five minutes ago.”

The strong U.S. consumer inflation data reported Thursday has set off what looks like a chain reaction of upward revisions to projected interest rates rises and where the Fed is headed with monetary policy.

Fed watchers are talking seriously about an “emergency” interest rate hike before the Fed’s next formal meeting on March 16.

The consumer price index rose 0.6% in January, with broad based gains. The year-over-year rate rose to 7.5%, the highest level in 40 years.

Read: Consumer price inflation increases sharply in January

In the wake of the data, Goldman Sachs said it now sees seven consecutive 25 basis point rate hikes at each of the remaining Fed policy meeting this year. The investment bank’s earlier prediction was five hikes.

Economists at Citi said that their base case is a now for a 50 basis point hike in March followed by quarter point hikes in May, June, September and December.

Marc Cabana, head of U.S. rates strategy at BofA Securities, told Bloomberg Radio that it is very likely the Fed is going to raise rates by 50 basis points in March and “who knows, maybe even 50 in May.”

The talk about an inter-meeting rate hike before March 16 erupted late Thursday after St. Louis Fed President James Bullard said was open to having that discussion.

Market analyst Mohamed Ed-Erian said the frenzy of speculation is a sign the Fed has lost control of the policy narrative. He said he didn’t want to see the Fed take aggressive moves because the market will price in aggressive moves again and again.

“This is what typically happens in a developing country when a central bank loses control of the policy narrative,” he said.

March Chandler, forex analyst for Bannockburn Global Forex, said it will be difficult for Fed officials to get ahead of the curve of expectations.

It is a strange time for the Fed. The central bank has been slowly “tapering” or reducing the amount of securities is is buying under its quantitative easing program started in the depth of the pandemic. The buying of Treasurys and mortgage backed securities is scheduled to end in mid-March.

Some Fed watchers think the Fed may decide to end these purchases “cold turkey,” with the announcement coming Friday.

Under the Fed’s QE program, the Fed is scheduled to release its schedule for the last month of asset purchases.

“If the Fed releases that calendar at 3 p.m, it is pretty strong forward guidance they’re not going to do an intermeeting hike,” Cabana said.

Cabana said he didn’t expect a rate hike before the March 16 meeting. He suggested that investors who want to bet on an intermeeting hike would be better positioned to play for a 75 basis point hike in March.

However, Robert Perli, head of global policy at Piper Sandler, said the firestorm among Fed watchers felt like “much ado about little.”

“We are first to recognize that inflation is too high for comfort. But what we learned yesterday from both the CPI report and FOMC members doesn’t seem enough to change the policy outlook nearly as much as the market did,” Perli said, in a note to clients.

Three Fed officials were not as hawkish as Bullard in their comments the wake of the CPI report.

Richmond Fed President Tom Barkin told the Stanford Institute for Economic Policy Research on Thursday evening that he would have to be convinced of a need for a 50 basis point rate hike, Reuters said.

In an interview with Market News International, San Francisco Fed President Mary Daly downplayed the chances of a half-a-percentage point hike in March.

And Atlanta Fed President Raphael Bostic told CNBC after the CPI data that he was sticking with his call for four rate hikes this year, including a 25 basis point hike in March.

Tim Duy, chief U.S. economist at SGH Macro Advisors, called these dovish Fed comments “nonsensical.”

“It is just getting to the point where the distance between the Fed’s current position and reality is too wide to ignore any longer,” Duy said, in a note to clients.

U.S. stocks

DJIA,

-0.17%

SPX,

-0.45%

were mixed late morning Friday after a wild week on Wall Street. The yield on the 10-year Treasury note

TMUBMUSD10Y,

2.024%

stayed above 2%, the highest level since 2019.

IMF says emerging economies must prepare for Fed policy tightening

A participant stands near a logo of IMF at the International Monetary Fund – World Bank Annual Meeting 2018 in Nusa Dua, Bali, Indonesia, October 12, 2018. REUTERS/Johannes P. Christo

Register now for FREE unlimited access to Reuters.com

Register

WASHINGTON, Jan 10 (Reuters) – Emerging economies must prepare for U.S. interest rate hikes, the International Monetary Fund said, warning that faster than expected Federal Reserve moves could rattle financial markets and trigger capital outflows and currency depreciation abroad.

In a blog published Monday, the IMF said it expected robust U.S. growth to continue, with inflation likely to moderate later in the year. The global lender is due to release fresh global economic forecasts on Jan. 25.

It said a gradual, well-telegraphed tightening of U.S. monetary policy would likely have little impact on emerging markets, with foreign demand offsetting the impact of rising financing costs.

Register now for FREE unlimited access to Reuters.com

Register

But broad-based U.S. wage inflation or sustained supply bottlenecks could boost prices more than anticipated and fuel expectations for more rapid inflation, triggering faster rate hikes by the U.S. central bank.

“Emerging economies should prepare for potential bouts of economic turbulence,” the IMF said, citing the risks posed by faster-than-expected Fed rate hikes and the resurgent pandemic.

St. Louis Fed President James Bullard this week said the Fed could raise interest rates as soon as March, months earlier than previously expected, and is now in a “good position” to take even more aggressive steps against inflation, as needed.

“Faster Fed rate increases could rattle financial markets and tighten financial conditions globally. These developments could come with a slowing of U.S. demand and trade and may lead to capital outflows and currency depreciation in emerging markets,” senior IMF officials wrote in the blog.

It said emerging markets with high public and private debt, foreign exchange exposures, and lower current-account balances had already seen larger movements of their currencies relative to the U.S. dollar.

The fund said emerging markets with stronger inflation pressures or weaker institutions should act swiftly to let currencies depreciate and raise benchmark interest rates.

It urged central banks to clearly and consistently communicate their plans to tighten policy, and said countries with high levels of debt denominated in foreign currencies should look to hedge their exposures where feasible.

Governments could also announce plans to boost fiscal resources by gradually increasing tax revenues, implementing pension and subsidy overhauls, or other measures, it added.

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Andrea Shalal; Editing by Lincoln Feast.

Our Standards: The Thomson Reuters Trust Principles.

Treasury Yields & Mortgage Rates Spike: Markets Begin to Grapple with Quantitative Tightening

This is now moving fast.

By Wolf Richter for WOLF STREET.

The two-year Treasury yield started rising in late September, from about 0.23%, and ended the year at 0.73%. In the five trading days since then, it jumped to 0.87%, the highest since February 28, 2020. Most of the jump occurred on Wednesday and Thursday, triggered by the hawkish Fed minutes on Wednesday.

Markets are finally and in baby steps starting to take the Fed seriously. And the most reckless Fed ever – it’s still printing money hand-over-fist and repressing short-term interest rates to near 0%, despite the worst inflation in 40 years – is finally and in baby steps, after some kind of come-to-Jesus moment late last year, starting to take inflation seriously. Treasury yields are now responding:

Jawboning about Quantitative Tightening.

Even though the Fed hasn’t actually done any hawkish thing, and is still printing money and repressing interest rates to near 0%, it is laying the groundwork with innumerable warnings all over the place, from the FOMC post-meeting presser on December 15, when Powell said everything would move faster, to hawkish speeches by Fed governors, to the very hawkish minutes of the FOMC meeting, which put Quantitative Tightening in black-and-white.

The Fed is now spelling out that it will make Quantitative Tightening – QT is the opposite of QE – its primary policy tool in battling inflation. It even spelled out in the minutes why QT won’t blow up the repo market, as it had done last time in September 2019, because last July, the Fed established the Standing Repo Facilities (SRFs) to calm the repo market while the balance sheet gets unwound sooner, faster, and by more than last time.

It is now clear to everyone that the Fed will hike interest rates sooner and by more than expected just a few months ago, and that it will reduce its balance sheet sooner, faster, and by a lot more.

This is a huge thing. And the Fed is communicating this shift to the markets so that markets can adjust to it gradually, more or less orderly, and not all at once. And the Treasury market is doing that.

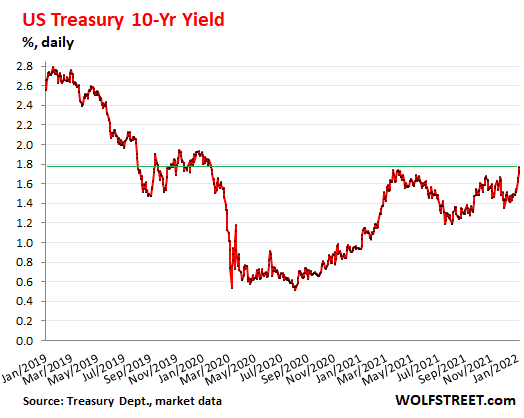

10-year Treasury yield highest in nearly two years.

The 10-year Treasury yield has risen by 25 basis points since the end of the year, to 1.78% on Friday. It’s now at the highest point since January 21, 2020, before the pandemic was even a factor for the markets:

The jawboning will continue until morale improves.

Browbeaten by the worst and very un-temporary inflation in 40 years, even ultimate Fed doves, such as San Francisco Fed President Mary Daly on Friday, are now talking up rate hikes this year, and more importantly the arrival of Quantitative Tightening soon after liftoff.

“I would prefer to see us adjust the policy rate gradually and move into balance sheet reduction earlier than we did in the last cycle,” she said, echoing in harmony what the minutes of the December 15 FOMC meeting had revealed in detail on Wednesday.

Powell and the minutes called the balance sheet reduction the “runoff.” This Quantitative Tightening, or QT, is the opposite of QE.

QE was designed to push down long-term interest rates, and it did a marvelous job at that, and it triggered the biggest asset bubbles the US had ever seen, including the massive real estate bubble, with house prices spiking by 20% over a 12-month period, from already very lofty levels.

QT does the opposite: It allows long-term interest rates to drift higher, and markets will adjust to it, just like they adjusted to QE.

Markets are responding to the Fed’s jawboning, and long-term rates are already rising even though the Fed has just started to talk about QT, while it’s still doing QE, and while it’s still repressing short-term interest rates. Jawboning is an essential and official tool in the Fed’s toolbox.

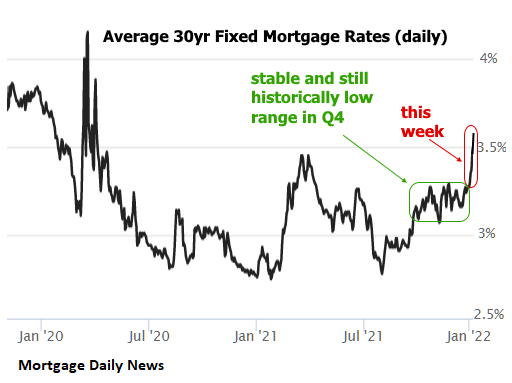

Mortgage rates highest in two years and moving fast.

The surge in the 10-year Treasury yield has already translated into the highest mortgage rates in nearly two years. And those rates are moving higher fast.

According to Freddie Mac, the average 30-year fixed rate mortgage rate rose to 3.22%, the highest since May 2020. But that was based on surveys that most mortgage bankers filled out at the beginning of the week. And since then, mortgage rates have spiked.

Daily measures of average mortgage rates have jumped every day. The Average 30-Year Fixed-Rate Mortgage Rates index by Mortgage News Daily has jumped to around 3.50% on Thursday and Friday – rates not seen since the end of January 2020 (chart via Mortgage Daily News)

This rate of 3.50% is still very low, but it’s a lot higher than it was in 2020, when the average 30-year fixed rate dropped to 2.65%. And the Fed is still repressing long-term interest rates via QE. QT won’t even start for a few months. So the show hasn’t even stared yet. We’re watching the preview.

And these coming higher mortgage rates will have to be used to finance the home prices that have exploded by ridiculous amounts over the past 18 months from already ridiculously inflated prices, given the massive QE and interest rate repression for a big part of the past 13 years.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Classic Metal Roofing Systems, our sponsor, manufactures beautiful metal shingles:

- A variety of resin-based finishes & colors

- Deep grooves for a high-end natural look

- Maintenance free – will not rust, crack, or rot

- Resists streaking and staining

To reach the Classic Metal Roofing folks, click here or call 1-800-543-8938

NASA delays tightening James Webb Space Telescope sunshield to study power system

NASA personnel are spending the day studying the power subsystem of the massive James Webb Space Telescope to ensure the observatory is ready to execute a key procedure: tensioning its vast sunshield.

The Webb space telescope, which launched on Dec. 25, is conducting a month-long deployment procedure necessary to prepare the telescope to gather data. But most steps in that procedure are controlled from the ground: While NASA has a tentative schedule for the work, mission leaders can decide to adjust the timeline along the way. So after taking Saturday (Jan. 1) as a rest day, the Webb team is spending Sunday (Jan. 2) studying the observatory’s power subsystem, NASA announced.

“Nothing we can learn from simulations on the ground is as good as analyzing the observatory when it’s up and running,” Bill Ochs, Webb project manager at NASA’s Goddard Space Flight Center (GSFC) in Maryland, said in an agency statement released Sunday (Jan. 2). “Now is the time to take the opportunity to learn everything we can about its baseline operations. Then we will take the next steps.”

Live updates: NASA’s James Webb Space Telescope mission

Related: How the James Webb Space Telescope works in pictures

In particular, the team is focused on the temperature of a set of motors that will be used during sunshield tensioning, the process that separates and smooths the five delicate layers of the kite-shaped sun deflector. (Webb specializes in infrared observations, which are sensitive to heat, making the sunshield a vital component of the observatory.)

“We’ve spent 20 years on the ground with Webb, designing, developing, and testing,” Mike Menzel, Webb’s lead systems engineer at GSFC said in the same statement. “We’ve had a week to see how the observatory actually behaves in space. It’s not uncommon to learn certain characteristics of your spacecraft once you’re in flight. That’s what we’re doing right now. So far, the major deployments we’ve executed have gone about as smoothly as we could have hoped for. But we want to take our time and understand everything we can about the observatory before moving forward.”

Tensioning the sunshield is a complex process that NASA expects to take two days. NASA initially intended to start the work on Saturday, but Friday’s operations ran later than expected and the team decided to take New Year’s Day to rest.

And when mission managers decided to take a closer look at the motor temperatures, they didn’t want the team to be working on two aspects of the observatory at once.

After the sunshield is fully tensioned, the team will move on to deploying the secondary mirror.

Although deployment has paused, the observatory is still making progress. As of just before 3 p.m. EST (2000 GMT), Webb was more than 510,000 miles (825,000 kilometers) away from Earth, or 57% of the way to its final destination of the Earth-sun Lagrange point 2. That point, also known as L2, is located nearly 1 million miles (1.6 million kilometers) from Earth in the direction opposite the sun.

Email Meghan Bartels at mbartels@space.com or follow her on Twitter @meghanbartels. Follow us on Twitter @Spacedotcom and on Facebook.

U.S. export tightening slows advance of Chinese C919 jet -sources

FILE PHOTO: The fifth prototype of China’s home-built C919 passenger plane takes off for its first test flight from Shanghai Pudong International Airport in Shanghai, China October 24, 2019. Picture taken October 24, 2019. REUTERS/Stringer/File Photo

ZHUHAI, China, Sept 27 (Reuters) – China’s C919 jetliner – a no-show at the country’s biggest air show this week – has found it harder to meet certification and production targets amid tough U.S. export rules, according to three people with knowledge of the programme.

The state-owned manufacturer, Commercial Aircraft Corp of China (COMAC), has been unable to get timely help from suppliers and has run out of some spare parts, those people said.

As of December 2020, the U.S. has required special licenses to export parts and technology assistance to any company with ties to the Chinese military. That has thrown a monkey wrench into the C919 programme, which has been in development for 13 years – one of the longest such periods in aviation.

U.S.-linked suppliers are gradually receiving the licences, but the hiccup has slowed down Chinese certification, and months-long delays threaten to affect early production, said the people, who declined to be named because of the sensitivity of the matter.

COMAC has 815 provisional orders, but only China Eastern Airlines (600115.SS) placed a firm order for five jets.

The state-backed airline said in August it expects to receive its first C919 by the end of the year, two in 2022 and two more in 2023.

A slow production rampup would mean the C919 will not pose a near-term threat to Airbus (AIR.PA) and Boeing (BA.N), which produce dozens of narrowbodies a month.

“One of the biggest hurdles is going to be the supply chain, especially now with inflation, material availability and supplier changes,” said aerospace supply chain expert Alex Krutz at U.S-based aerospace consultancy Patriot Industrial Partners.

“The suppliers may not have the liquidity to make the post-certification changes or be willing as they were a few years ago to continue supporting an initial lower-rate production programme like COMAC,” he added.

COMAC is years behind its initial certification schedule – one reason it did not take the C919 to the China Airshow. read more

“COMAC are very preoccupied with test flights. They’re behind schedule and are flying as much as they can to reach the minimum hours needed for Chinese certification,” an industry source told Reuters. “Despite all the issues, COMAC is very determined to get certified, as this is a paramount political task.”

Sources say that the C919 is likely to receive its type certificate from China’s aviation regulator by the end of this year, but that there will be a long list of limits on flight operations. Even after the certification, COMAC must make upgrades, the sources said.

COMAC and the Civil Aviation Administration of China (CAAC) did not respond to requests to comment.

CAUTIOUS REGULATOR

The sources with knowledge of the C919 programme said the jet’s progress seemed to mirror the certification pattern and slow production of its predecessor, the ARJ21 regional jet.

The ARJ21 faced a 2.5-year gap between obtaining a “type certificate”, which declares the design safe, and a “production certificate” allowing it to enter mass production.

That contrasts with the West, where those certificates are typically granted around the same time.

About 60 ARJ21 aircraft have been delivered to date, but the production ramp-up was also slow, rising from two planes a year in 2017 to 24 in 2020, according to COMAC data.

The C919 is in a phase called “batch production”, where each plane requires a sign-off by the regulator.

FOREIGN PARTS

The C919 is assembled in China but relies heavily on Western components, including engines and avionics. That has made it vulnerable to crackdowns on key technology transfers.

The addition of two key COMAC subsidiaries to a list of companies with military ties in December 2020 created bureaucratic licensing requirements.

China has been doubling down on developing its own engine for the C919; state engine maker Aero Engine Corporation of China (AECC) will display a model of the CJ-1000 engine at the air show, but the domestic solution for the airliner is years away.

AECC is spending 10 billion yuan ($1.55 billion) to build an industrial complex in the southwestern city of Chengdu to manufacture engine nacelles and thrust reversers, local media reported last month. A source with knowledge of the matter said the complex related to CJ-1000 production.

The nacelle capacity is expected to reach 100 per year, enough for 50 planes, the reports said, though no target date was stated. AECC did not respond immediately to a request for comment.

($1 = 6.4589 Chinese yuan renminbi)

Reporting by Stella Qiu and David Kirton in Zhuhai and Jamie Freed in Sydney; additional reporting by Tim Hepher in Paris; Editing by Miyoung Kim and Gerry Doyle

Our Standards: The Thomson Reuters Trust Principles.