Some investors are on edge that the Federal Reserve may be overtightening monetary policy in its bid to tame hot inflation, as markets look ahead to a reading this coming week from the Fed’s preferred gauge of the cost of living in the U.S.

“Fed officials have been scrambling to scare investors almost every day recently in speeches declaring that they will continue to raise the federal funds rate,” the central bank’s benchmark interest rate, “until inflation breaks,” said Yardeni Research in a note Friday. The note suggests they went “trick-or-treating” before Halloween as they’ve now entered their “blackout period” ending the day after the conclusion of their November 1-2 policy meeting.

“The mounting fear is that something else will break along the way, like the entire U.S. Treasury bond market,” Yardeni said.

Treasury yields have recently soared as the Fed lifts its benchmark interest rate, pressuring the stock market. On Friday, their rapid ascent paused, as investors digested reports suggesting the Fed may debate slightly slowing aggressive rate hikes late this year.

Stocks jumped sharply Friday while the market weighed what was seen as a potential start of a shift in Fed policy, even as the central bank appeared set to continue a path of large rate increases this year to curb soaring inflation.

The stock market’s reaction to The Wall Street Journal’s report that the central bank appears set to raise the fed funds rate by three-quarters of a percentage point next month – and that Fed officials may debate whether to hike by a half percentage point in December — seemed overly enthusiastic to Anthony Saglimbene, chief market strategist at Ameriprise Financial.

“It’s wishful thinking” that the Fed is heading toward a pause in rate hikes, as they’ll probably leave future rate hikes “on the table,” he said in a phone interview.

“I think they painted themselves into a corner when they left interest rates at zero all last year” while buying bonds under so-called quantitative easing, said Saglimbene. As long as high inflation remains sticky, the Fed will probably keep raising rates while recognizing those hikes operate with a lag — and could do “more damage than they want to” in trying to cool the economy.

“Something in the economy may break in the process,” he said. “That’s the risk that we find ourselves in.”

‘Debacle’

Higher interest rates mean it costs more for companies and consumers to borrow, slowing economic growth amid heightened fears the U.S. faces a potential recession next year, according to Saglimbene. Unemployment may rise as a result of the Fed’s aggressive rate hikes, he said, while “dislocations in currency and bond markets” could emerge.

U.S. investors have seen such financial-market cracks abroad.

The Bank of England recently made a surprise intervention in the U.K. bond market after yields on its government debt spiked and the British pound sank amid concerns over a tax cut plan that surfaced as Britain’s central bank was tightening monetary policy to curb high inflation. Prime minister Liz Truss stepped down in the wake of the chaos, just weeks after taking the top job, saying she would leave as soon as the Conservative party holds a contest to replace her.

“The experiment’s over, if you will,” said JJ Kinahan, chief executive officer of IG Group North America, the parent of online brokerage tastyworks, in a phone interview. “So now we’re going to get a different leader,” he said. “Normally, you wouldn’t be happy about that, but since the day she came, her policies have been pretty poorly received.”

Meanwhile, the U.S. Treasury market is “fragile” and “vulnerable to shock,” strategists at Bank of America warned in a BofA Global Research report dated Oct. 20. They expressed concern that the Treasury market “may be one shock away from market functioning challenges,” pointing to deteriorated liquidity amid weak demand and “elevated investor risk aversion.”

Read: ‘Fragile’ Treasury market is at risk of ‘large scale forced selling’ or surprise that leads to breakdown, BofA says

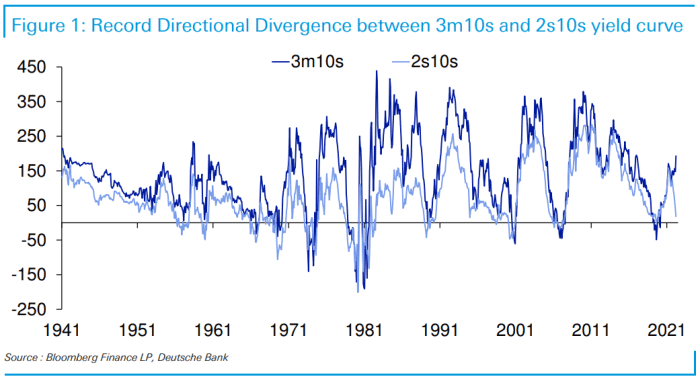

“The fear is that a debacle like the recent one in the U.K. bond market could happen in the U.S.,” Yardeni said, in its note Friday.

“While anything seems possible these days, especially scary scenarios, we would like to point out that even as the Fed is withdrawing liquidity” by raising the fed funds rate and continuing quantitative tightening, the U.S. is a safe haven amid challenging times globally, the firm said. In other words, the notion that “there is no alternative country” in which to invest other than the U.S., may provide liquidity to the domestic bond market, according to its note.

YARDENI RESEARCH NOTE DATED OCT. 21, 2022

“I just don’t think this economy works” if the yield on the 10-year Treasury

TMUBMUSD10Y,

4.228%

note starts to approach anywhere close to 5%, said Rhys Williams, chief strategist at Spouting Rock Asset Management, by phone.

Ten-year Treasury yields dipped slightly more than one basis point to 4.212% on Friday, after climbing Thursday to their highest rate since June 17, 2008 based on 3 p.m. Eastern time levels, according to Dow Jones Market Data.

Williams said he worries that rising financing rates in the housing and auto markets will pinch consumers, leading to slower sales in those markets.

Read: Why the housing market should brace for double-digit mortgage rates in 2023

“The market has more or less priced in a mild recession,” said Williams. If the Fed were to keep tightening, “without paying any attention to what’s going on in the real world” while being “maniacally focused on unemployment rates,” there’d be “a very big recession,” he said.

Investors are anticipating that the Fed’s path of unusually large rate hikes this year will eventually lead to a softer labor market, dampening demand in the economy under its effort to curb soaring inflation. But the labor market has so far remained strong, with an historically low unemployment rate of 3.5%.

George Catrambone, head of Americas trading at DWS Group, said in a phone interview that he’s “fairly worried” about the Fed potentially overtightening monetary policy, or raising rates too much too fast.

The central bank “has told us that they are data dependent,” he said, but expressed concerns it’s relying on data that’s “backward-looking by at least a month,” he said.

The unemployment rate, for example, is a lagging economic indicator. The shelter component of the consumer-price index, a measure of U.S. inflation, is “sticky, but also particularly lagging,” said Catrambone.

At the end of this upcoming week, investors will get a reading from the personal-consumption-expenditures-price index, the Fed’s preferred inflation gauge, for September. The so-called PCE data will be released before the U.S. stock market opens on Oct. 28.

Meanwhile, corporate earnings results, which have started being reported for the third quarter, are also “backward-looking,” said Catrambone. And the U.S. dollar, which has soared as the Fed raises rates, is creating “headwinds” for U.S. companies with multinational businesses.

Read: Stock-market investors brace for busiest week of earnings season. Here’s how it stacks up so far.

“Because of the lag that the Fed is operating under, you’re not going to know until it’s too late that you’ve gone too far,” said Catrambone. “This is what happens when you’re moving with such speed but also such size, he said, referencing the central bank’s string of large rate hikes in 2022.

“It’s a lot easier to tiptoe around when you’re raising rates at 25 basis points at a time,” said Catrambone.

‘Tightrope’

In the U.S., the Fed is on a “tightrope” as it risks over tightening monetary policy, according to IG’s Kinahan. “We haven’t seen the full effect of what the Fed has done,” he said.

While the labor market appears strong for now, the Fed is tightening into a slowing economy. For example, existing home sales have fallen as mortgage rates climb, while the Institute for Supply Management’s manufacturing survey, a barometer of American factories, fell to a 28-month low of 50.9% in September.

Also, trouble in financial markets may show up unexpectedly as a ripple effect of the Fed’s monetary tightening, warned Spouting Rock’s Williams. “Anytime the Fed raises rates this quickly, that’s when the water goes out and you find out who’s got the bathing suit” — or not, he said.

“You just don’t know who is overlevered,” he said, raising concern over the potential for illiquidity blowups. “You only know that when you get that margin call.”

U.S. stocks ended sharply higher Friday, with the S&P 500

SPX,

+2.37%,

Dow Jones Industrial Average

DJIA,

+2.47%

and Nasdaq Composite each scoring their biggest weekly percentage gains since June, according to Dow Jones Market Data.

Still, U.S. equities are in a bear market.

“We’ve been advising our advisors and clients to remain cautious through the rest of this year,” leaning on quality assets while staying focused on the U.S. and considering defensive areas such as healthcare that can help mitigate risk, said Ameriprise’s Saglimbene. “I think volatility is going to be high.”