TOKYO—The Bank of Japan made a surprise decision to let a benchmark interest rate rise to 0.5% from 0.25%, pushing the yen higher and ending a long period in which it was the only major central bank not to increase rates.

The

BOJ

said the yield on the 10-year Japanese government bond could rise as high as 0.5% from a previous cap of 0.25%. The central bank has set a target range around zero for the benchmark government bond yield since 2016 and used that as a tool to keep overall market interest rates low.

The 10-year yield, which had been stuck around 0.25% for months because of the central bank cap, quickly moved up to 0.46% in afternoon trading.

The yen rose in tandem. In Tuesday afternoon trading in Tokyo, one dollar bought between 133 and 134 yen, compared with more than 137 yen before the BOJ’s decision.

The Nikkei Stock Average, which had been slightly higher in the morning, was down more than 2% as investors digested the possibility that companies would have to pay higher interest on their debt. Also, the weak yen has pushed up profits for many exporters, so a stronger yen could be negative for stocks.

Gov.

Haruhiko Kuroda,

who is nearing the end of 10 years in office, is known for making moves that surprise the market, although he had made fewer of them in recent years.

Market players had anticipated that time might be running out on the Bank of Japan’s low-rate policy, but they generally didn’t expect Mr. Kuroda to move at the year’s final policy meeting.

The Bank of Japan’s statement on its decision Tuesday didn’t mention inflation as a reason to let the yield on government bonds rise as high as 0.5%. Instead, it cited the deteriorating functioning of the government bond market and discrepancies between the 10-year government bond yield and the yield on bonds with other maturities.

The bank said Tuesday’s move would “facilitate the transmission of monetary-easing effects,” suggesting it didn’t want the decision to be interpreted as monetary tightening.

The move is “a small step toward an exit” from monetary easing, said

Mitsubishi UFJ Morgan Stanley Securities

strategist Naomi Muguruma.

Ms. Muguruma said the BOJ needed to narrow the gap between its cap on the 10-year yield and where the yield would stand if market forces were given full rein.

“Otherwise magma for higher yields could build up, causing the yield to rise sharply when the BOJ actually unwinds easing,” she said.

Japan’s interest rates are still low compared with the U.S. and Europe, largely because its inflation rate hasn’t risen as fast. The Federal Reserve last week raised its benchmark federal-funds rate to a range between 4.25% and 4.5%—a 15-year high—while the European Central Bank said it would raise its key rate to 2% from 1.5%.

In the U.S., inflation has started to slow down recently but is still running above 7%. In Japan, consumer prices in October were 3.7% higher than they were a year earlier.

Japan has seen prices rise like other countries, owing to the impact of the war in Ukraine as well as the yen’s weakness. However, the pace of inflation is milder in Japan, where consumers tend to be highly price sensitive.

Write to Megumi Fujikawa at megumi.fujikawa@wsj.com

LONDON—The Bank of England extended support targeted at pension funds for the second day in a row, the latest attempt to contain a bond-market selloff that has threatened U.K. financial stability.

The central bank on Tuesday said it would add inflation-linked government bonds to its program of long-dated bond purchases, after an attempt on Monday to help pension funds failed to calm markets.

“Dysfunction in this market, and the prospect of self-reinforcing ‘fire sale’ dynamics pose a material risk to U.K. financial stability,” the BOE said.

The yield on a 30-year U.K. inflation-linked bond has soared above 1.5% this week, up from 0.851% on Oct. 7, according to

Tradeweb.

Just weeks ago, the yield on the gilt, as U.K. government bonds are known, was negative. Because yields rise as prices fall, the effect has been punishing losses for bond investors.

Turmoil in the U.K. bond market created a feedback loop that left investors like pension funds short on cash and rippled out into other markets. WSJ’s Chelsey Dulaney explains the type of investment at the heart of the crisis. Illustration: Ryan Trefes

On Tuesday, after the BOE expanded the purchases, the yield on inflation-linked gilts held mostly steady but at the new, elevated levels. The central bank said it bought roughly £2 billion, equivalent to about $2.21 billion, in inflation-linked gilts, out of a £5 billion daily capacity.

The bank’s bond purchases, however, are meant to run out on Friday. The Pensions and Lifetime Savings Association, a trade body that represents the pension industry, urged the central bank on Tuesday to extend its purchases until the end of the month.

The near-daily expansion of the Bank of England’s rescue plan highlighted the challenges facing central banks in stamping out problems fueled by a once-in-a-generation increase in inflation and interest rates. It also raised questions about whether the BOE was providing the right medicine to address the problem.

The turmoil sparked fresh demands on Monday for pension funds to come up with cash to shore up LDIs, or liability-driven investments, derivative-based strategies that were meant to help match the money they owe to retirees over the long term.

LDIs were at the root of the bond selloff that prompted the BOE’s original intervention. Pension plans in late September saw a wave of margin calls after Prime Minister

Liz Truss’s

government announced large, debt-funded tax cuts that fueled an unprecedented bond-market selloff.

The BOE launched its original bond-purchase program on Sept. 28, but it only restored calm for a couple of days before selling resumed. An expansion of the program on Monday backfired, with yields again soaring higher.

The selloff on Monday was “very reminiscent of two weeks ago,” said

Simeon Willis,

chief investment officer of XPS, a company that advises pension plans.

LDI strategies use leveraged financial derivatives tied to interest rates to amplify returns. The outsize moves in U.K. bond markets last month led to huge collateral calls on pensions to back up the leveraged investments. The pension funds have sold other assets, including government and corporate bonds, to meet those calls, adding to pressure on yields to rise and creating a spiral effect on markets.

Pensions are typically big holders of inflation-linked government bonds, which help protect the plans from both inflation and interest-rate changes. But these weren’t eligible in the BOE’s bond-buying program until Tuesday.

The U.K. helped pioneer bonds with payouts linked to inflation, sometimes referred to as linkers, in the 1980s. Linkers were originally sold exclusively to pensions, but the U.K. opened them to other investors over the years.

Pensions remain a dominant force in the market because the bonds offer long-term protection against both inflation and interest-rate changes. Their outsize role left the market vulnerable to shifts in pension-fund demand like that seen in recent weeks.

Adam Skerry, a fund manager at Abrdn with a focus on inflation-linked government bonds, said his firm has struggled to trade those assets in recent days.

“We were trying to sell some bonds this morning, and it was virtually impossible to do that,” he said. “The LDI issue that’s facing the market, the fact that the market is moving to the degree that it did, particularly yesterday, suggests that there’s still an awful lot [of selling] there.”

Pensions have also appeared hesitant to sell their bonds to the BOE, reflecting a mismatch in what the central bank is offering and what the market needs.

“The way that the bank has structured this intervention is they can only buy assets if people put offers into them, but nobody is putting offers in,” said Craig Inches, head of rates and cash at Royal London Asset Management. He said the pension funds would rather sell their riskier assets, including corporate bonds or property.

Mr. Willis of XPS said many pensions want to hold on to their government bonds because it helps protect pensions against changes in interest rates, which impact the way their liabilities are valued.

“If they sell gilts now, they’re doing it in the likelihood that they’ll need to buy them back in the future at some point and they might be more expensive, and that’s unhelpful,” he said.

Also plaguing the program: Pension funds are traditionally slow-moving organizations that make decisions with multidecade horizons. The market turmoil has hurtled them into the warp-speed-style moves usually reserved for traders at swashbuckling hedge funds.

To make decisions about the sale of assets, industry players describe a game of telephone playing out among trustees, investment advisers, fund managers and banks. Pension funds spread their assets among multiple managers, which are in turn held by separate custodian banks. Calling everyone for the necessary signoffs is creating a lengthy and involved process.

To give themselves more time, pension funds are pushing the BOE to extend the bond-buying program at least to the end of the month. That is when the U.K.’s Treasury chief,

Kwasi Kwarteng,

is expected to lay out the government’s borrowing plans for the coming year.

The Institute for Fiscal Studies, a nonpartisan think tank that focuses on the budget, warned Tuesday that borrowing is likely to hit £200 billion in the financial year ending March, the third highest for a fiscal year since World War II and £100 billion higher than planned in March of this year. Increased borrowing increases the supply of bonds and generally causes bond yields to rise.

Mr. Kwarteng on Tuesday declared his confidence in BOE Gov. Andrew Bailey as he faced questions from lawmakers for the first time in his new job.

“I speak to the governor very frequently and he is someone who is absolutely independent and is managing what is a global situation very effectively,” he said.

—Caitlin Ostroff contributed to this article.

Write to Chelsey Dulaney at Chelsey.Dulaney@wsj.com, Anna Hirtenstein at anna.hirtenstein@wsj.com and Paul Hannon at paul.hannon@wsj.com

LONDON—The Bank of England expanded its support of pension funds at the heart of the U.K.’s bond-market crisis even as borrowing costs leapt higher, a sign that stress in the financial system wasn’t going away.

The U.K.’s central bank said Monday that it would increase the daily amounts it was willing to buy in long-dated bonds before ending the program as scheduled on Friday. It also unveiled two types of lending facilities aimed at freeing up cash for pension funds beyond the end of the bond buying.

The moves failed to calm markets, with yields on 30-year U.K. gilts, as government bonds are known, jumping to as high as 4.64%, from 4.39% on Friday. Outside the past two weeks such moves would be considered unusually large for a single day.

The Bank of England launched its initial foray into markets on Sept. 28 when it offered to buy up to £5 billion, or around $5.55 billion, a day of long-dated government bonds. The program was aimed at stanching the damage from a furious selloff in U.K. government debt over previous days in the aftermath of a surprise package of tax cuts announced by the government.

“The underlying message is that there’s been too little risk reduction so far,” said Antoine Bouvet, senior rates strategist at ING. “There’s a message to pension funds and potential sellers that the window is closing and they need to hurry up.”

Turmoil in the U.K. bond market created a feedback loop that left investors like pension funds short on cash and rippled out into other markets. WSJ’s Chelsey Dulaney explains the type of investment at the heart of the crisis. Illustration: Ryan Trefes

He attributed Monday’s bond selloff to disappointment among investors who had expected the BOE to extend the bond-buying facility.

The original intervention in late September at first calmed markets, with government bond yields plunging in response. But yields shot back up in recent days after it appeared the bank was buying far less than the £5 billion a day, a possible sign that the program wasn’t working as intended.

In the history of crisis interventions, central banks often have to make multiple stabs at solving problems with different types of bond buying or lending programs before markets become convinced that a viable backstop has been created. During the Covid-19 meltdown in March 2020, the Federal Reserve expanded its lending programs several times before calm was restored.

The BOE said it would increase the daily amount of purchases on offer until the program ends, starting with £10 billion Monday, though it was unclear if there would be take-up by distressed sellers.

Newsletter Sign-up

Real Time Economics

The latest economic news, analysis and data curated weekdays by WSJ’s Jeffrey Sparshott.

The lending programs announced Monday included what the BOE called a temporary expanded collateral repo facility. This lends cash to pension funds in exchange for an expanded menu of collateral than was previously available to the pension plans, including index-linked gilts, whose returns are tied to inflation, and corporate bonds.

The operations would be processed through banks working on behalf of the pension funds. The BOE also made an existing, permanent repo lending facility available to banks acting to help pension-fund clients.

The crisis centers on a corner of the market known as LDIs, or liability-driven investments. LDIs became popular in recent years among U.K. defined-benefit pension plans to make enough money in the long term to match what they owed retirees. These strategies use financial derivatives tied to interest rates.

LDIs also contain leverage, or borrowing, that amplifies pension-fund investments by as much as six or seven times. When the long-dated U.K. government bond yield that undergird LDI investments surged more than they ever have in a single day at the end of September, LDI fund managers required pension funds to post massive amounts of fresh collateral to back up the investments.

To generate that collateral, pension funds have been selling non-LDI bonds, stocks and other investments.

In a letter to lawmakers last week, BOE Deputy Gov.

Jon Cunliffe

said the bank acted to stop forced selling by LDI investors and a “self-reinforcing spiral of price falls.”

The point of the new lending programs and the bond buying is to make it easier for the pension funds to drum up cash so they can pay down the leverage on their LDI funds without causing wider market disruption.

Newsletter Sign-up

Markets

A pre-markets primer packed with news, trends and ideas. Plus, up-to-the-minute market data.

“The Bank of England has been listening to schemes and the challenges they’re facing right now in still struggling to access liquidity quickly enough to recapitalize LDI,” said Ben Gold, head of investment at

XPS Pensions Group,

a U.K. pensions consultant. The measures also help funds avoid having to sell assets at poor prices, he said.

Mr. Gold estimates that it is going to take between £100 billion and £150 billion for the industry to shore up its collateral on LDI funds.

“I would estimate that we’re probably about halfway there,” he said. “There is still a lot of activity that’s needed to get it done before 14th October.”

Soaring inflation and expectations of swelling government bond issuance pushed bond yields up sharply in recent months. Investors in U.K. government bonds were troubled by the tax cuts announced by Prime Minister

Liz Truss’s

government in part because they weren’t accompanied by a customary analysis of the impact on borrowing by the independent budget watchdog.

U.K. Treasury chief

Kwasi Kwarteng

on Monday said he would announce further budgetary measures on Oct. 31 that will be accompanied by forecasts from the Office for Budget Responsibility, which provides independent analysis of government spending. He previously said that wouldn’t happen until Nov. 23.

—Caitlin Ostroff contributed to this article.

Write to Paul Hannon at paul.hannon@wsj.com, Chelsey Dulaney at Chelsey.Dulaney@wsj.com and Julie Steinberg at julie.steinberg@wsj.com

U.S. stock futures fell, oil prices dropped and bond yields ticked lower after major indexes rallied to start the trading week, with recent volatility in markets showing few signs of abating.

Futures for the S&P 500 declined 1.4% Wednesday. Contracts for the tech-focused Nasdaq-100 contracted 1.6% and futures for the Dow Jones Industrial Average receded 1.2%. U.S. stocks rallied Tuesday off their worst week since March 2020, offering investors a reprieve from a recent stretch of whipsaw trading that had sent stocks and cryptocurrencies falling.

Stocks have seen sharp moves in recent weeks following aggressive interest-rate increases from the Federal Reserve, with more expected, as central banking officials seek to put a cap on inflation. Investors have scrambled to unload riskier assets amid growing fears that quick tightening of financial conditions will plunge the U.S. economy into a recession. The S&P 500 is on track for its worst first half of the year in decades, according to Deutsche Bank research analysts.

Recession fears weighed on shares of energy, autos and travel companies in premarket and European trading.

Occidental Petroleum

declined 4.1% premarket, while

Halliburton

shares fell 3.9%.

United Airlines Holdings

fell 3.3%.

The

Cboe

Volatility Index—Wall Street’s so-called fear gauge, also known as the VIX—rose 3.6% to 31.29.

Investors sought assets viewed as safer to hold Wednesday, such as the U.S. dollar and U.S. government debt. The WSJ Dollar Index, which measures the dollar against a basket of 16 currencies, added 0.2%.

In bond markets, the yield on the benchmark 10-year Treasury note ticked down to 3.228% from 3.304% Tuesday. Yields fall when prices rise.

“There is certainly an anxiousness in markets and that’s playing through in volatility,” said

Edward Park,

chief investment officer at U.K. investment firm Brooks Macdonald, adding that investors are likely awaiting fresh inflation data or a central bank meeting to assess their future trades.

Fed Chairman

Jerome Powell

is set to testify before Congress on both Wednesday and Thursday. Investors will be watching his words for clues about the future path of monetary policy.

In energy markets, Brent crude, the international benchmark for oil prices, dropped 4.4% to $109.63 a barrel. President Biden is planning to call for a temporary suspension of the federal gasoline tax, The Wall Street Journal reported. Energy prices remain near historically high levels as Russia’s invasion of Ukraine has caused Western nations to move rapidly away from Moscow’s supplies.

“This is a reminder for markets that governments are unlikely to sit back and take a higher oil prices,” Mr. Park said.

The dollar value of bitcoin, the world’s largest cryptocurrency by market value, edged down 2.1% from its 5 p.m. ET level Tuesday to trade at $20,393.06, according to CoinDesk. Cryptocurrencies have fallen recently amid broad investor desire to get out of speculative assets and concerns about the future of some crypto companies.

U.S. stocks rallied Tuesday off their worst week since March 2020.

Photo:

Seth Wenig/Associated Press

Overseas, the pan-continental Stoxx Europe 600 declined 1.6%, with losses led by the basic resources, oil-and-gas and autos sectors.

In Asia, major indexes closed with losses. South Korea’s Kospi declined 2.7%, China’s Shanghai Composite fell 1.2% and Japan’s Nikkei 225 edged down 0.4%.

Write to Caitlin Ostroff at caitlin.ostroff@wsj.com

U.S. stocks were higher Friday, putting major indexes on course to extend the whipsaw moves that have injected fresh volatility into markets this week.

The S&P 500 rose 0.7%. The Dow Jones Industrial Average added 0.3%, and the Nasdaq Composite climbed 1.4%. All three major indexes fell Thursday, closing at their lowest levels since 2020. Thursday’s decline reversed a rally in stocks Wednesday.

Stock indexes are on track to finish the week with sharp losses as investors have tried to assess inflation, central banks’ response to it and the outlook for the global economy. The Federal Reserve earlier this week approved the largest interest-rate increase since 1994 and signaled it would continue lifting rates this year at the most rapid pace in decades to fight inflation.

Recent rate increases have reversed a prior cycle of loosening monetary policy that allowed prices for both stocks and bonds to rally in recent years. Prospects for repeated rate rises throughout the rest of the year have caused investors to sell out of both assets and lent to fears that rapid tightening could reduce growth. U.S. mortgage rates recently reached their highest level in more than 13 years. Recent economic data reports have shown sharp declines in key sectors.

“The central banks, who have been our friends for a very long time, are telling us we should expect pain,” said Hani Redha, a portfolio manager at PineBridge Investments. “That inflation number is the only thing that matters right now. Even if we see growth slowing a lot, that will not be enough to cause the Fed to change course.”

Mr. Redha said it is possible that inflation could still climb further in the coming months as energy prices remain elevated. Brent crude, the international benchmark for oil prices, edged down 2.4% to $117.03 a barrel.

European natural-gas prices edged down 0.6% Friday, putting them up almost 50% for the week. Moscow’s move to slash natural-gas exports to Europe this week has pitched the continent’s energy crisis into a dangerous new phase that threatens to drain vital fuel supplies and kneecap the continent’s economy.

Where in Americans’ household budgets is inflation hitting the hardest? WSJ’s Jon Hilsenrath traces the roots of the rising prices to learn why some sectors have risen so much more than others. Photo Illustration: Laura Kammermann/WSJ

Signs remained that investors sought assets viewed as safe to hold, such as the U.S. dollar and U.S. government bonds. The WSJ Dollar Index, which measures the greenback against a basket of 16 currencies, rose 0.9%. In bond markets, the yield on benchmark 10-year Treasurys ticked down to 3.262% from 3.303% Thursday. Yields fall as prices rise.

The dollar value of bitcoin and other cryptocurrencies showed tepid signs of stabilizing after tumbling sharply over the 10 days prior. Bitcoin was roughly unchanged from its 5 p.m. ET level Thursday to trade at $20,637 Friday. Cryptocurrencies have been hit by rising interest rates that are sapping appetite for riskier assets, and concerns about select projects and companies in the crypto ecosystem.

Shares of

Adobe

fell 4.1% after the provider of software for creativity, marketing, and documents gave softer-than-expected guidance.

Overseas, the pan-continental Stoxx Europe 600 added 0.7%. Shares of commodity mining and trading giant

Glencore

added 0.8% in London trading after the company raised price and cost guidance for its coal operations and said that its trading business is outperforming expectations.

Stocks on Wall Street closed sharply lower on Thursday, with Dow Jones Industrial Average below 30000.

Photo:

BRENDAN MCDERMID/REUTERS

In Asia, the

Bank of Japan

maintained ultralow interest rates on Friday, confirming that it won’t join the Federal Reserve and other major global central banks in tightening monetary policy. Japan’s Nikkei 225 stock index fell 1.8% and the Japanese yen fell 1.8% against the dollar.

South Korea’s Kospi edged down 0.4%, while China’s Shanghai Composite added 1%.

Write to Caitlin Ostroff at caitlin.ostroff@wsj.com

U.S. stocks flipped higher Monday as government-bond yields retreated and investors took the opportunity to scoop up shares of beaten-down technology and other growth stocks.

The S&P 500 climbed 24.34 points, or 0.6%, to 4296.12 after dropping nearly 1.7% earlier in the session. The Dow Jones Industrial Average advanced 238.06 points, or 0.7%, to 34049.46.

The tech-heavy Nasdaq Composite Index rose 165.56 points, or 1.3%, to 13004.85.

Twitter

shares rose 5.7% after the social-media company accepted

Elon Musk’s

$44 billion takeover deal.

All three indexes had opened lower after Chinese shares suffered their worst selloff in more than two years as Beijing sticks to its zero-Covid strategy while faced with increasing cases in major cities. Oil prices fell, at one point dipping below $100 a barrel, before staging an afternoon rally.

A decline in bond yields signaled to investors that the Federal Reserve may not move to raise interest rates as aggressively as feared, investors said.

“Rates had been weighing against the market,” said

Jack Ablin,

chief investment officer of Cresset Capital. “Now what we’re seeing is a reversal of that trend.”

The yield on the benchmark 10-year Treasury note ticked down to 2.825% Monday from 2.905% Friday as investors sought safer assets to hold. Yields and prices move inversely.

“I think a lot of growth stocks have been punished too severely,” said

Brian Price,

head of investment management for Commonwealth Financial Network. “Part of what we’re seeing may be a reversal of that. Longer-term rates have just moved so far.

“The market is stepping back and assessing if they should have moved so fast. And falling interest rates tend to help growth stocks.”

Twitter rose $2.77 to $51.70.

Microsoft

climbed $6.69, or 2.4%, to $280.72, while Google parent

Alphabet

added $68.77, or 2.9%, to close at $2,461.48

Meantime, the S&P 500’s energy sector was the biggest decliner, falling 3.3%.

Schlumberger

fell $2.96, or 7.1%, to $38.69.

Halliburton

dropped $2.36, or 6.3%, to $35.33.

APA,

Apache’s parent company, slipped $1.63, or 4%, $39.08.

Investors are worried that strict policies China has in place to combat Covid-19 will further disrupt global supply chains. But the extended lockdowns, and a slowdown in China’s economy, also could crimp global demand for oil, investors said.

The Shanghai Composite and CSI 300 indexes fell 5.1% and 4.9%, respectively. Those were the largest single-day percentage declines for both benchmarks since February 2020, in the early days of the pandemic.

The offshore yuan fell about 1% to trade at about 6.59 per dollar. That was the lowest since November 2020, according to FactSet. The decline built on a selloff last week that ended months of relative stability.

As Shanghai remains locked down amid China’s biggest Covid-19 outbreak, residents are taking to social media to vent about a shortage of food or they are bartering with neighbors. Anxiety and hunger are prompting many to question Beijing’s pandemic strategy. Photo: Chinatopix Via AP

“The problem with inflation is it can get embedded and we see inflation getting quite sticky,” said

Sebastian Mackay,

a multiasset fund manager at Invesco. “What we’re seeing is a combination of the war in Ukraine and the lockdown in China causing supply issues.”

Limitation of movement in China also could sap demand for oil. Brent crude, the international benchmark for oil, fell 4.1% to $102.32 a barrel. Oil prices still remain near historically high levels due to concerns about disruptions to energy markets from Russia’s invasion of Ukraine.

In other corporate news, shares of

Coca-Cola

rose 69 cents, or 1.1%, to $65.94. The company said it logged higher sales for the latest quarter as demand held up in the face of price increases.

Advanced Micro Devices

added $2.55, or 2.9%, to $90.69 after a Raymond James analyst lifted his rating on the chip maker’s shares.

Elevated inflation has caused the Federal Reserve to increase efforts to combat it. Last week, Fed Chairman

Jerome Powell

signaled that the central bank is ready to tighten monetary policy more quickly and indicated that it was likely to raise interest rates by a half-percentage point at its meeting in May.

Money managers are worried that the Fed’s aggressive interest-rate increases could slow economic growth or even tip the economy into recession. This could lead to a situation where the Fed has to raise interest rates in the short term but cut them in the long term, Mr. Mackay said.

On Monday, the

Cboe

Volatility Index—Wall Street’s so-called fear gauge, also known as the VIX—approached its highest level since mid-March before retreating to 27.02.

The Dow Jones Industrial Average on Friday posted its worst one-day percentage change since October 2020.

Photo:

BRENDAN MCDERMID/REUTERS

Gold futures fell 2% to $1,893.20 a troy ounce. While gold is historically seen as an inflation hedge, it pays no yield, making it less attractive than government bonds in a time of rising interest rates. The cost of buying gold, which is denominated in dollars, also is more expensive for foreign investors when the dollar strengthens.

Overseas, the pan-continental Stoxx Europe 600 dropped 1.8%. South Korea’s Kospi declined 1.8%, and Japan’s Nikkei 225 contracted 1.9%.

How the Biggest Companies Are Performing

Write to Caitlin Ostroff at caitlin.ostroff@wsj.com and Justin Baer at justin.baer@wsj.com

U.S. stocks fell and a selloff in government bonds stabilized Friday, after the latest sign that the Federal Reserve will tighten monetary policy aggressively to fight inflation.

The S&P 500 fell 1.3% in morning trading, while the technology-heavy Nasdaq Composite declined 0.8%. The Dow Jones Industrial Average dropped 500 points, or 1.4%. On Thursday, major U.S. stock indexes finished with losses. All three indexes were on course to finish the week in the red.

This week’s steep rise in government bond yields showed signs of steadying, with the yield on the 10-year Treasury note recently at 2.895% after ending at 2.917% Thursday. Earlier Friday, yields staged a climb before reversing course. Yields rise when bond prices decline.

Concerns about inflation and the pace of monetary tightening by the Fed have remained at the forefront of investors’ minds this week and have helped lead to swings in major stock indexes. On Thursday, Fed Chairman

Jerome Powell

gave investors a clear signal that the central bank is ready to tighten monetary policy more quickly and indicated it was likely to raise interest rates by a half-percentage point at its meeting in May.

A rate increase next month, following the Fed’s quarter percentage point increase in March, would mark the first time since 2006 that the central bank increased its policy rate at back-to-back meetings.

Mr. Powell’s comments injected fresh volatility into a stock market that has been whipsawed this year by the war in Ukraine, soaring inflation and rising Covid-19 cases in China. Many traders are now worried that the Fed’s tightening cycle could tip the economy into a recession as consumers are already feeling uneasy about the economy. Next week, investors will parse fresh figures from The University of Michigan on April consumer sentiment.

Federal Reserve Chairman Jerome Powell indicated on Thursday that the central bank was likely to raise interest rates by a half percentage point at its meeting in May. Photo: Samuel Corum/Getty Images

“I think what you’re seeing is consumers are becoming much more hesitant,” said

Susannah Streeter,

senior investment and markets analyst at Hargreaves Lansdown. “It’s a tricky tightrope that central-bank policy makers are having to tread right now. They need to put a lid on that boiling pot of inflation but they don’t want steam to be driven out of the economy completely.”

Still, for now, investors have been encouraged by strong first-quarter earnings. Of the companies that have reported so far, nearly 80% have beat analyst expectations. That has helped provide some stability to the U.S. stock market.

Shares of

HCA Healthcare

fell about 17%, on pace for its largest percent decrease since March 2020, after the hospital chain lowered its guidance for the year. The company said volume and revenue for the first quarter was offset by higher-than-expected inflationary pressures on labor costs.

The healthcare-company’s decline is worrying investors, who consider it be a defensive stock. Money managers often bet that consumers would spend money on hospital bills before any discretionary purchases.

“Usually when the economy’s slowing down, or there is a perception it’ll slow down, there are obvious sectors to hide in. Those traditional sectors aren’t as safe from earnings basis as they are historically because they still are going to have negative impact from inflation,” said

Tavis McCourt,

institutional equity strategist at Raymond James.

Shares of airlines rose.

United Airlines Holdings

added 2.3% and

American Airlines Group

gained 0.5%. On Thursday, American said its sales hit a record in March, the first month since the pandemic began in which the airline’s total revenue surpassed 2019 levels. United said it has been able to pass the rise in fuel prices on to consumers.

Shares of

American Express

fell 1.8% after the credit-card company logged first-quarter net income of $2.10 billion, down from $2.24 billion a year earlier, even as spending on travel and entertainment surged.

Gap shares fell 19% in early trading Friday, after the retailer cut its fiscal first-quarter guidance and announced the departure of the president and chief executive of its Old Navy business.

Kimberly-Clark

jumped 9 after the maker of Huggies diapers and Cottonelle toilet paper raised its sales-growth projection for 2022 and said that first-quarter sales increased compared with the year before.

Stocks on Wall Street declined on Thursday after Federal Reserve Chairman Jerome Powell signaled the central bank would raise interest rates by a half-percentage point at its next meeting.

Photo:

Courtney Crow/Associated Press

In commodities, Brent crude, the international benchmark for oil, fell 1.6% to $106.23 a barrel.

In the currency markets, the ICE U.S. Dollar Index, which tracks the currency against a basket of others, gained 0.6%, on pace to notch a gain for the week. Including Friday, the index has climbed for all but two sessions in April, thanks to geopolitical concerns and looming interest-rate increases by the Fed.

In overseas markets, the pan-continental Stoxx Europe 600 fell 1.7% dragged down by technology companies including German software companies SAP and

TeamViewer,

which fell 3.4% and 3.8%, respectively. In contrast, Swiss cement maker

Holcim

climbed 4.8% after the company reported sales growth and upgraded its outlook for the year.

On Friday, data from the U.K.’s Office for National Statistics showed signs of consumer skittishness. U.K. retail sales volumes fell sharply last month, weakening by 1.4%. That sent the British pound falling 1.1% against the dollar to its lowest level since 2020. London’s FTSE 100 stock index fell 0.7%.

In Asia, Hong Kong’s Hang Seng lost 0.2% and Japan’s Nikkei 225 fell 1.6%. The Shanghai Composite, in contrast, bucked the trend, rising 0.2%.

Write to Caitlin McCabe at caitlin.mccabe@wsj.com and Hardika Singh at hardika.singh@wsj.com

Uncertainty about Federal Reserve policy and the war in Ukraine pushed the S&P 500 to a weekly loss and stoked a selloff in the government bond market.

The broad stock-market gauge lost 11.93 points, or 0.3%, to 4488.28 Friday. The tech-heavy Nasdaq Composite declined 186.30 points, or 1.3%, to 13711.00. The blue-chip Dow Jones Industrial Average reversed early losses to close up 137.55 points, or 0.4%, to 34721.12.

All three major indexes ended the week with losses. The S&P 500 snapped a three-week winning streak that had sent it toward its best performance since November 2020, losing 1.3%. The Dow and Nasdaq lost 0.3% and 3.9%, respectively.

Meanwhile, the yield on the benchmark 10-year Treasury note jumped to the highest level since March 2019 as bond prices tumbled.

Throughout the week, investors remained preoccupied with commentary from Federal Reserve officials as well as the minutes from the central bank’s March policy meeting, Those minutes showed that policy makers had considered raising interest rates and unwinding its balance sheet faster, driving stocks lower.

U.S. government bond yields influence the cost of borrowing, from mortgages to student loans. WSJ explains how they work and why they are so crucial to the economy. Photo illustration: Tom Grillo/WSJ

Federal Reserve Bank of St. Louis President

James Bullard

said Thursday that the central bank is behind on its mission to tame inflation and will likely have to act fairly forcefully to get price pressures under control.

The swings in assets across the market highlight how murky the path of the economy remains for many investors, who are trying to pick the winners and losers of the rising interest-rate regime and grappling with surging commodity prices world-wide.

“The Fed has been the number-one story and that continues,” said

James Athey,

an investment manager at

Abrdn.

“The effect of the sort of tightening that has been discussed, that has a history of being very destabilizing.”

A rapid jump in bond yields has led some investors and analysts to wonder whether the rise in yields will chip away at stock returns, and at what point investors will opt to ditch stocks in favor of bonds. Some investors have grown worried that the central bank’s interest rate hikes will drive a recession just two years after the U.S. exited the last downturn.

The yield on the benchmark 10-year Treasury note rose for a sixth consecutive day to 2.713%. Shorter-dated bond yields also advanced, with the two-year yield rising to 2.518% and notching a fifth consecutive week of gains. The two-year yield recorded its biggest five-week gain since May 1987.

“Although yield levels are still fairly low, if they rise fast enough, can equities withstand such a monetary shock?” wrote

Jim Paulsen,

chief investment strategist at the Leuthold Group, in a note to clients on Thursday.

Mr. Paulsen said that in the last three months, yields have risen faster than nearly 97% of all three-month periods since 1950. Still, he said, stocks have typically done well when the 10-year Treasury yield has been below 3% and until it rises to around 4%.

Some tech heavyweights that had rebounded lately pulled back in recent sessions.

Amazon.com

shares lost 5.6% this week, while Google-parent

Alphabet

shed 4.9%. The tech-heavy Nasdaq badly underperformed its peers, continuing a trend from earlier in the year.

Investors have also had to analyze mixed signals stemming from different parts of the market. The bond market, for example, was recently flashing a signal that a recession may be on the horizon. And transportation stocks, which are often viewed as an indicator of the health of the economy, have been tumbling.

The Dow Jones Transportation Average, which tracks 20 large U.S. companies ranging from delivery giant

United Parcel Service

to railroad operator

Union Pacific,

has fallen 11% to start the month, while the Dow industrials broadly are up about 0.1%. Companies that operate things like trains and planes tend to see higher demand when consumers are ramping up spending on travel and other goods and the economic outlook is brighter.

Traders worked on the floor of the New York Stock Exchange on Thursday.

Photo:

David L. Nemec/Associated Press

The war in Ukraine has also continued to weigh on markets. Allegations of war crimes by Russian troops against civilians prompted a new round of sanctions from the U.S. and the European Union this week. The United Nations General Assembly on Thursday voted to suspend Russia from its Human Rights Council.

Despite the recent volatility and signals from the bond market, major indexes have rapidly ascended from their lows in March. The S&P 500 has gained 7.6% since its March low in a broad-based rally. Some investors have said that stocks remain attractive even though Treasury yields have jumped.

“If you want to grow your buying power over the next 10 years, I can’t think of a better place to do it than equities,” said

Dev Kantesaria,

founder of Valley Forge Capital. “We have been buying more of the companies that are in our portfolio. We are close to 0% cash.”

Newsletter Sign-up

Markets

A pre-markets primer packed with news, trends and ideas. Plus, up-to-the-minute market data.

In commodities, prices for palladium and platinum jumped after the body that oversees London’s market for the metals said it would bar metal produced by two major refining companies owned by the Russian government. Meanwhile, the United Nations on Friday said global food prices hit a record high in March.

Oil prices edged lower, with global benchmark Brent crude dropping for the second consecutive week to trade at $102.78 after losing 1.5%. Traders are assessing the impact of sanctions and self-sanctioning measures by energy companies on Russian oil exports and the release of strategic reserves by member nations of the International Energy Agency.

Overseas, the pan-continental Stoxx Europe 600 closed Friday up 1.3%, finishing the week ahead 0.6%. The FTSE 100 ended the week up 1.7%, while Germany’s DAX index fell 1.1%.

In Asia, most major benchmarks closed up. The Shanghai Composite Index added 0.5% while Hong Kong’s Hang Seng Index rose 0.3%. Japan’s Nikkei 225 ticked up 0.4%.

Write to Anna Hirtenstein at anna.hirtenstein@wsj.com and Gunjan Banerji at gunjan.banerji@wsj.com

Blink and you missed it, but the yield on the 2-year Treasury note traded briefly above the yield on the 10-year note Tuesday afternoon, temporarily inverting the yield curve and triggering recession warning bells.

Data shows that it hasn’t paid in the past to abandon stocks the moment the Treasury yield curve turns upside down, with short term yields higher than longer term yields.

Not a good timing tool

“While a good indicator of future economic woes, an inverted yield curve has not been a very good timing tool for equity investors,” wrote Brian Levitt, global market strategist at Invesco in a March 24 note.

See: A key part of the Treasury yield curve has finally inverted, setting off recession warning — here’s what investors need to know

“For example, investors who sold when the yield curve first inverted on Dec. 14, 1988, missed a subsequent 34% gain in the S&P 500 index,” Levitt wrote. “Those who sold when it happened again on May 26, 1998, missed out on 39% additional upside to the market,” he said. “In fact, the median return of the S&P 500 index from the date in each cycle when the yield curve inverts to the market peak is 19%.” (See table below.)

Invesco

Investors certainly didn’t head for the hills Tuesday. U.S. stocks ended with strong gains, building on a bounce from early March lows and even propelling the S&P 500

SPX,

+1.23%

to an exit from the market correction it entered in February. The Dow Jones Industrial Average

DJIA,

+0.97%

jumped 338 points, or 1%, while the Nasdaq Composite

COMP,

+1.84%

advanced 1.8%.

Read: S&P 500 exits correction: Here’s what history says happens next to U.S. stock-market benchmark

Inversions and what they mean

Normally the yield curve, a line that measures the yields across all maturities, slopes upward given the time value of money. An inversion of the curve signals that investors expect longer term rates to be below near-term rates, a phenomenon widely taken as a signal of a potential economic downturn.

But there’s a lag there, too. Levitt noted that the data, going back to 1965, show the median length of time between an inversion and a recession has been 18 months — matching the median stretch between the onset of an inversion and an S&P 500 peak.

Moreover, researchers have argued that a persistent inversion is necessary to send a signal, something that hasn’t occurred yet, but remains widely expected.

Which curve?

An inversion of the 2-year

TMUBMUSD02Y,

2.322%

/10-year

TMUBMUSD10Y,

2.410%

measure of the yield curve has preceded all six recessions since 1978, with just one false positive, said Ross Mayfield, investment strategy analyst at Baird, in a Monday note.

But the 3-month/10-year spread is seen as even, if only slightly, more reliable and has been more popular among academics, noted researchers at the San Francisco Fed. And Fed Chairman Jerome Powell earlier this month expressed a preference for a more short-term oriented measure that measures 3-month rates versus expectations for 3-month rates 18 months in the future.

The 3-month/10-year spread, meanwhile, is “far from inverted,” Mayfield noted.

See: Stock-market investors should watch this part of the yield curve for the ‘best leading indicator of trouble ahead’

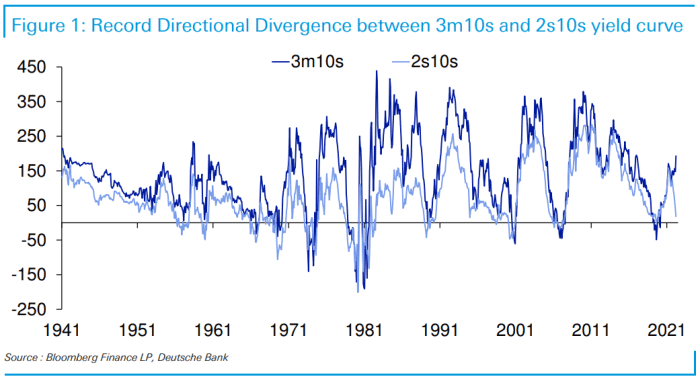

Indeed, the divergence between the two closely followed measures of the curve has been a head scratcher for some market watchers.

“The remarkable thing is that the two have always gone hand in hand directionally until around December 2021 when 3m/10s started to steepen as 2s/10s collapsed,” said Jim Reid, strategist at Deutsche Bank, in a Tuesday note (see chart below).

Deutsche Bank

“There has never been such a directional divergence possibly because the Fed [has] never been as behind the ‘curve’ as they are today,” Reid said. “If market pricing is correct, they will rapidly catch up over the next year so it’s possible that in 12 months’ time” the 3-month/10-year measure will be flat as short-term rates rise as the Fed hikes its benchmark policy rates.

The takeaway, Mayfield wrote, is that the yield curve remains a powerful indicator and is at the very least signaling a cooling economy.

“Volatility should remain heightened and the bar for investing success is raised. But in the end, we think it is worth taking the time to digest the larger picture and not rely on any single indicator,” he said.

In One Chart: ‘The dam finally broke’: 10-year Treasury yields spike to breach top of downward trend channel seen since mid-1980s

U.S. government bonds yields rose sharply Wednesday after the Federal Reserve said it would lift short-term interest rates and signaled they could reach nearly 2% by the end of the year.

In recent trading, the yield on the benchmark 10-year U.S. Treasury note was 2.239%, according to Tradeweb, compared with 2.160% Tuesday. The two-year Treasury yield—which is especially sensitive to changes in monetary policy—was recently 1.989%, up from 1.855% Tuesday.

Yields, which rise when bond prices fall, had drifted higher earlier in the session but added to those gains immediately after the Fed released its latest policy statement, which stated that the central bank would raise its benchmark federal-funds rate by a quarter percentage point to a range between 0.25% and 0.5% from near zero. A forecast for interest rates showed officials think rates could rise to roughly 1.9% by the end of 2022 and 2.8% by the end of next year.

The Federal Reserve’s main tool for managing the economy is to change the federal-funds rate, which can affect not only borrowing costs for consumers but also shape broader decisions by companies like how many people to hire. WSJ explains how the Fed manipulates this one rate to guide the entire economy. Illustration: Jacob Reynolds

Heading into Wednesday, yields had climbed substantially in recent sessions to their highest levels since 2019 as investors prepare for a new regime of tighter monetary policies.

This year has been a tough one for bond investors. When inflation started to accelerate last year, investors for months thought that it could subside on its own, allowing the Fed to keep short-term interest rates near zero. Those views, though, changed quickly this year due largely to a shift in tone from Fed officials, who began expressing more concern about inflation and an eagerness to start raising rates.

This year’s one significant bond rally came at the end of February when Russia first invaded Ukraine, casting uncertainty over the economic outlook.

SHARE YOUR THOUGHTS

Is the Fed doing enough to address inflation? Join the conversation below.

More recently, though, investors have grown more skeptical that the invasion could keep a lid on interest rates. Some have argued that higher commodity prices spurred by the invasion might only further stoke inflation, putting even more pressure on the Fed to tighten policy. Meanwhile, energy prices have already come down from their recent highs, driven in part by hopes for a negotiated settlement between Russia and Ukraine. That has eased the concerns of those that thought the higher prices could have the opposite effect: slowing economic growth and making it harder for the Fed to raise rates.

The Fed on Wednesday was seen as all but certain to raise its target for overnight interbank borrowing rates by a quarter percentage point to between 0.25% and 0.5%. As a result, investors are primarily focused on the Fed’s so-called dot plot, showing where individual officials expect rates to head over the next few years. They will also gauge the overall tone of Fed Chairman

Jerome Powell’s

news conference, looking to see whether officials are becoming even more worried about inflation.

Regardless of what officials say Wednesday, monetary policies—and therefore bond yields—will still be largely determined by the state of the economy.

Newsletter Sign-up

Real Time Economics

The latest economic news, analysis and data curated weekdays by WSJ’s Jeffrey Sparshott.

On that front, new data showed Wednesday morning that retail sales rose a seasonally adjusted 0.3% in February, below analysts’ forecasts for a 0.4% increase. At the same, sales for January were revised upward to 4.9% from 3.8%.

Treasury yields were little changed after the report. In a note to clients, Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets, wrote that the data showed “a troubling trajectory” but that the upward revisions to January sales did “take the edge off of the disappointing Feb numbers.”