It’s been a difficult year for stocks as the Federal Reserve’s rate-hiking campaign and fears of a recession ahead largely pummel growth-oriented areas of the market. But despite a rough 2022, Jefferies says it’s time for investors to consider putting their money back in some “fallen angels” with solid fundamentals and a decent growth trajectory ahead. “While some of the derating in growth stocks is likely structural, there are also cyclical components such as risks related to slowing economy,” the firm wrote in a note to clients Sunday. “In particular, stocks that have witnessed a significant correction and are now trading at trough valuations compared to their own history while still exhibiting relatively better earnings momentum and quality characteristics compared to their peers, are likely to see the most investor interest.” To find these so-called “fallen angels,” the firm searched for quality names that have undergone a significant correction, trading down more than 25% from their 52-week highs. Despite slumping shares and valuations trading near 10-year lows, these names offer a 10% return on invested capital, and more than 15% return on equity over the next two years. Shares are also trading relatively cheap, at less than 20 times forward price-to-earnings and offer decent earnings momentum ahead. Here are some of the names that made the cut: Several beaten-up technology names came up, including Qualcomm . The semiconductor stock, down more than 40% this year, shared a weak outlook for the current quarter in its earnings results last week and said it’s implemented a hiring freeze. Despite the dropdown in the stock price, shares are expected to bring a 58.2% return on equity and 52.4% return on invested capital and trade cheap at 8.8 times forward earnings, Jefferies found. On the tech front, Jefferies’ screen also included shares of PayPal . Despite slumping 59% this year, the stock offers a 21.9% return on equity. While the payments company recently shared a weaker-than-expected revenue outlook for the fourth quarter , it said last week it plans to add its PayPal and Venmo cards to Apple Wallet. Shares trade at nearly 17 times forward earnings, Jefferies found. A slew of consumer discretionary stocks also made the cut, including Hasbro and Tapestry . Toymaker Hasbro, down about 38% in 2022, recently shared quarterly results that missed earnings expectation s as it grapples with high inventories and rising inflation. Shares trade at about 12 times forward earnings. Home Depot , 3M and Southwestern Energy were also among the names included in Jefferies’ screen. — CNBC’s Michael Bloom contributed reporting

Tag Archives: Jefferies

Wall Street to Pay $1.8 Billion in Fines Over Traders’ Use of Banned Messaging Apps

WASHINGTON—Eleven of the world’s largest banks and brokerages will collectively pay $1.8 billion in fines to resolve regulatory investigations over their employees’ use of messaging applications that broke record-keeping rules, regulators said Tuesday.

The fines, which many of the banks had already disclosed to shareholders, underscore the market regulators’ stern approach to civil enforcement. Fines of $200 million, which many of the banks will pay under the agreements, have typically been seen only in fraud cases or investigations that alleged harm to investors.

But the SEC, in particular, has during the Biden administration pushed for fines that are higher than precedents, saying it wants to levy fines that punish wrongdoing and effectively deter future potential harm. The SEC’s focus on record-keeping is likely to be extended next to money managers, who also have a duty to maintain written communications related to investment advice.

Last month, the SEC alleged that hedge-fund manager Deccan Value Investors LP and its chief investment officer failed to maintain messages sent over

Apple

iMessage and WhatsApp. In some cases, the chief investment officer directed an officer of the company to delete their text messages, the SEC said. The claims were included in a broader enforcement action, which Deccan settled without admitting or denying wrongdoing.

The Wall Street Journal reported last month that the settlements announced Tuesday were likely to top $1 billion and would be announced before the end of September.

Eight of the largest entities, including Goldman Sachs and Morgan Stanley, agreed to pay $125 million to the SEC and at least $75 million to the CFTC. Jefferies will pay a total of $80 million to the two market regulators, and

Nomura

NMR -1.20%

agreed to pay $100 million. Cantor agreed to pay $16 million.

The SEC said it found “pervasive off-channel communications.” In some cases, supervisors at the banks were aware of and even encouraged employees to use unauthorized messaging apps instead of communicating over company email or other approved platforms.

“Today’s actions—both in terms of the firms involved and the size of the penalties ordered—underscore the importance of recordkeeping requirements: they’re sacrosanct. If there are allegations of wrongdoing or misconduct, we must be able to examine a firm’s books and records to determine what happened,” said SEC Enforcement Director

Gurbir Grewal.

Bank of America, which faced the highest fine from the CFTC, had a “widespread and long-standing use of unapproved methods to engage in business-related communications,” according to the CFTC’s settlement order. One trader wrote in a 2020 message to a colleague: “We use WhatsApp all the time, but we delete convos regularly,” according to the CFTC.

One head of a trading desk at Bank of America told subordinates to delete messages from their personal devices and to communicate through the encrypted messaging app Signal, the CFTC said. The head of that trading desk resigned this year, although the bank was aware of his conduct in 2021, the CFTC said.

At Nomura, one trader deleted messages on his personal device in 2019 after being told the CFTC wanted them for an investigation, the agency said. The trader made false statements to the CFTC about his compliance with the records request, the regulator said.

Broker-dealers have to follow strict record-keeping rules intended to ensure regulators can access documents for oversight purposes. The firms settling with the SEC and CFTC admitted their employees’ conduct violated those regulations.

JPMorgan Chase

& Co.’s brokerage arm was the first to settle with the two market regulators over its failure to maintain required electronic records. JPMorgan paid $200 million last year and admitted some employees used WhatsApp and other messaging tools to do business, which also broke the bank’s own policies.

Regulators discovered that some JPMorgan communications, which should have been turned over for separate enforcement investigations, weren’t collected because they were sent on employees’ personal devices or apps that the bank didn’t supervise.

Write to Dave Michaels at dave.michaels@wsj.com

Copyright ©2022 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

Wall Street firm Jefferies returns to remote work and cancels social events after dozens of Covid cases

“Our priority now is to best protect every one of you and your families,” Jefferies (JEF) CEO Rich Handler and president Brian Friedman wrote in a memo to employees Wednesday.

The investment bank said that since the start of December, it has experienced nearly 40 new Covid cases. Tuesday alone saw 10 cases, causing nearly 50 employees to quarantine until they test negative.

Jefferies is based in New York, but it has nearly three dozen offices around the world, including in London and Hong Kong. The company did not specify where the infections occurred. A person familiar with the matter told CNN that the case total refers to a global figure.

Jefferies said that “with only a very few exceptions,” most of the cases have not required hospitalization. The bank pointed out that 95% of all employees are vaccinated and 100% of those who enter its offices are vaccinated.

As a result of the flurry of positive cases, Jefferies said employees will be encouraged to work remotely for the rest of December.

“When you can, we ask that you work from home,” the executives wrote.

Additionally, Jefferies said it will reimpose a mask mandate in all offices and require anyone who wants to enter any office or attend an event to have their booster administered by January 31, unless they are not yet eligible to do so.

“Effective today, we are canceling all social events and entertainment until January 3rd,” the executives said. “We will reassess then, and hopefully all will be better. All parties, big client functions and group events are now on pause. Additionally, all but the most essential business travel should stop, unless it is pre-approved. We are highly disappointed we need to take this step, but it is the prudent path forward to keep everyone as safe as possible.”

Just a day ago, JPMorgan Chase put out an optimistic outlook predicting that 2022 will be a year of a “full global recovery, an end of the global pandemic and a return to normal conditions we had prior to the Covid-19 outbreak.”

But the new health protocols at Jefferies underscore the difficulty businesses face as they try to get employees to work in person at a time of rising Covid cases and concerns about the new Omicron variant. Earlier this week, Ford delayed its return to the office for 30,000 workers because of Covid concerns.

“We strongly believe we are much closer to the end of this mess than the beginning,” the Jefferies executives wrote. “And thanks to all of you, we have achieved incredible success.”

Due to COVID cases, Jefferies cancels travel and parties, resumes remote working

Dec 8 (Reuters) – Investment bank Jefferies Financial Group (JEF.N) on Wednesday cancelled all client parties and most travel, asking employees to work from home when possible due to a spate of COVID-19 cases.

U.S. banks have been more assertive than other industries in encouraging employees back to the office although those plans have come under renewed scrutiny due to the rapid spread of the Omicron variant. Jefferies’ disclosure raised questions about whether other banks will also review return-to-office plans, mask mandates and travel and entertainment policies.

Jefferies, with its headquarters in midtown Manhattan, called its staff back to offices in October. The bank has felt the pandemic’s impact acutely, as its Chief Financial Officer Peg Broadbent died due to coronavirus complications in March 2020.

Register now for FREE unlimited access to reuters.com

Register

“Our priority now is to best protect every one of you and your families,” wrote Chief Executive Richard Handler in a memo seen by Reuters. “Effective today, we are cancelling all social events and entertainment until January 3rd.”

The firm has had more than 40 new COVID-19 cases this month including 10 on Tuesday, the memo said, adding only very few cases required hospitalization. Handler added that Jefferies was re-imposing a mask mandate in all offices, regardless of vaccination status.

The investment bank, which has 3,000 employees worldwide, also has offices in Asia and Europe. More than 95% of Jefferies staff are now vaccinated, and all visitors to Jefferies’ offices must be fully vaccinated, Handler said in the memo.

Most major U.S. banks have had staff working in offices since the summer. Senior bankers such as Goldman Sachs Chief Executive David Solomon and Morgan Stanley Chief Executive James Gorman have spoken of the benefits of in-person interaction, particularly for younger employees.

So far, U.S. banks are sticking to their existing COVID-19 policies although sources at the “big six” firms say they are keeping a close watch on developments. read more

Goldman Sachs (GS.N), Morgan Stanley (MS.N) and JPMorgan (JPM.N) have had most workers back at offices on a rotational basis since the summer.

Others, like Wells Fargo (WFC.N), Citigroup (C.N) and Bank of America (BAC.N), have taken a more flexible stance.

Wells Fargo pushed its return-to-office plans back to January, while Citigroup employees in New York, Chicago, Boston, Philadelphia and Washington, D.C. have been working from the office at least two days a week since Sept. 13.

Most major U.S. banks have also been continuing with holiday parties and client meetings since the Omicron variant was discovered, sources said, although they require proof of vaccination to attend.

Wells Fargo said Wednesday it had no firm-wide celebrations planned. Team parties are at the discretion of individual managers, it added.

In Europe, where Omicron has spread more rapidly, some banks have cancelled events such as JPMorgan’s annual festive carols reception in London and year-end party in Paris.

Deutsche Bank (DBKGn.DE) has told its London staff they can hold small gatherings at the team level. Asset manager Schroders (SDR.L) and the City of London Corporation, which runs London’s historic financial district, ask guests to take rapid tests before some festive events. read more

Some large U.S. companies are also pushing back their office-return date due to the Omicron variant. read more

Jefferies, which the memo said had seen attendance average as high as 60% many days globally in recent weeks, said anyone who wants to enter a Jefferies office or event will have to have a booster vaccination administered by Jan. 31, unless they are not yet eligible to do so.

Register now for FREE unlimited access to reuters.com

Register

Reporting by Matt Scuffham and Aaron Saldanha, additional reporting by Noor Zainab Hussain and Sruthi Shankar in Bangalore; writing by Matt Scuffham and Megan Davies; editing by Edward Tobin and Cynthia Osterman

Our Standards: The Thomson Reuters Trust Principles.

Amid the GameStop-led frenzy, Jefferies says ‘plenty of air’ to come out of riskier assets. Another strategist says wait to buy the dip

Markets are buckled into the fighting chair as another day of the retail-led feeding frenzy on shorted stocks is about to come online.

In case you thought the trading mania was a limited battle between internet day traders and Wall Street hedge funds: videogame retailer GameStop was one of the most traded stocks by value in the U.S. on Wednesday.

Amateur investors, many based on the Reddit group WallStreetBets, are jumping into heavily-shorted stocks, driving prices to astronomical levels and forcing hedge funds to sell bigger, safer bets to cover losses.

Selloff is creeping to other investments and spooking sentiment. Major indexes took a 2% to 3% ride down on Wednesday and are set to continue surfing.

A must-read: Tendies? Diamond hands? Your guide to the lingo on WallStreetBets, the Reddit forum fueling Gamestop’s wild rise

Our call of the day comes from the U.S. equity researchers at Jefferies, led by global equity strategist Sean Darby, with a bonus call from Sébastien Galy, a strategist at Nordea Asset Management.

The team at Jefferies is clear that the correction in share prices has little to do with fundamentals. Rather, what’s happening is a reflection of a “sentiment shift within some of the more overbought and speculative parts of the market.”

The group’s retail speculative index, measuring the deviation from trend of assets where value is hard to determine, is high at 4 standard deviations. “Hence, there is plenty of air to come out of the riskier financial assets,” the team said.

Darby’s team noted that the short-term worry is whether the “popping” of riskier parts of the market will create a domino effect, as mainstream equities are liquidated to stem losses.

Galy, of the Nordic asset manager Nordea, echoes Jefferies’ caution about a wider selloff. He also says it’s too early to buy the dip, because there’s more to come.

The big moves to cover shorts at a time of high leverage typically forces more deleveraging, Galy said. This is because the constraint on capital from the risk of losses on investments is ratcheting up.

“As a consequence, the cost of hedging downside risk has sharply increased,” Galy said. “This risk reduction could last a few days followed by a sharp liquidity driven rebound in U.S. and to a lesser extent European stocks.”

Galy said that even a dovish Federal Reserve meeting on Wednesday couldn’t turn around this market, which is another signal that it may last.

The buzz

Shares in GameStop

GME,

+134.84%

touched the $500 level in the premarket before pulling back. The stock was just $19 heading into 2021. Fashion brand Nakd

NAKD,

+252.31%

is another stock making a big leap in the premarket, up 130%.

In a Securities and Exchange Commission filing this morning, cinema-theater chain AMC

AMC,

+301.21%

revealed that holders of the company’s convertible bonds have chosen to convert the notes into stock, as shares in the company have rallied around 330% since Tuesday.

Apple

AAPL,

-0.77%,

Facebook

FB,

-3.51%,

and Tesla

TSLA,

-2.14%

posted earnings after the close yesterday. Technology giant Apple topped $100 billion in quarterly revenue for the first time, crushing expectations, as social-media company Facebook also beat estimates, with sales soaring 156% from “other revenue” — like virtual-reality headsets and video-chat devices. Electric-car maker Tesla reported its sixth straight quarter of profit, but it was a miss on expectations.

But if you can peel your eyes away from the stock market, it is a big day on the economic front. Initial and continuing jobless claims are due at 8:30 a.m. EST, with around 875,000 people expected to have filed for unemployment last week. Gross domestic product figures for the fourth quarter of 2020 will come at the same time, before new home-sales figures for December are reported at 10 a.m.

After the Federal Open Market Committee decided to hold monetary policy steady yesterday, Fed Chair Jerome Powell gave dovish signals that the central bank wasn’t done restoring the COVID-19 pandemic-ravaged economy to health. “We have not won this yet,” he said.

The markets

It looks like another wild day on Wall Street. Yesterday’s tumult saw the Dow Jones Industrial Average

DJIA,

-2.05%

tumble more than 630 points, and stock market futures

YM00,

-0.07%

ES00,

-0.31%

NQ00,

-0.90%

are pointing down, set to continue the selloff. Asian markets

NIK,

-1.53%

HSI,

-2.55%

HSI,

-2.55%

fell across the board and European indexes

SXXP,

-0.76%

UKX,

-1.13%

DAX,

-0.86%

PX1,

-0.17%

are firmly in the red.

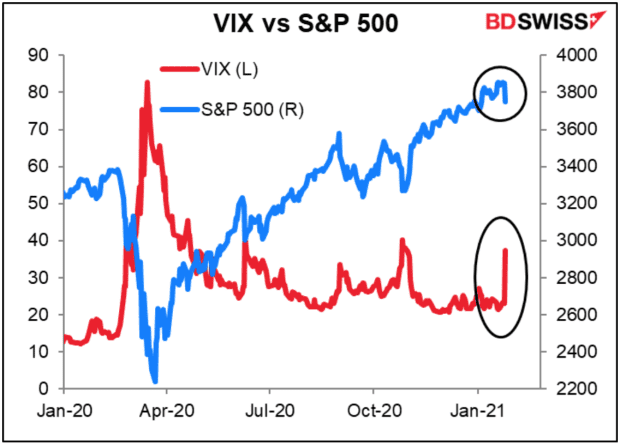

The chart

Our chart of the day, from Marshall Gittler at BDSwiss, shows how the S&P 500

SPX,

-2.57%

dropped by the most since October 2020, and the VIX index of expected volatility saw its biggest one-day rise since the COVID-19 pandemic hit in March 2020.

The tweet

When the sharks root for the fish. Billionaire entrepreneur and investor Mark Cuban — of “Shark Tank” fame — is rooting for Reddit’s WallStreetBets traders.

Random reads

An Oklahoma lawmaker has proposed a ‘Bigfoot’ hunting season with a new bill.

Key West wants to ban people from feeding fat, feral, free-roaming chickens.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Want more for the day ahead? Sign up for The Barron’s Daily, a morning briefing for investors, including exclusive commentary from Barron’s and MarketWatch writers.