- John Cleese Defends Monty Python Manager After Eric Idle Called Group’s Income Disastrous: ‘We Always Loathed and Despised Each Other’ Variety

- Monty Python’s Eric Idle says he’s still working at 80 for financial reasons: “Not easy at this age” CBS News

- Is Eric Idle Broke? 5 Revelations Made by the Monty Python Co-Founder on X Hollywood Reporter

- Eric Idle Takes Shots at Monty Python Co-Stars as He Reveals Financial Woes The Daily Beast

- John Cleese Responds To Eric Idle Slam: “We Always Loathed And Despised Each Other” Deadline

Tag Archives: income

State-level macro-economic factors moderate the association of low income with brain structure and mental health in U.S. children – Nature.com

- State-level macro-economic factors moderate the association of low income with brain structure and mental health in U.S. children Nature.com

- Anti-poverty programs may help reduce disparities in brain development and mental health symptoms in children National Institutes of Health (.gov)

- Larger welfare checks lead to healthier brains, study finds The Hill

- Poverty hurts young brains but social safety net may help Harvard Gazette

- Anti-poverty programs may help reduce disparities in brain development and mental health symptoms in children | National Institute on Drug Abuse National Institute on Drug Abuse

- View Full Coverage on Google News

Russell Wilson’s Why Not You charity is using less than quarter of its income to help kids – CBS Sports

- Russell Wilson’s Why Not You charity is using less than quarter of its income to help kids CBS Sports

- Russell Wilson’s foundation responds to investigation into financial practices KING 5 Seattle

- Russell Wilson and Ciara’s children’s charity gives almost no money to kids SB Nation

- Russell Wilson’s foundation responds to report scrutinizing charitable practices The Seattle Times

- Russell Wilson’s Why Not You Foundation reportedly spent more on employee salaries than charitable activities Yahoo Sports

- View Full Coverage on Google News

New MIT Research Indicates That Automation Is Responsible for Income Inequality

A newly published paper quantifies the extent to which automation has contributed to income inequality in the U.S., simply by replacing workers with technology — whether self-checkout machines, call-center systems, assembly-line technology, or other devices.

Recent data suggests that the majority of the increase in the wage gap since 1980 can be attributed to automation replacing less-educated workers.

When using self-checkout machines in supermarkets and drugstores, it is unlikely that you are bagging your purchases as efficiently as checkout clerks used to. The main advantage of automation for large retail chains is that it reduces the cost of bagging.

“If you introduce self-checkout kiosks, it’s not going to change productivity all that much,” says MIT economist Daron Acemoglu. However, in terms of lost wages for employees, he adds, “It’s going to have fairly large distributional effects, especially for low-skill service workers. It’s a labor-shifting device, rather than a productivity-increasing device.”

A newly published study co-authored by Acemoglu quantifies the extent to which automation has contributed to income inequality in the U.S., simply by replacing workers with technology — whether self-checkout machines, call-center systems, assembly-line technology, or other devices. Over the last four decades, the income gap between more- and less-educated workers has grown significantly; the study finds that automation accounts for more than half of that increase.

“This single one variable … explains 50 to 70 percent of the changes or variation between group inequality from 1980 to about 2016,” Acemoglu says.

The paper was recently published in the journal Econometrica. The authors are Acemoglu, who is an Institute Professor at

At the same time, the scholars used U.S. Census Bureau metrics, including its American Community Survey data, to track worker outcomes during this time for roughly 500 demographic subgroups, broken out by gender, education, age, race and ethnicity, and immigration status, while looking at employment, inflation-adjusted hourly wages, and more, from 1980 to 2016. By examining the links between changes in business practices alongside changes in labor market outcomes, the study can estimate what impact automation has had on workers.

Ultimately, Acemoglu and Restrepo conclude that the effects have been profound. Since 1980, for instance, they estimate that automation has reduced the wages of men without a high school degree by 8.8 percent and women without a high school degree by 2.3 percent, adjusted for inflation.

A central conceptual point, Acemoglu says, is that automation should be regarded differently from other forms of innovation, with its own distinct effects in workplaces, and not just lumped in as part of a broader trend toward the implementation of technology in everyday life generally.

Consider again those self-checkout kiosks. Acemoglu calls these types of tools “so-so technology,” or “so-so automation,” because of the tradeoffs they contain: Such innovations are good for the corporate bottom line, bad for service-industry employees, and not hugely important in terms of overall productivity gains, the real marker of an innovation that may improve our overall quality of life.

“Technological change that creates or increases industry productivity, or productivity of one type of labor, creates [those] large productivity gains but does not have huge distributional effects,” Acemoglu says. “In contrast, automation creates very large distributional effects and may not have big productivity effects.”

A new perspective on the big picture

The results occupy a distinctive place in the literature on automation and jobs. Some popular accounts of technology have forecast a near-total wipeout of jobs in the future. Alternately, many scholars have developed a more nuanced picture, in which technology disproportionately benefits highly educated workers but also produces significant complementarities between high-tech tools and labor.

The current study differs at least by degree with this latter picture, presenting a more stark outlook in which automation reduces earnings power for workers and potentially reduces the extent to which policy solutions — more bargaining power for workers, less market concentration — could mitigate the detrimental effects of automation upon wages.

“These are controversial findings in the sense that they imply a much bigger effect for automation than anyone else has thought, and they also imply less explanatory power for other [factors],” Acemoglu says.

Still, he adds, in the effort to identify drivers of income inequality, the study “does not obviate other nontechnological theories completely. Moreover, the pace of automation is often influenced by various institutional factors, including labor’s bargaining power.”

Labor economists say the study is an important addition to the literature on automation, work, and inequality, and should be reckoned with in future discussions of these issues.

For their part, in the paper Acemoglu and Restrepo identify multiple directions for future research. That includes investigating the reaction over time by both business and labor to the increase in automation; the quantitative effects of technologies that do create jobs; and the industry competition between firms that quickly adopted automation and those that did not.

Reference: “Tasks, Automation, and the Rise in U.S. Wage Inequality” by Daron Acemoglu and Pascual Restrepo, 14 October 2022, Econometrica.

DOI: 10.3982/ECTA19815

The study was funded by Google, the Hewlett Foundation, Microsoft, the National Science Foundation, Schmidt Sciences, the Sloan Foundation, and the Smith Richardson Foundation.

A 39-year-old who makes $160,000/month in passive income shares his best advice

When starting a business, it’s sometimes hard to know what to prioritize, and going at it alone can be overwhelming. But there are strategies you can use to avoid common pitfalls.

My mission is to teach people how to earn money from their passions. It’s what I did: I went from living on food stamps to building two online businesses.

Today, I run a music blog, The Recording Revolution, and a entrepreneurship coaching company. I work just five hours a week from my home office and make $160,000 a month in passive income.

Here’s what I tell my 3,000 clients to think about in the first 30 days of starting a business:

1. Be clear about how you want to spend your time.

Many new business owners I meet know only one thing: how much money they want to make.

While that’s a great starting point, it’s incomplete. Your business should serve your life, not the other way around. So make sure it aligns with your hopes, dreams and goals.

To get clear about the type of business and life you want, ask three questions:

- What does a perfect day look like to you? Don’t just think about your typical workday. Consider other life activities you want to fit into your day, like exercising or spending time with family.

- How many hours do you want to work a week? You don’t have to follow the standard 40-hour workweek. Knowing exactly how many hours you want to work will help you better prioritize tasks.

- How important is time off? Some people don’t care much about taking time off, as long as they love what they do. Others value extended time off. In order to have money flowing in when you’re not working, you’ll need to have some sort of passive income stream.

2. Simplify your business model.

When I started my music education business, people told me I needed to test my sales pages, throw launch parties and pre-record a bunch of ads in order to grow.

Rather than stretching myself thin doing things that didn’t make sense to me, I kept it simple and focused on three things: creating weekly content for my blog and YouTube channel, growing my email list from that audience, and promoting the paid products I created to that list.

If you’re just starting out, develop content around your expertise to grow an audience. It doesn’t have to be perfect. You can iterate as you go and design new products based on what your customers want more of.

3. Cut out unnecessary daily tasks.

Identify what daily activities will help you earn more. Don’t waste time or burn yourself out focusing on unimportant tasks.

It might feel good to get to inbox zero or change the color of the buttons on your website, especially in the early days where you want to feel like you’ve achieved a goal. But neither of those things will make you money.

Before you start a new task, ask yourself three questions:

- What’s the expected outcome for doing this task?

- Does it lead to more money?

- Can I point to a direct link between doing that task and earning income?

- What’s the cost of doing this instead of something else?

4. Prioritize having fun.

People can tell if you’re just doing something for the money or if you actually love what you do. That authenticity will connect you deeper to your customers and it will sustain you for the long haul.

You don’t want to burn out because you spent all your time doing things that weren’t meaningful to you.

I always give my students this framework when they are beginning their entrepreneur journey: Build a business around something you see yourself doing and enjoying for the next 10 years.

Graham Cochrane is founder of The Recording Revolution and author of “How to Get Paid for What You Know.” He has helped more than 3,000 people launch and improve their own businesses. Follow him on Instagram and Twitter.

Don’t miss:

Trump paid no federal income tax in his last year as president

New York

CNN

—

Former President Donald Trump reported a stunning reversal of fortune during the middle two years of his presidency that led to a considerable tax bill, according to a report from the Joint Committee on Taxation released Tuesday night.

The $1.1 million Trump paid in federal taxes in 2018 and 2019 stand in stark contrast to the $750 he paid in 2017 and $0 in 2020.

Trump’s tax bill grew substantially as his income surged in 2018 and 2019, according the report that included details on Trump’s tax returns from 2015 to 2020, ahead of the planned release of the returns themselves. For example, Trump reported a $22 million capital gain in 2018 and a $9 million gain in 2019 from asset sales, sending his income into the black following years of enormous losses.

In 2015 and 2016, Trump reported he lost more than $32 million each year. In 2017, Trump said he lost nearly $13 million. But he reported taxable income of $24 million in 2018 and more than $4 million in 2019, giving him a sizeable tax bill.

Trump has leveraged massive losses he accumulated over the years to zero out his tax liabilities, as previously shown by a New York Times investigation. For example, the JCT noted that Trump carried forward $105 million in losses on his 2015 return, $73 million in 2016, $45 million in 2017 and $23 million in 2018.

“It’s the 2,000-pound gorilla. … He still uses the net operating losses” to reduce his tax liability, said Steven M. Rosenthal, senior fellow in the Urban-Brookings Tax Policy Center at the Urban Institute.

And once again, in 2020, as the pandemic raged on, Trump reported a loss of nearly $5 million. He paid $0 in federal income taxes that year.

D.C. attorney general sues billionaire Michael Saylor for alleged income tax evasion

The lawsuit, which Racine filed Aug. 22 in D.C. Superior Court, alleges that Saylor has for years fraudulently claimed to be a resident of lower-tax jurisdictions despite living in a 7,000-square-foot penthouse on the Georgetown waterfront. The complaint further alleges that MicroStrategy, despite knowing Saylor was a D.C. resident, conspired in the scheme “instead of accurately reporting his address to local and federal tax authorities and correctly withholding District taxes.” Both Saylor and MicroStrategy issued statements on Wednesday, denying the allegations in the suit.

The complaint alleges that Saylor purchased the Georgetown property in 2005 before buying two adjoining penthouse units, combining them into a single residence Saylor calls “Trigate,” and also purchased a penthouse unit in Adams Morgan. Beginning in 2012, according to the complaint, Saylor purchased a home in Miami Beach, obtained a Florida driver’s license and registered to vote there despite living primarily in D.C. The suit alleges he did not pay income taxes in D.C. at any point between 2005 and 2021, despite social media posts over the years that indicate he lived in D.C. and considered it home.

“Since at least 2012, Saylor has bragged to his confidants about his successful plan to create the illusion of residing in Florida in order to evade the District’s personal income taxes,” the complaint reads. The lawsuit alleges that MicroStrategy abetted in the fraud through an agreement to list Saylor’s residence on federal tax forms as his house in Florida, despite knowing he lived in D.C., “actively assisting Saylor to avoid his obligation to pay taxes owed to the District.” (Florida has no state individual income tax).

Saylor said in his statement that he bought the Miami Beach home a decade ago after moving from Virginia.

“Although MicroStrategy is based in Virginia, Florida is where I live, vote, and have reported for jury duty, and it is at the center of my personal and family life,” he wrote. “I respectfully disagree with the position of the District of Columbia, and look forward to a fair resolution in the courts.”

Saylor founded MicroStrategy in 1998 and served as its CEO until earlier this month when the publicly traded company announced that he would take on a new role as its executive chairman. In an Aug. 2 news release announcing the leadership change, MicroStrategy said that Saylor would also remain chairman of its board of directors.

MicroStrategy in its own statement denied the allegations and vowed to “defend aggressively against this overreach.”

“The case is a personal tax matter involving Mr. Saylor,” the statement said. “The Company was not responsible for his day-to-day affairs and did not oversee his individual tax responsibilities. Nor did the Company conspire with Mr. Saylor in the discharge of his personal tax responsibilities.”

Racine’s office said the lawsuit was brought under the city’s recently expanded False Claims Act, which the D.C. Council last year amended to include tax-related issues, and incentivizes whistleblowers to identify tax fraud. Racine said the law also enables the court to levy a punishment up to three times the amount of taxes evaded, and that between the unpaid income taxes and other penalties his office is seeking to recover from Saylor and MicroStrategy, damages in the case could amount to more than $100 million.

The lawsuit builds on a similar complaint filed against Saylor by whistleblowers in D.C. Superior Court last year, which was unsealed Wednesday. Racine’s office said it independently investigated the tax fraud allegations and intervened in the whistleblower complaint, filing its own lawsuit against Saylor and MicroStrategy.

Joe Biden, Harris donated less than others in income bracket

When it comes to charity, President Biden and Vice President Harris came up short compared to their fellow Americans, a review of their tax returns shows.

The president and First Lady Jill Biden reported $610,702 in income for 2021 and paid $183,925 in federal and state income taxes. The couple gave $17,394 to charity, or about 2.8%. That’s roughly 0.3 % less than the average charitable deduction for Americans making between $500,000 and $2 million, according to 2016 data from the nonpartisan Tax Policy Center.

In Harris’ case, the disparity was worse. The vice president and her husband, Second Gentleman Doug Emhoff, earned $1,655,563 in 2021 and paid $523,371 in federal income taxes. The couple donated $22,100 — or 1.3% — to charity. The figure is considerably less than the 3.1% on average donated by those making between $500,000 and $2 million.

The giving disparity between the Biden and Harris families was first reported by Fox News. The Tax Policy Center data showed the poorest Americans were by far the most generous, with those making less than $50,000 who itemized charitable deductions donating 8.4%.

Biden’s largest charitable donation of 2021 was a $5,000 gift to the Beau Biden Foundation, named in honor of his son who died of cancer in 2015. The Bidens were considerably more generous in 2020, donating $30,704 of their income to charity, or about 5%.

The Beau Biden Foundation is officially dedicated to protecting children from abuse, but unofficially has long served as a clearinghouse for Biden cronies to collect fat paychecks.

The organization’s executive director Patricia Dailey Lewis, served as Delaware deputy attorney general while when Beau Biden served as AG. She pocketed $150,660 in 2020, including a $3,500 bonus, records show. Joshua Alcorn, another longtime Biden political consultant, made $131,437 as COO, though he has since stepped down. Board members have included President Biden’s troubled son Hunter as well as Beau’s widow Hallie Biden.

The charity only spent 58% of its raised funds on its stated mission — well below top rated philanthropic organizations, industry experts said.

“A 58 percent program ratio does not reflect a high level of financial efficiency,” said Laurie Styron, the executive director of CharityWatch told The Post.

Can the US Government Afford Higher Interest Rates? You Bet. $67 Trillion “Fixed Income” Assets Will Generate Higher Incomes & Tax Revenues, Boost Secondary Effects

Bring them on. Financial Repression has a huge cost.

By Wolf Richter for WOLF STREET.

Yields have been rising in anticipation of a tightening cycle, and they will rise further when the Fed actually raises rates and engages in quantitative tightening (QT). Rising yields reduce bond prices for investors who sell those bonds. Investors that hold bonds to maturity earn the yield at which they purchased the security, and at maturity they get paid face value. A few hedge funds might blow up along the way because their highly leveraged bets went awry. So for current bondholders, a tightening cycle is not pretty.

But for future bond buyers and for savers, a whole new world opens up: a world with more income. And this higher income will throw off more tax revenues for governments. So how much money are we talking about here? $67 trillion in assets that will generate higher incomes.

There has been a lot of talk how the Fed can never raise interest rates because of x,y, and z, and how the Fed can never do QT because of x,y, and z. And one of the reasons often cited is that the US government wouldn’t be able to afford the higher interest payments. But that’s a red herring.

First, the US government issues its own currency and can always pay for anything with the Fed’s newly created money. The Federal Reserve Board of Governors, of which Powell is Chair Pro Tempore, is an agency of the US government. So the US won’t ever run out of money, but the dollar might run out of purchasing power – the trade-off that is now particularly ugly.

Second, only newly-issued Treasury securities would carry the higher coupon interest rate, and the still outstanding Treasury securities would continue to pay the same coupon interest as before. The higher rates would only show up when securities mature and are replaced by new securities, and as deficit spending is funded with new securities. So higher interest rates would only gradually filter into actual interest expenses for the government.

Third, and this is the topic here because no one ever mentions it: higher interest rates generate higher income across the entire Fixed Income spectrum, and higher income generates higher tax revenues.

Total “Fixed Income” Spectrum: $67 trillion.

There were nearly $54 trillion in US-issued bonds that were publicly traded at the end of 2021. This does not include bank loans, and it does not include the Treasury securities that are held by US government pension funds and by the Social Security Trust Fund (source of data: Sifma, US Treasury Dept.).

| US issued publicly traded bonds | Trillion $ |

| Treasury Securities, portion held by the public | 23.1 |

| Mortgage-backed securities | 12.0 |

| Corporate bonds | 10.0 |

| Municipal securities | 4.0 |

| Federal Agency securities | 2.0 |

| Asset-backed securities | 1.5 |

| Money Market | 1.1 |

| Total publicly traded bonds | 53.7 |

And deposits… There are about $18 trillion in deposits at commercial banks and credit unions. About $5 trillion are demand deposits, such as checking accounts. But around $13 trillion are deposits that in normal times carry interest, such as savings accounts and CDs.

Combined, the $53.7 trillion in publicly traded bonds and the $13 trillion in savings products make up the spectrum of “Fixed Income.” But that “fixed income” – the cash flow from regular interest payments – has gotten brutally crushed and sacrificed by the Fed on the altar of asset price inflation, as that whole range of investors, from life insurers to retirees and savers can attest to.

So about $67 trillion total investments would gradually begin to generate higher interest income as interest rates rise. And that income would generate income taxes for the federal government.

In other words, if some day in the future, the Federal government had to pay an interest rate that is 3 percentage points higher on average on its public debt, the entire and much larger fixed income spectrum would pay out about 3 percentage points higher interest rates, and recipients pay taxes on this additional income.

In addition, there are the secondary effects: Fixed income investors have gotten crushed when the cash flows from their investments went to near-zero. Many of them cut back their spending in response. Higher interest incomes across the Fixed Income spectrum would fuel more spending by the recipients – many of whom, such as retirees, would spend every dime they get – and this economic activity would generate more income, and more tax revenues.

Crushing the huge Fixed Income spectrum through the Fed’s financial repression was a really, really bad idea for numerous reasons – including the consequences on real economic activity. This started during the Financial Crisis with QE, and except for a feeble respite in 2018 and 2019, continues through today.

Obviously, when interest rates rise beyond a certain level, they begin to impact the economy in the other direction more strongly than higher interest income boosts spending and supports the economy – and the cooling-down process that the Fed is now planning begins.

When we look at the interest expense of the government, we should look at tax revenues triggered by the whole Fixed Income spectrum. That’s not how budget analysis works, but that’s how reality works. In other words: bring on those higher interest rates!

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

WHOOSH Goes the Fed’s Lowest Lowball Inflation Measure. And Eats Up All Income Gains Plus Some

Powell should pay attention here so he’s better prepared at the next press conference when asked about the impact of inflation on regular Americans.

By Wolf Richter for WOLF STREET.

Fed chair Jerome Powell’s reaction today after he saw the consequences of his reckless monetary policies. Imagined by cartoonist Marco Ricolli for WOLF STREET.

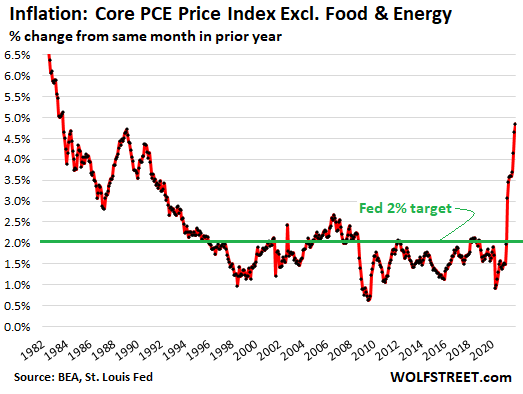

The “core PCE” price index, which excludes food and energy and which understates inflation by the most of all of the government’s inflation measures and which is therefore wisely used by the Fed for its inflation target, spiked by 0.50% in December from November, and by 4.9% year-over-year, the worst inflation reading since 1983, according to the Bureau of Economic Analysis today. As measured by this lowest lowball inflation measure, inflation, is well over double the Fed’s inflation target:

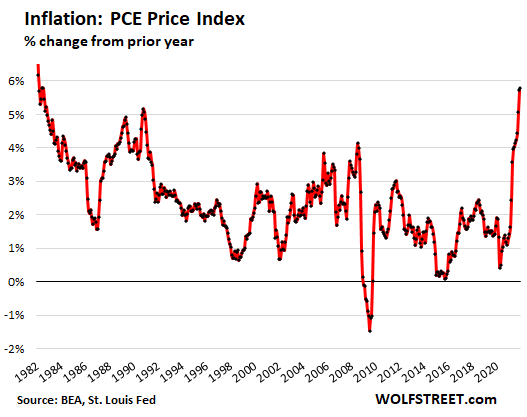

The overall PCE inflation index, which includes food and energy, spiked by 0.45% in December from November, and by 5.8% year-over-year, the worst reading since 1982.

So how did this inflation – the worst in 40 years – impact wages and salaries? Powell should pay attention here so that he is better prepared for the next post-meeting press conference when some wayward reporter asks him about the impact of inflation on regular Americans.

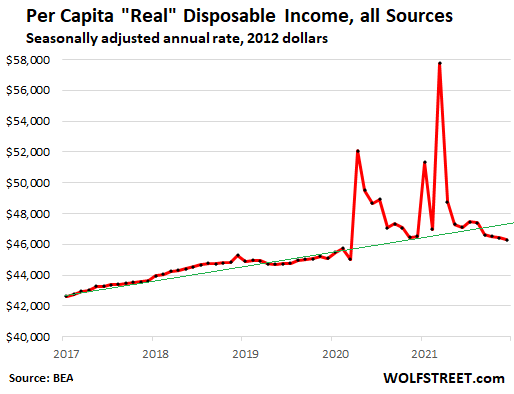

Adjusted for inflation, per-capita disposable income (income from all sources minus income-related taxes, on a per person basis) fell by 0.3% for the month and fell by 0.5% year-over-year, continuing the relentless decline that started last summer when inflation took off at a velocity not seen in decades. Note the pre-pandemic, pre-massive-inflation trend line (green):

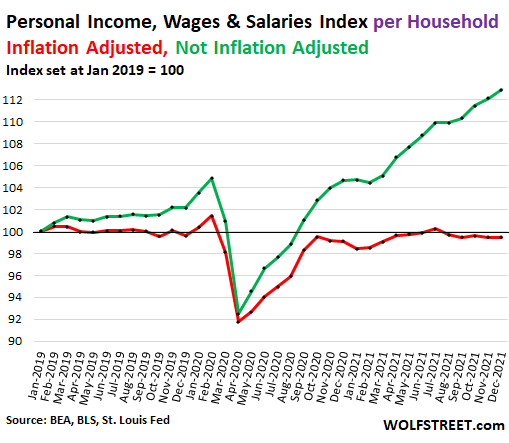

Compensation from wages and salaries, not adjusted for inflation, and not including government transfer payments, rose by 0.7% in December, by 9.2% year-over-year. And those kinds of wage and salary gains would be something to celebrate. But they were eaten up entirely by inflation. On a per-household basis, after inflation, those wage and salary gains disappeared entirely, opening up an ever-wider gap between the money people earn with their labor, and what’s left over after inflation.

As inflation whittled down the purchasing power of labor, the rising number of households reduced the slice each household gets of the aggregate inflation-diminished income figures to where inflation-adjusted income from wages and salaries is now below where it was two years ago and below where it was three years ago:

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()