- Paramount Global Sees Tough Q2 In Film (‘Transformers’ Vs ‘Top Gun’), Muted DTC Growth But Otherwise Bests Forecasts; Streaming Losses Narrow, Stock Pops Deadline

- Paramount stock jumps amid improved Q2 streaming losses Yahoo Finance

- Paramount’s Streaming Losses Narrow to $424M as Subscribers Inch to 61M Hollywood Reporter

- Paramount Global Narrows Streaming Q2 Loss But Grapples With TV Ad Declines Variety

- Paramount CEO Bob Bakish Says “We Remain Hopeful For A Timely Resolution” To Writers & Actors Strikes Deadline

- View Full Coverage on Google News

Tag Archives: forecasts

World premiere for the efficiency champion: Volkswagen ID.7 (ID.7 – Near-production concept car. The vehicle has not gone on sale yet.) with a range of up to 700 km (Depending on the battery size, forecasts indicate that WLTP ranges of up to 700 kilometres – Volkswagen Newsroom

- World premiere for the efficiency champion: Volkswagen ID.7 (ID.7 – Near-production concept car. The vehicle has not gone on sale yet.) with a range of up to 700 km (Depending on the battery size, forecasts indicate that WLTP ranges of up to 700 kilometres Volkswagen Newsroom

- VW ID.7 World Premiere Volkswagen News

- VW aims to dethrone the Tesla Model 3 with its long-ranging ID.7 electric sedan The Verge

- Why you should check out the new 435-mile range Volkswagen ID.7 electric sedan Electrek.co

- 2025 Volkswagen ID.7 Promises More Power, Better Range Than ID.4 Car and Driver

- View Full Coverage on Google News

‘Surprisingly resilient’: IMF lifts global growth forecasts | International Monetary Fund

The International Monetary Fund (IMF) has raised its 2023 global growth outlook slightly due to “surprisingly resilient” demand in the United States and Europe and the reopening of China’s economy after Beijing abandoned its strict zero-COVID strategy.

The IMF said global growth would still fall to 2.9 percent in 2023 from 3.4 percent in 2022, but its latest World Economic Outlook forecasts mark an improvement over an October prediction of 2.7 percent growth this year, with warnings that the world could easily tip into recession.

For 2024, the IMF said global growth would accelerate slightly to 3.1 percent, but interest rate hikes by central banks around the world would slow demand.

IMF chief economist Pierre-Olivier Gourinchas said recession risks had subsided and central banks were making progress in controlling inflation, but more work was needed to curb prices, and new disruptions could come from further escalation of the war in Ukraine and China’s battle against COVID-19.

“We have to sort of be prepared to expect the unexpected, but it could well represent a turning point, with growth bottoming out and then inflation declining,” Gourinchas told reporters of the 2023 outlook.

Strong demand

In its 2023 gross domestic product (GDP) forecasts, the IMF said it now expected GDP growth in the US of 1.4 percent, up from the 1.0 percent predicted in October and following 2.0 percent growth in 2022.

The fund cited stronger-than-expected consumption and investment in the third quarter of 2022, a robust labour market and strong consumer balance sheets.

It said the eurozone had made similar gains, with 2023 growth for the bloc now forecast at 0.7 percent, compared with 0.5 percent in the October outlook, following 3.5 percent growth in 2022. The IMF said Europe had adapted to higher energy costs more quickly than expected, and an easing of energy prices had helped the region.

The United Kingdom was the only major advanced economy the IMF predicted to be in recession this year.

It forecast the British economy to shrink 0.6 percent this year, compared with a previous expectation for growth of 0.3 percent. People are struggling with higher interest rates, and government moves to further tighten spending are also squeezing growth, it said.

“These figures confirm we are not immune to the pressures hitting nearly all advanced economies,’’ Chancellor of the Exchequer Jeremy Hunt said in response to the IMF forecast. “Short-term challenges should not obscure our long-term prospects — the UK outperformed many forecasts last year, and if we stick to our plan to halve inflation, the UK is still predicted to grow faster than Germany and Japan over the coming years.”

China reopens

The IMF revised China’s growth outlook sharply higher for 2023, to 5.2 percent from 4.4 percent in the October forecast after its ‘zero-COVID’ strategy held back the economy. China’s growth rate was 3.0 percent in 2022, below the global average for the first time in more than 40 years.

Still, the fund added that China’s growth will “fall to 4.5 percent in 2024 before settling at below 4 percent over the medium term amid declining business dynamism and slow progress on structural reforms”.

At the same time, it maintained India’s outlook for a dip in 2023 growth to 6.1 percent but a rebound to 6.8 percent in 2024, matching its 2022 performance.

Gourinchas said together, the two Asian powerhouse economies will contribute more than 50 percent of global growth in 2023.

He acknowledged that China’s reopening would put some upward pressure on commodity prices, but “on balance, I think we view the reopening of China as a benefit to the global economy” as it will help ease production bottlenecks that have worsened inflation and by creating more demand from Chinese households.

Even with China’s reopening, the IMF is predicting that oil prices will fall in both 2023 and 2024 due to lower global growth compared with 2022.

Risks

The IMF said there were both upside and downside risks to the outlook, with built-up savings creating the possibility of sustained demand growth, particularly for tourism, and an easing of labour market pressures in some advanced economies helping to cool inflation, lessening the need for aggressive rate hikes.

But it detailed more and larger downside risks, including more widespread COVID-19 outbreaks in China and a worsening of the country’s property turmoil.

An escalation of the war in Ukraine could lead to a further spike in energy and food prices, as would a cold northern winter next year as Europe struggles to refill gas storage and competes with China for liquefied natural gas supplies, the fund said.

Gourinchas said central banks need to stay vigilant and be more certain that inflation is on a downward path, particularly in countries where real interest rates remain low, such as in Europe.

“So we’re just saying, look, bring monetary policy slightly above neutral at the very least and hold it there. And then assess what’s going on with price dynamics and how the economy is responding, and there will be plenty of time to adjust course, so that we avoid having overtightening,” Gourinchas said.

2023 Housing Price Forecasts: More Bears Than Bulls

2023 housing price forecasts from various institutions range from -22% to + 5.4%. There is no consensus as to which way house prices will go. However, the bias is towards the downside.

There is also the issue of forecasting the national median home price and the price of your local housing market. While we care about the national median home price forecast, we care way more about our local housing market forecast.

For background, I expected the median sales price in the United States to rise by 8% to 10% in 2022. My estimate was less bullish than the majority of firms expecting 12% – 18% price increases.

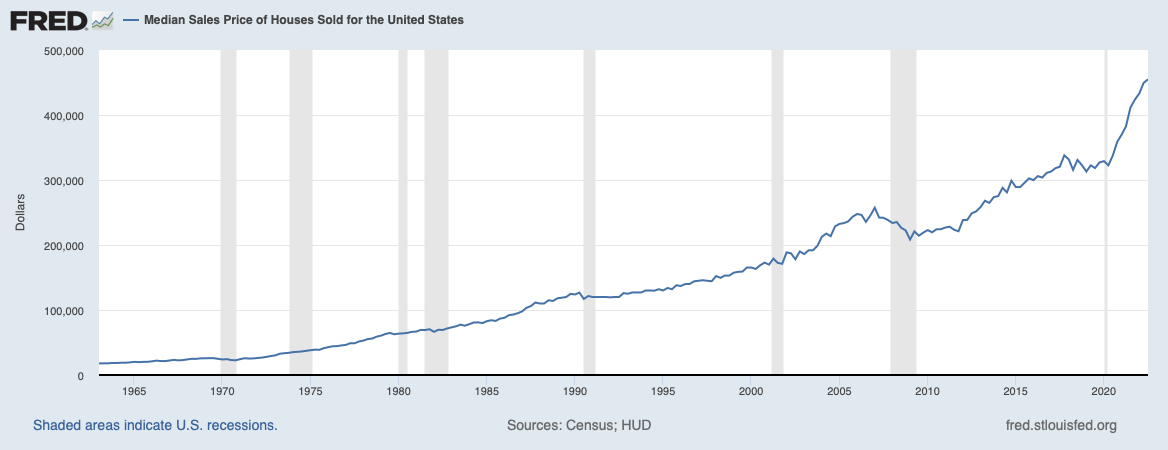

The 4Q2021 median home price was $423,600. The latest pricing data available, 3Q 2022, shows the median home price of $454,900, or a 7.4% increase. 4Q 2022 housing price data will be released in 1Q 2023.

2023 Housing Price Forecasts

Take a look at the housing price forecasts for 2023 from some popular real estate or real estate-related institutions. They are all over the place!

All housing price forecasts are subject to change over time as datapoints and conditions change. I will update the changes as they happen.

The Most Bearish Housing Forecasts For 2023

John Burns Real Estate Consulting (JBREC): -20% to -22%

Zonda: -10%

Goldman Sachs: -5% to -10%

Redfin: -4%

The Most Bullish Housing Price Forecasts For 2023

Realtor.com: +5.4%

CoreLogic: +4.1%

National Association Of Realtors: +1.2%

The Most Boring Housing Price Forecasts For 2023

Fannie Mae: -1.5%

Freddie Mac: -0.2%

MBA: +0.7%

Zillow: +0.8%

My Thoughts On The Extreme Housing Price Forecasts

When it comes to forecasting, it’s good to first look at the tail ends. It helps to see who is delusional and whether you have any blind spots.

Most Bearish Call

I like the work of John Burns Real Estate Consulting (JBREC). However, they are too pessimistic forecasting a -20% to -22% decline in housing prices in 2023. A 20% median home price decline would bring the national median home price down to about $364,000.

A 20% – 22% price decline would mean a GREATER decline than the one during the global financial crisis. Median home prices declined from $257,000 in 1Q 2007 to $208,400 in 1Q 2009, or -18.9%. Further, it took two years for national median home prices to decline by 18.9%.

It is improbable the national median home price will decline by more than it did during the global financial crisis in half the amount of time. Credit standards are much higher than they were before the 2008 crisis. Meanwhile, the vast majority of homeowners locked in mortgage rates below 5%.

If we say this housing downturn is 30% as bad as the one from 2007 – 2009, then we’d get to a -5.7% housing price decline.

Most Bullish Call

On the flip side, there’s the +5.4% housing price forecast by Realtor dot com. Realtor dot com is a website that helps you find a realtor to buy or sell a home. The realtor pays a referral fee on closed transactions. The stronger the housing market, the more business Realtor dot com will generate.

It’s not a coincidence CoreLogic (+4.1%),the National Association Of Realtors (+1.2%), Mortgage Bankers Association (+0.7%), and Zillow (+0.8%) are all also looking for higher median house prices in 2023. I fear they suffer from business sector bias.

With a Fed-induced recession likely in 2023 and higher average mortgage rates, I think every forecast that shows an increase in 2023 housing prices is wrong. Housing prices lag, not lead.

My 2023 Housing Price Forecast

With an 75% conviction level, I expect the median housing price for 2023 to decline by 8% to $419,000. I’m assuming the median house price ends 2022 at $455,000 based on the St. Louis Fed data.

The reasons include:

- A global recession by the end of 2023

- The Fed insisting on hiking to a 5% – 5.125% terminal rate even though inflation is clearly declining and annualizing under 2%

- A higher risk-free rate makes investing in risk assets less appealing

An 8% decline in housing prices is disappointing for real estate owners. However, real estate has outperformed the S&P 500 by over 25% in 2022. Giving back 8% is not that bad, especially if you bought responsibility or have little-to-no mortgage left.

The reasons why I don’t expect home prices to decline by more than 8% are:

- 30-year fixed mortgage rates should decline by 2% – 3% from their peak of 7% by mid-2023. 4% – 5% 30-year fixed mortgage rates should bring back demand.

- The Treasury bond market has stopped listening to the Fed. The 10-year bond yield did not move after the Fed raised rates another 50 bps on December 14, 2022. The huge yield inversion between the 10-year and the 3-month Treasury bond is saying the Fed is making a mistake. And retail mortgage rates are priced largely off the 10-year bond yield.

- Consumers still have “excess” savings thanks to tremendous stimulus spending in 2020 and 2021.

- There will continue to be an undersupply of homes. The vast majority of homeowners have 30-year fixed mortgage rates under 5%. Therefore, there’s no need for most to sell.

- The will be a continued capital shift towards real assets and away from funny money assets like stocks, cryptocurrencies, and anything else that provides zero utility.

- The average credit score for borrowers of new mortgages is over 720.

- There is a huge amount of home equity built over the years. Home prices would need to fall by over 40% to have the same proportion of homes under water starting in 2008.

Downside Risks To My Negative Housing Price Forecast: Desperation

One of the biggest unknowns is how much new housing supply will come to market during the traditionally strong spring season. If there are too many desperate sellers, we could see home prices fall by more than 8%.

You also have funky scenarios where a house is priced too high and becomes “stale fish.” You might also encounter extremely motivated sellers going through a divorce. One short-sale can ruin the values of a dozen neighboring homes.

The other main downside risk to my negative housing price forecast is a more aggressive Fed. Although the Treasury bond market has stopped believing the Fed, a 5.125% Fed Funds rate will squeeze consumer debt borrowers. Everything from credit card rates to auto loan rates will go up.

A minority of thinly stretched borrowers can cause harm to the majority who have their finances in order. During the global financial crisis, even some of the elites decided to stop paying their mortgages, despite having the money.

Seeing prices fall by 8%+ in your local housing market is easy to see, especially if your housing market showed the most robust gains in 2020 and 2021. Prices in Boise and Austin could easily fall by 20% from their peaks before bottoming if the Fed stays aggressive.

Biggest Upside Risk To My Negative Housing Price Forecast: Stealth Wealth

I may be underestimating the amount of liquid wealth potential buyers are secretly holding. Further, I may also be underestimating how much demand will return to the housing market if mortgage rates do decline by 2% – 3% in 2023.

Personally, I have a lot of cash and short-term Treasury bonds. So do all of my friends. I have a feeling, many Financial Samurai readers have an elevated amount of cash as well.

If many of us are going to be hunting for housing deals in 2023, will housing prices really decline by my forecasted 8%? Maybe not.

When it comes to housing prices, prices tend to get bid up quicker than they fall due to real estate FOMO. Hence, buyers might only have a six-month window remaining to take advantage of big price discounts.

Mortgage Demand Highly Sensitive To Even High Rates

Take a look at this chart below. It shows a surge in mortgage purchase applications as the average 30-year fixed rate fell from 7.1% in October 2022 to 6.3% in mid-December 2022. 6.3% is still high compared to a year ago. Yet mortgage purchase applications still went up 13.8%. That’s surprising during the slow winter months.

Hence, if mortgage rates fall to 4% – 5% by mid-2023, perhaps we will see a 25%+ increase in mortgage purchase applications. The longer the inactivity in real estate transactions, the greater the pent-up demand.

There Will Always Be Opportunities

Real estate continues to be my favorite asset class to build wealth for most people.

Even if all my properties were to decline by 10% on average in 2023, I won’t care because I won’t feel it. I will continue to raise my family in our primary residence. Then I’ll continue to collect my rental income to help pay for our lifestyles.

An asset that provides both income and utility is the best type of asset class to own. However, tenant headaches, maintenance issues, and property taxes can get to even the most patient of real estate investors. As a result, a diversification of investments into stocks, private real estate, bonds, and alternatives that provide truly passive income is recommended.

If you want to buy real estate in 2023, there will be plenty of opportunities to do so at more reasonable prices. The combination of declines in both housing prices and mortgage rates will make real estate more attractive by the middle of 2023. Be patient.

When that time comes, I just hope nobody bids against me. Being able to buy my current forever home after the lockdowns began on March 18, 2020, was ideal. If I had faced competition, I would have easily paid 4% more.

Reader Questions And Suggestions

Readers, what are your housing price forecasts for 2023 and why? Are you planning on hunting for deals in 2023? What would cause you to sell your property in 2023?

If you want to invest in real estate more surgically, take a look at Fundrise. I just had an hour-long conversation with Ben Miller, CEO of Fundrise. Its income fund is generating an 8%+ yield. Further, Fundrise is using its existing cash to hunt for distressed deals with 12-14% yields. Our views about 2023 housing prices are very similar.

For more nuanced personal finance content, join 55,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Inflation Forecasts Were Wrong Last Year. Should We Believe Them Now?

At this time last year, economists were hopeful that snarls in global shipping and manufacturing would soon clear; consumer spending would shift away from goods and back to services; and the combination would allow supply and demand to come back into balance, slowing price increases on everything from cars to couches. That has happened, but only gradually. It has also taken longer to translate into lower consumer prices than some economists had expected.

Inflation F.A.Q.

Card 1 of 5

What is inflation? Inflation is a loss of purchasing power over time, meaning your dollar will not go as far tomorrow as it did today. It is typically expressed as the annual change in prices for everyday goods and services such as food, furniture, apparel, transportation and toys.

But the expected shift is finally, if belatedly, showing up. After months of supply chain healing, consumers are now beginning to feel the benefit. Used car prices began declining meaningfully in October inflation data, furniture prices are slumping and apparel is falling in price. Similar cost declines are expected to weigh on inflation next year.

“It is far too early to declare goods inflation vanquished, but if current trends continue, goods prices should begin to exert downward pressure on overall inflation in coming months,” Jerome H. Powell, the Fed chair, said during a recent speech.

The Fed is working on cooling demand.

Unfortunately, moderation in goods prices alone would probably fail to return America to a normal inflation rate, because price increases for services have been accelerating. That category — which covers everything from meals out to monthly rent — accounted for half of consumer price inflation in October, based on a Bloomberg breakdown, up from less than a third a year earlier.

Many types of service inflation are closely intertwined with what’s happening in the job market. For companies including hair salons, restaurant chains and tax accountants, paying employees is typically a major, if not the biggest, cost of doing business. When workers are scarce and wages are climbing rapidly, businesses are more likely to raise their prices to try to cover heftier labor bills.

That means that today’s very low unemployment and abnormally rapid wage growth could help to keep price increases faster than usual, even though the job market wasn’t a big driver of the initial burst in inflation.

That is where Fed policy could come in. Companies can only charge more if their customers are able — and willing — to pay more. The Fed can stop that chain reaction by lifting interest rates to slow demand.

Amazon Stock Slides After it Gives Weak Outlook Amid Recession Fears

Amazon.com Inc.

AMZN -4.06%

projected sales in the current quarter would be far below expectations, sending its stock plunging and offering the latest stark sign of how shifting economic forces are battering tech giants that thrived during the pandemic.

The company on Thursday said sales in the recently completed third quarter rose 15% from a year earlier, while net income was $2.9 billion—its first quarterly profit in 2022, though still a 9% decline from the same period last year.

The e-commerce giant jolted investors with its projection for revenue of $140 billion to $148 billion in the current period—analysts had expected more than $155 billion, according to FactSet. Amazon, which said the estimate includes a sizable hit from foreign-exchange factors, also said it anticipated operating income of anywhere between zero and $4 billion, reflecting the uncertainty looming over what is traditionally its biggest quarter of the year because of holiday shopping.

The company’s shares fell more than 12% in after-hours trading following the results to trade near $97. At that level, Amazon’s valuation is below $1 trillion, which it first hit in 2018.

The disappointing outlook capped an extraordinary several days that also saw shares of other tech giants plummet after their results showed worsening conditions in a range of areas.

Shares of

parent Meta Platforms Inc., already battered over the past year, dropped nearly 25% on Thursday after it reported its second quarterly revenue decline in a row a day earlier.

Microsoft Corp.’s

stock also fell after it delivered on Tuesday its worst net income decline in more than two years and the weakest revenue growth in over five years. Google-parent

Alphabet Inc.

similarly disappointed investors with slowing sales.

These tech companies flourished during the pandemic, as life and work suddenly shifted more to the internet, pushing up sales and spurring the already fast-growing companies to accelerate hiring and investment.

Now, one after another, engines that drove that growth are sputtering. Sales of personal computers and other gadgets are falling. Consumers, walloped by inflation, are broadly trimming their spending, while companies are tightening their outlays for everything from digital ads to IT services.

“There is obviously a lot happening in the macroeconomic environment, and we’ll balance our investments to be more streamlined without compromising our key long-term, strategic bets,” Amazon Chief Executive

Andy Jassy

said Thursday.

In the third quarter, Amazon’s online store sales rose 7% to $53.48 billion after falling in recent quarters. The segment includes product sales primarily on its flagship site and digital media content. Its online sales got a boost from its annual Prime Day sale, which this year fell in the third quarter where last year it was in the second quarter.

While still the nation’s largest online store, Amazon’s e-commerce division has struggled to grow this year. The company in the second quarter reported a 4% year-over-year drop in its online stores segment. That marked the largest drop since the metric was first reported in 2016.

This year, Amazon’s e-commerce machine—which has grown at breakneck speed for decade—has been showing signs that it could be entering a phase of slower growth. After a multibillion-dollar infrastructure build-out and hiring spree, it now has to contend with high inflation and concerns about a recession weighing on consumer spending.

Chief Financial Officer

Brian Olsavsky

said the company has entered a period of caution.

“We are preparing for what could be a slower growth period like most companies. We are going to be very careful on our hiring,” Mr. Olsavsky said during a call with reporters Thursday. “We certainly are looking at our cost structure and looking for areas where we can save money.”

He said Amazon is “seeing signs all around that people’s budgets are tight, inflation is still high.”

Analysts say the new challenges Amazon faces in e-commerce could linger.

Amazon has the largest share of online commerce, about 38%, but its market share has plateaued in recent years, according to market research firm Insider Intelligence. Analysts say the company’s size has made it unlikely the e-commerce unit’s growth would hit the same pace it once did. Amazon also is dealing with increased competition from

Walmart Inc.,

Target Corp.

and others.

Mr. Jassy has shifted toward cost-cutting. The company cut back on subleasing millions of square feet of excess warehouse space and put off opening new facilities while earlier thinning out its hourly workforce through attrition.

It enacted a hiring freeze through the end of the year at its corporate retail division, the segment that drives core sales and is responsible for a large part of this year’s slowdown. The company has paused hiring among some teams at its Amazon Web Services cloud-computing division.

While Amazon’s earnings continue to be aided by AWS and its expanding advertising business, growth slowed in the cloud business. AWS had sales of $20.5 billion during the third quarter, a 27% rise but one of the lowest rates of growth posted by the unit in recent quarters. Mr. Olsavsky said the company saw AWS customers “working to cut their bills.”

Amazon’s advertising revenues rose 25% to $9.5 billion.

Amazon is headed toward the end of the year with added challenges. After needing fewer blue-collar employees earlier in the year, it has looked to add more than 100,000 workers at its warehouses to meet the expected holiday demand. Still, that strategy has come with a cost. Amazon recently said it would spend $1 billion to raise average starting salaries to $19 an hour nationwide and is earmarking millions to raise wages and benefits for its delivery employees.

Consumers will be more likely to return to bricks-and-mortar stores for their holiday shopping this year, and economic concerns will likely weigh on spending, according to analysts. Amazon’s own

Jeff Bezos

seemed cautious about the future. He recently said it is time to “batten down the hatches,” referring to warning signs that the U.S. is headed for a recession.

Write to Sebastian Herrera at sebastian.herrera@wsj.com

Copyright ©2022 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

BYD shares jump after Chinese EV maker forecasts surging profits

Warren Buffett-backed BYD said it expects a more than 300% jump in third-quarter profit. Despite headwinds including a resurgence of Covid in China, rising material costs and a slowing economy, BYD has remained fairly resilient.

Nathan Laine | Bloomberg | Getty Images

Shares of Chinese electric carmaker BYD rose Tuesday after the company forecast a huge jump in profit for the third quarter.

Late Monday, the Warren Buffett-backed firm said net profit in the three months to Sept. 30 is estimated to be between 5.5 billion yuan to 5.9 billion yuan ($764.5 million to $820 million), a rise of 333.6% to 365.11% versus the same period last year.

BYD’s Hong Kong-listed shares were 5.6% higher in afternoon trade.

“In the third quarter of 2022, despite the complex and severe economic situation, the spread of the pandemic, extreme high temperature weather, high commodity prices and other unfavorable factors, the new energy vehicle industry continued to accelerate its upward trend,” BYD said in a statement.

The company said sales volume of its new energy vehicles, which include electric cars, “continued to reach record highs” helping boost market share and “driving significant improvement in earnings and effectively relieving the pressure on earnings brought by the rising prices of upstream raw materials.”

A number of electric carmakers from Tesla to BYD to have been grappling with the rising cost of raw materials, such as lithium, that are critical to batteries.

From the start of the year to the end of September, BYD has sold 1.18 million new energy vehicles, trumping Tesla’s figure of just over 900,000 deliveries.

BYDs various models are among the top-selling new energy vehicles in China which is the world’s largest electric car market.

While the Shenzhen-headquartered company has remained fairly resilient in the face of headwinds such as a resurgence of Covid in China and a slowing economy, its smaller rivals have faced difficulties.

In August, Chinese electric car start-up Xpeng reported weak vehicle delivery guidance for the third quarter.

Wall Street banks’ profits slide as economic clouds loom, some beat forecasts

Oct 14 (Reuters) – Profits slid at Wall Street’s biggest banks in the third quarter as they braced for a weaker economy while investment banking was hit hard, but investors saw a silver lining with some banks beating estimates.

JPMorgan Chase & Co (JPM.N), Morgan Stanley (MS.N), Citigroup Inc (C.N) and Wells Fargo & Co’s (WFC.N) showed a slide in net income after turbulent markets choked off investment banking activity and lenders set aside more rainy-day funds to cover losses from borrowers who fall behind on payments.

“We’re in an environment where it’s kind of odd,” said JPMorgan Chief Executive Officer Jamie Dimon, who said that while the bank was “hoping for the best, we always remain vigilant and are prepared for bad outcomes.”

Register now for FREE unlimited access to Reuters.com

Central banks globally have been battling surging inflation which is expected to cause an economic slowdown. The Federal Reserve has raised the benchmark interest rate from near zero in March to the current range of 3.00% to 3.25% and signaled more increases.

Rising rates tend to buoy bank profits, but the broader risk of an economic downturn sparked by high inflation, supply-chain bottlenecks and the war in Ukraine could weigh on future earnings.

On a conference call, Dimon said U.S. consumers remained strong and he wasn’t predicting a recession but “there are a lot of headwinds out there.”

Money that people have in their checking accounts will “deplete probably by sometime midyear next year” while they are contending with headwinds like inflation, higher rates and higher mortgage rates, he cautioned.

Banks set aside more money in preparation for a hit from a potential economic slowdown. JPMorgan set aside $808 million in reserves, Citi added $370 million to reserves and Wells had a $385 million increase in the allowance for credit losses.

Still, shares of JPMorgan and Wells Fargo gained strongly, up 2.5% and 3.7% respectively while Citi gained 1.2% as the profit falls were not as deep as feared.

JPM also said it hopes to be able to resume stock buybacks early next year, although other banks were less bullish with Citi saying buybacks continue to be on hold and Wells Fargo saying it continues to be prudent about buybacks.

“JPMorgan delivered a solid set of results, from top to bottom,” Susan Roth Katzke, an analyst at Credit Suisse, wrote in a note. “At least equally as important is the evidence of preparedness to manage through whatever turn the macro takes; expect the latter to be in focus.”

JPMorgan reported a 17% drop in third-quarter profit to $9.74 billion, although that was less than had been feared. Wells Fargo posted a 31% decline to $3.53 billion but it also beat expectations. And Citi reported a 25% drop to $3.5 billion which also beat expectations.

“Most of these banks are making more spread income now than ever because of the change in interest rates,” said Chris Marinac, Director of Research at Janney Montgomery Scott. “And this was the first quarter where you had the full effect of the Fed, because the Fed increased a little bit in May.”

Signage is seen at the JPMorgan Chase & Co. New York Head Quarters in Manhattan, New York City, U.S., June 30, 2022. REUTERS/Andrew Kelly

JPMorgan said net interest income rose 34% to a record $17.6 billion, up 34%.

“Generally banks obviously seem to be benefiting from a higher rate environment, and we’ve obviously seen banks able to earn, in terms of revenues, on higher interest rates,” said Eric Theoret, global macro strategist at Manulife Investment Management.

Marinac said investors would want to see banks build reserves at this point in the economic cycle.

“They’re bracing for a hard landing, because they’re building the reserves,” said Marinac. “But that’s not necessarily a bad thing.”

While a number of the banks managed to beat expectations, Morgan Stanley reported a 30% slump in profit to $2.49 billion which missed estimates. Its shares fell 5%.

Morgan Stanley’s earnings showed that investment banking revenue more than halved to $1.3 billion with declines across the bank’s advisory, equity and fixed income segments.

James Gorman, Chairman and Chief Executive Officer of Morgan Stanley, said his firm’s performance was “resilient and balanced in an uncertain and difficult environment.”

Corporations’ interest in mergers, acquisitions and initial public offerings dried up, particularly hitting banks strong in investment banking. Global M&A lost ground in the third quarter with volumes in the United States plummeting nearly 63% as the rising cost of debt forced companies to postpone big buyouts.

While banks were optimistic they could weather the likely tougher economy ahead, some observers were concerned about the long term outlook for growth.

“Against the backdrop of economic headwinds, the solid earnings reports from this morning will quickly pass into the rearview mirror,” said Peter Torrente, KPMG US National Sector Leader for Banking and Capital Markets. “Worries of inflation, which shows little sign of slowing down, are casting a long shadow on future outlook.”

Torrente said while banks’ revenues reflect the benefit of rising interest rates and persisting loan demand, the buildup in loan loss provisions also reflects the uncertainty in the road ahead.

“Next quarter and beyond, credit risk, loan growth, and deposit balances will be key areas to monitor in the banking industry,” Torrente said.

Register now for FREE unlimited access to Reuters.com

Reporting by Saeed Azhar and Lananh Nguyen and Davide Barbuscia in New York, Noor Zainab Hussain, Niket Nishant, Mehnaz Yasmin, Sweta Singh and Manya Saini in Bengaluru

Writing by Megan Davies

Editing by Lananh Nguyen, Mark Potter, David Gregorio and Chizu Nomiyama

Our Standards: The Thomson Reuters Trust Principles.

IMF forecasts ‘very painful’ outlook for global economy

The IMF has said there is a growing risk that the global economy will slide into recession next year as households and businesses in most countries face “stormy waters”.

China’s zero-Covid policy and fragile housing market, the need to raise interest rates to control inflation in advanced economies, and higher energy and food prices following Russia’s invasion of Ukraine will lower world economic growth from 3.2 per cent in 2022 to 2.7 per cent next year, the fund predicted.

The growth forecast for 2023 is the lowest for the year ahead that the IMF has published since 2001, apart from the years of the coronavirus pandemic and following the global financial crisis.

The fund’s economists judged that there was a greater than even chance that the world economy would perform worse than its central forecast and a 25 per cent chance that growth would fall below 2 per cent. That would represent global economic weakness seen only one year in 10 and only in 1973, 1981, 1982, 2009 and 2020 over the past half a century.

In an interview with the Financial Times, Pierre Olivier Gourinchas, the IMF’s chief economist, said there was as much as a 15 per cent chance global growth could fall below 1 per cent eventually. This level would likely meet the threshold of a recession and would be “very, very painful for a lot of people”.

“We are not in a crisis yet, but things are really not looking good,” he said, adding that 2023 would be the “darkest hour” for the global economy.

Financial turmoil, triggered by a shift into dollar assets, threatened to compound the economic threat.

“As the global economy is headed for stormy waters, financial turmoil may well erupt, prompting investors to seek the protection of safe-haven investments, such as US Treasuries, and pushing the dollar even higher,” Gourinchas added in his statement that accompanied the report.

Although the sharp rises in interest rates around the world were weighing on growth, the IMF said they were necessary to ensure inflation came back under control and restored the global economy to a more stable footing.

The fund forecasts inflation in advanced economies will hit 7.2 per cent this year and 4.4 per cent next year, both more than 1 percentage point higher than its previous April forecasts for 2023. For emerging and developing economies, consumer price growth will peak at an annual pace of almost 10 per cent this year before moderating to 8.1 per cent in 2023.

“On the front lines, you have the central banks. That’s their job, that’s their mandate [and] their whole reputation is at stake,” said Gourinchas. The fund said that monetary authorities must “stay the course” rather than repeat the mistakes of the 1970s when most monetary policymakers did not have the nerve to keep raising interest rates when their economies slowed or stalled.

There was a chance of tightening monetary policy too much, the IMF admitted, but it said the risks of doing too much were not as serious as letting inflation become normalised and ingrained into everyday life.

For the US Federal Reserve in particular, Gourinchas warned it was too soon for it to back off from its aggressive campaign to tighten monetary policy.

“We are far from having won that battle,” said the chief economist, adding that any signal that the Fed would not raise rates further could, at this point, be interpreted by financial markets as a sign policymakers were unwilling “to do what it takes”.

“Inflation expectations could de-anchor and we could have a more persistent process,” he said.

The IMF expanded on its recent criticism of UK economic policy, advising all countries not to have highly expansionary policies of taxation and public spending, despite the surge in energy and food prices.

There was a need to lower deficits and rebuild fiscal buffers, Gourinchas said. “Doing otherwise will only prolong the fight to bring inflation down, risk de-anchoring inflation expectations, increase funding costs, and stoke further financial instability, complicating the task of fiscal as well as monetary and financial authorities, as recent events illustrated,” he said in his statement.

Likening it to two drivers, each with their own steering wheels, Gourinchas told the FT that opposing fiscal and monetary policies prompted financial markets to question, “which way is that car going? Are we really fighting inflation or are we really stimulating economic activity?”

In the revised forecasts, 93 per cent of countries received downgrades to their growth outlook.

The 2022 global growth forecast has declined from 4.9 per cent in the fund’s report a year ago to 3.2 per cent now. The 2023 growth estimate was cut from 3.6 per cent a year ago to 2.3 per cent, with the downgrades concentrated in advanced economies rather than in the emerging world.

In what will be a difficult report for Beijing’s government as it prepared for the 20th national congress of the Communist party, China’s economy was forecast to grow only 4.4 per cent this year, well below the government’s 5.5 per cent growth target. The IMF expects this annual growth rate to improve only to 4.6 per cent over the next five years.

The US economy is expected to stagnate over the four quarters of 2022 and then maintain a sluggish 1 per cent growth rate in 2023. Many European countries will fall into recession, the IMF predicted, as households and companies struggle to cope with natural gas prices five times 2021 levels.

The fund was no more optimistic about the future. The downgrades were likely to be permanent, it said. Scarring from the pandemic and war in Ukraine would leave the global economy 4.3 per cent smaller in 2024 than it expected in January 2020 as coronavirus began to spread globally.

Strong New-Car Demand Collides With Rising Interest Rates

Auto executives for months have expressed confidence there will be eager buyers for all the vehicles they can build. A worsening economic picture is putting that theory to the test.

The U.S. auto industry is expected to report flat new-car sales for the third-quarter, despite earlier predictions that this year’s depressed selling pace would accelerate in the second half, analysts predict. Most auto makers are scheduled to report third-quarter sales results Monday.

Tight supplies continue to be the big problem, car executives and dealers say, as a shortage of computer chips and other supply-chain snags continue to dog vehicle output and curb sales.

Still, there are signs the backlog of demand built up over the last 18 months could deteriorate as consumers feel the pinch of higher interest rates, analysts say.

“It seems likely that much of the pent-up demand from limited supply is quickly disappearing as high interest rates eat away at vehicle buyers’ willingness and ability to purchase,” said

Charlie Chesbrough,

senior economist with research firm Cox Automotive.

Car companies and dealers say that most new vehicles that get shipped from the factory are quickly snapped up by buyers.

Photo:

Brandon Bell/Getty Images

The firm last week lowered its 2022 U.S. sales forecast, to 13.7 million new vehicles, which would be down 9% from last year. In the five years leading up to the pandemic-plagued year of 2020, the industry sold more than 17 million vehicles annually.

So far, though, car companies and dealers say that most new vehicles that get shipped from the factory are quickly snapped up by buyers.

“There is still really strong consumer demand, and huge replacement demand,” said

Duncan Aldred,

head of

General Motors Co.

GM -3.52%

’s Buick and GMC brands, during an interview at the Detroit auto show last month. “I think that will probably overcome a lot of the economic headwinds.”

SHARE YOUR THOUGHTS

Are you planning to buy a car this year, or are higher interest rates making you rethink your plan? Join the conversation below.

Auto makers and dealers continue to pull in strong profits, as the tight supplies keep prices at or near record highs. The average price paid by U.S. car buyers in the third quarter hit $45,971, up 10% from a year earlier and the most for any quarter on record, according to research firm J.D. Power.

But there are signs that rising interest rates are starting to strain car buyers, which could pressure pricing. The average interest rate paid on a new vehicle purchase hit 5.7% in September, up from around 4% a year earlier, J.D. Power said.

This past week,

CarMax Inc.

KMX 1.32%

shares sank after the used-car retailer flagged that high prices, paired with high broader inflation and rising interest rates, have slowed demand. The company’s profit fell 50% in its most recent quarter and its sales leveled off at 2% growth, both worse than analysts expected.

“This points to some deterioration in per unit pricing and profitability in the coming quarters, as rising interest rates and economic conditions affect demand,” said

Thomas King,

president of the data and analytics division at J.D. Power.

Write to Mike Colias at mike.colias@wsj.com

Copyright ©2022 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8