The China Evergrande Centre building sign is seen in Hong Kong, China December 7, 2021. REUTERS/Tyrone Siu

Register now for FREE unlimited access to Reuters.com

Register

HONG KONG, March 21 (Reuters) – Shares of embattled property developer China Evergrande Group (3333.HK) and onshore bonds issued by its flagship unit Hengda Real Estate Group were suspended from trading on Monday, pending an announcement by the company.

Trading was also halted in shares of its property services unit, Evergrande Property Services Group Ltd (6666.HK), and electric vehicle unit, China Evergrande New Energy Vehicle Group Ltd (0708.HK), exchange filings showed.

The filings gave no further details.

Register now for FREE unlimited access to Reuters.com

Register

Evergrande, the world’s most indebted developer with over $300 billion in liabilities, has been struggling to repay its suppliers and creditors and complete projects and homes.

Hengda secured approval from its onshore bondholders over the weekend to delay a coupon payment due last September to September 2022, according to a filing by the company’s lawyer to the Shenzhen Stock Exchange on Sunday.

Hengda held a meeting with creditors of the 4 billion yuan ($629 million) 2025 bond on March 18-19 to approve the payment of interests incurred between September 2020 to September 2021 to be made in September 2023. read more

Evergrande has so far avoided technical bond defaults onshore, though it has missed payments on some offshore bonds.

Evergrande shares traded at HK$1.65 before the suspension. They have gained 3.8% this year after plunging 89% in 2021.

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Clare Jim and Donny Kwok in Hong Kong, Beijing newsroom; Editing by Himani Sarkar

Our Standards: The Thomson Reuters Trust Principles.

The company logo is seen on the headquarters of China Evergrande Group in Shenzhen, Guangdong province, China September 26, 2021. REUTERS/Aly Song

Register now for FREE unlimited access to Reuters.com

Register

HONG KONG, Jan 26 (Reuters) – China Evergrande Group (3333.HK) and its financial advisers will hold a call with investors at 9 pm (1300 GMT) on Wednesday, sources said, the first such call since it defaulted on some dollar bond payments last month.

Evergrande, once China’s top selling real estate developer, has more than $300 billion in liabilities, including nearly $20 billion of international bonds all deemed to be in default.

Its debt crisis has engulfed other Chinese developers and roiled global financial markets over the past year, and contributed to a sharp slump in China’s property market. read more

Register now for FREE unlimited access to Reuters.com

Register

Newly appointed company executive director Siu Shawn, who is also the chairman of Evergrande New Energy Vehicle Group Limited (0708.HK), and a member of the property developer’s risk management committee, Chen Yong, will join the call, the sources said, speaking on condition of anonymity.

Chen is a compliance director of state-owned Guosen Securities. Andrew Huang, Evergrande’s Hong Kong branch general manager, will also be present on the call.

Evergrande set up the risk management committee in December with mostly members from state enterprises, as the Guangdong provincial government leads the work on the firm’s restructuring.

The embattled firm on Monday sought more time from its offshore bondholders to work on a “comprehensive” and “effective” debt restructuring plan, after a group of Evergrande’s offshore creditors said they were ready to take “all necessary actions” to defend their rights if the company did not show more urgency to resolve a default. read more

Evergrande has also asked the bondholders to disclose their holdings by mid-this week to identify investors for communications, and hired more financial and legal advisers to follow up with demands from creditors. read more

Shares of Evergrande closed up 1.7% on Wednesday, while its defaulted dollar bond due April 2022 dropped to 15.997 cents on the dollar from 17.074 overnight, according to data by Duration Finance.

Rating agency Moody’s said in a report on Wednesday that covenant packages in Evergrande’s offshore issuances had become increasingly lax, loosening or eliminating key protections, and putting the recovery prospects for offshore bondholders in peril.

Offshore bondholders rank behind the creditors of Evergrande’s over 1,950 onshore subsidiaries, Moody’s added, and none of which guarantee the offshore bonds.

The agency said the weakened covenants and increased size of debt carve-outs have allowed the firm to increase leverage materially.

“Flexible covenants have left Evergrande and other Chinese property developers with a corporate family rating of B3 negative and below vulnerable to the highly cyclical nature of China’s real estate market,” Jake Avayou, a Moody’s vice president and senior covenant officer, said in the report.

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Clare Jim in Hong Kong and Jason Xue in Shanghai; Editing by Clarence Fernandez and Kim Coghill

Our Standards: The Thomson Reuters Trust Principles.

A man walks past a wall carrying the logo of Shimao Group, with residential buildings and the financial district of Pudong seen in the background, in Shanghai, China January 1, 2013. Picture taken January 1, 2013. REUTERS/Stringer

Register now for FREE unlimited access to Reuters.com

Register

Shimao puts assets on the block, ratings slashed again

Evergrande extends deadline for bond payment deferral

R&F next in focus with $750 mln debt payment on Thursday

HONG KONG/LONDON, Jan 10 (Reuters) – China’s property sector saw more drama on Monday after reports Shimao – investment grade-rated until a couple of months ago – had put all its projects up for sale, and Evergrande attempted to avoid another high-profile default.

More unwelcome surprises this month have meant no let up in the Chinese property crisis that wiped over a trillion dollars off the sector last year.

Monday’s twists saw Shimao Group’s credit rating cut again by both S&P and Moody’s after it unexpectedly defaulted on a “trust loan” last week, although its shares surged nearly 20% (0813.HK) on reports it was in talks about asset sales with state-backed giant China Vanke. read more

Register now for FREE unlimited access to Reuters.com

Register

China Evergrande (3333.HK), the world’s most indebted developer that first triggered the turmoil last year, said it had moved out of its Shenzhen headquarters to cut costs. read more

The company kept a glimmer of hope alive that its first “onshore” Chinese yuan bond default might still be avoided by extending until Thursday a deadline for bondholders to agree to a six-month, 4.5 billion yuan ($157 million) payment deferral. read more

Chinese property firms have faced unprecedented pressure over the last six months following efforts by Beijing to curb overborrowing in the sector.

Reuters reported last week that the government now plans to make it easier for state-backed property developers to buy up assets of struggling private rivals. read more

But the sector’s cash crunch is expected to intensify too with firms needing to make nearly $40 billion of international bond payments over the next six months according to brokerage Nomura, including almost $1.5 billion this week alone.

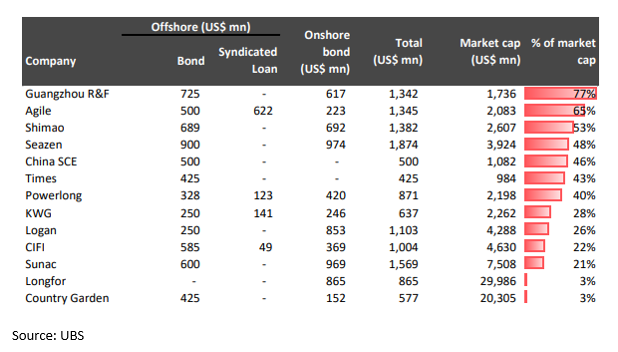

One of those likely to be highlighted alongside Evergrande on Thursday will be Guangzhou R&F Properties (2777.HK). Its bonds have slumped to deeply distressed levels ahead of a $750 million bond payment due that day . It also has a number of unfinished mega projects in global cities like London.

“I think the worst might be yet to come” said Himanshu Porwal, emerging markets corporate credit analyst at Seaport Global.

“A lot will depend on what the Chinese government does in terms of liquidity measures… But it has been four months already so I don’t know what they would be waiting for.”

China high yield crushed by property collapse

NEW LOWS

The woes of recent days have seen ICE’s China high-yield debt index (.MERACYC), which is dominated by homebuilders, hit an all-time low, while Evergrande and fellow-defaulter Kaisa have seen their bonds ejected from J.P. Morgan’s closely followed emerging market corporate debt index.

S&P and Moody’s both cut Shimao’s rating deeper into the junk category on Monday and warned of potential for a further downgrade.

S&P, which had rated Shimao investment grade as recently as November, cut it by a full two notches. It said, “The decline is worse than we previously anticipated. We now assess the company’s liquidity to be weak.”

Moody’s and Fitch also downgraded Yuzhou Group (1628.HK) due to increased refinancing risk while Moody’s withdrew the rating of another firm, Yango, due to “insufficient information.”

Separately, small developer Modern Land (1107.HK), which missed payment for its 12.85% notes due in October said in a filing on Monday that it has received notices from certain noteholders demanding early repayment of their senior notes.

The developer said it has been discussing a waiver with these creditors and has appointed financial advisers to formulate a plan. It is also in talks on a restructuring plan for $1.3 billion of its offshore bonds, the firm added.

Modern Land shares, which resumed trading after being suspended since Oct. 21, sank 40% in Hong Kong to HK$0.23.

“It’s going to be the peak of repayment period and we’ll see more developers default,” said Kington Lin, managing director of the asset management department at Canfield Securities Limited.

“The market is watching how many SOEs (state-owned enterprises) will get more M&A loans to help the developers in distress.”

Chinese property firms face big bills

(This story refiles to add dropped letter in first paragraph)

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Clare Jim and Donny Kwok in Hong Kong, Samuel Shen in Shanghai and Marc Jones in London; ; Editing by Kim Coghill, Shri Navaratnam, Tomasz Janowski and Cynthia Osterman

Our Standards: The Thomson Reuters Trust Principles.

Chinese media reported over the weekend that authorities in Hainan province — a tropical resort island off the coast of southern China — ordered Evergrande to demolish 39 buildings,saying that the building permits had been illegally obtained.

The company acknowledged the order in a post on WeChat on Monday night, noting that it did not affect other buildings in the same property project, which involve some 61,000 property owners.

The 39 buildings are part of Evergrande’s gigantic Ocean Flower Island project in Hainan, inwhich the company has invested nearly $13 billion over the last six years.

The company suspended trading in Hong Kong on Monday, without elaborating. Ina filing with the Hong Kong Stock Exchange on Tuesday, the company said it would resume trading in the afternoon, and confirmed that it would “actively communicate” with authorities about the Ocean Flower Island project and“resolve the issue properly.”

Shares surged as much as 10% after trading started in early afternoon, before paring gains. They were last up 1.3%.

In Tuesday’s filing, Evergrande also said it has achieved contracted sales of 443.02 billion yuan ($70 billion) for 2021. That was down 39% from 2020’s sales figure. And regarding liquidity, the company said it would continue to “actively maintain communication with creditors, strive to resolve risks and safeguard the legitimate rights and interests of all parties.”

Evergrande — which was China’s second largest property developers by sales in 2020 — is reeling under more than $300 billion of total liabilities.

It has been scrambling for months to raise cash to repay lenders, and the company’s chairman Xu Jiayin has been reportedly selling off personal assets to prop up its finances. But that doesn’t seem enough to avoid default.

In December, Fitch Ratings declared that the company had defaulted on its debt, a downgrade the credit ratings agency said reflected Evergrande’s inability to pay interest due that month on two dollar-denominated bonds.

Analysts have been long concerned that a collapse by Evergrande could trigger wider risks for China’s property market, hurting homeowners and the broader financial system. Real estate and related industries account for as much as 30% of the country’s GDP. The US Federal Reserve warned in November that trouble in Chinese real estate could damage the global economy.

There’s already plenty of evidence that Beijing is taking a leading role in guiding Evergrande through a restructuring of its debt and sprawling business operations.

But analysts warned, though, that the real estate crisis remains a looming threat for China.

An exterior view of China Evergrande Centre in Hong Kong, China March 26, 2018.

Bobby Yip | Reuters

BEIJING — Indebted property developer China Evergrande’s contracted sales plunged last year as the real estate giant struggled to repay creditors.

A filing Tuesday showed the company’s contracted sales of properties totaled 443.02 billion yuan ($69.22 billion) last year, down 38.7% from the 723.25 billion yuan in contracted sales reported for 2020.

Evergrande shares reopened higher in Hong Kong on Tuesday afternoon, with shares trying to hold gains of about 3% before turning lower.

Trading was halted as of 9 a.m. Monday, with shares at 1.59 Hong Kong dollars (20 cents) each. That’s just above the all-time intraday low of 1.42 Hong Kong dollars per share set on Dec. 24, according to FactSet.

The company added it “will continue to actively maintain communication with creditors, strive to resolve risks and safeguard the legitimate rights and interests of all parties.”

Read more about China from CNBC Pro

Evergrande shares have plunged more than 88% over the last 250 trading days. The company missed payments to creditors in December, Fitch Ratings said, sending the developer into default.

Evergrande is the largest Chinese real estate developer by issuance of offshore, U.S. dollar-denominated debt, which stood at $19 billion last year. The developer had a total of $300 billion in liabilities as of last year.

The company was China’s second largest developer by sales in 2020.

Like other Chinese real estate developers, Evergrande’s business model relies heavily on sales of apartments to customers before the units are completed. S&P Global Ratings said in November that an Evergrande default “is highly likely” since the company is no longer able to sell new homes.

Evergrande added that a demolition order for its Ocean Flower Island project only applied to 39 buildings, according to Tuesday’s filing with the Hong Kong stock exchange.

This is breaking news. Please check back for updates.

Evergrande said in a filing to the Hong Kong Stock Exchange that its trading halt was pending an “announcement containing inside information,” though it did not elaborate.

The company hasabout $300 billion in total liabilities, and analysts have worried for months about whether a collapse could trigger a wider crisis in China’s property market, hurting homeowners and the broader financial system. The US Federal Reserve warned last year that trouble in Chinese real estate could damage the global economy.

In December, Fitch Ratings declared that the company had defaulted on its debt, a downgrade the credit ratings agency said reflected Evergrande’s inability to pay interest due that month on two dollar-denominated bonds.

The company’s stock was rattled last week after more debt payment deadlines passed without signs that it had met its obligations, though it reportedly has a 30-day grace period to pay those debts. (Fitch’s downgrade came when Evergrande appeared to miss payments after their grace periods lapsed.)

Evergrande did not respond to a request for commentabout its decision to halt shares Monday.

The company has had some other setbacks recently, too. Local media recently reported that authorities in Hainan province — a tropical resort island off the coast of southern China — ordered Evergrande to demolish 39 buildings. The company acknowledged the order in a post on WeChat, noting that it did not affect the plots and buildings of some 61,000 property owners. It added that it would “actively communicate and handle properly in accordance with the guidance of the decision letter.”

While the company’s financial woes have been mounting, it did have some positive news last month, saying ithad made initial progress in resuming construction work. The company’s chairman Hui Ka Yan said that no one at the firm would be allowed to “lie flat” and vowed to deliver 39,000 units of properties in December.

Thatnumber was a massive jump compared with the fewer than 10,000 units the company had delivered in each of the previous three months.

And, there are signs that Chinese authorities are taking steps to contain fallout from the company’s downward spiral and guide it through a restructuring of its debt and business operations.

Evergrande announced in December it would set up a risk management committee, including government representatives, to focus on “mitigating and eliminating” future risks. Among its members are top officials from major state-owned enterprises in Guangdong, as well as an executive from a major bad debt manager owned by the central government.

The People’s Bank of China also said it would pump $188 billion into the economy, apparently to counter the real estate slump, which accounts for nearly a third of China’s GDP.

Trading in the shares of the indebted property developer China Evergrande Group were suspended on the Hong Kong Stock Exchange Monday morning as the company raced to deliver apartments to millions of home buyers and raise cash to manage its $300 billion in debt.

Evergrande said in a filing that its shares were halted pending an announcement “containing inside information,” without giving more details. The company had halted its shares once before, in October, as it tried to finalize the sale of a $2.6 billion stake in its property management unit.

That deal ultimately fell through.

The giant property developer entered into default last month after failing to make a final debt payment to foreign investors. The company owes an estimated 1.6 million apartments to home buyers and is facing dozens of lawsuits.

Although Evergrande has yet to solve its cash squeeze, it pledged last week to finish building 39,000 apartments before the end of 2021. The announcement sent Evergrande shares soaring, but they dropped the next day after the company failed to meet another payment deadline on its foreign debt.

On Friday, Evergrande appeared to revise its plan to repay investors in its wealth management unit, promising to make monthly payments of about $1,260 to each investor for three months. It had previously not given a specific repayment amount. In its statement to wealth management investors on Friday, Evergrande said that it plans to “actively raise funds,” and added that the situation was not “ideal.”

At one point, as many as 80 percent of Evergrande employees were asked to put money into wealth management products to help fund its operations. In September, Evergrande employees, contractors and home buyers protested outside company offices and government buildings.

Government officials joined a risk committee created in December to help steer Evergrande and restructure the company.

HONG KONG, Jan 3 (Reuters) – China Evergrande Group (3333.HK) shares will be suspended from trading on Monday pending the release of “inside information”, the embattled property developer said without elaborating.

Evergrande, the world’s most indebted developer, is struggling to repay more than $300 billion in liabilities, including nearly $20 billion of international market bonds that were deemed to be in cross-default by ratings firms last month after it missed payments.

The property developer missed new coupon payments worth $255 million due last Tuesday < VG162759965=>, though both have a 30-day grace period. read more

Register now for FREE unlimited access to Reuters.com

Register

The firm has set up a risk management committee with many members from state companies, and said it would actively engage with its creditors. read more

Local media reported over the weekend a city government in the Chinese resort island of Hainan had ordered Evergrande on Dec. 30 to demolish its 39 residential buildings within 10 days, due to illegal construction.

The buildings stretched over 435,000 square meters, the reports added, citing an official notice to Evergrande’s unit in Hainan.

Evergrande did not respond to request for comment on the Hainan development.

On Friday, Evergrande dialled back plans to repay investors in its wealth management products, saying each investor in its wealth management product could expect to receive 8,000 yuan ($1,257) per month as principal payment for three months irrespective of when the investment matures. read more

The move highlights the deepening liquidity squeeze at the property developer.

“The market is watching the asset disposal progress from Evergrande to repay its debt, but the process will take time,” said Conita Hung, investment strategy director at Tiger Faith Asset Management.

“And the demolition order in Hainan will hurt the little homebuyer confidence remained in the company.”

Evergrande said last week 91.7% of its national projects have resumed construction after three months of effort. Many projects were halted previously after the developer failed to pay its many suppliers and contractors. read more

Shares of Evergrande shed 89% last year, closing at HK$1.59 on Friday.

Its EV unit China Evergrande New Energy Vehicle Group (0708.HK)reversed early losses to rise 6% by late morning trades on Monday, while property management unit Evergrande Services (6666.HK) declined 3%.

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Clare Jim; Editing by Tom Hogue & Shri Navaratnam

Our Standards: The Thomson Reuters Trust Principles.

To mark the completion of a residential complex called World City, the indebted property giant China Evergrande Group held an elaborate red carpet ceremony on Monday, with eight cannons firing off confetti before a cheering crowd. The company then released a series of images featuring newly completed buildings covered with bright red decorations.

Just weeks earlier, Evergrande had been declared in default. The developer has unpaid bills in excess of $300 billion and has struggled to pay back its creditors and business partners. Some in China saw the company’s celebrations as premature.

For months, Evergrande could not pay its builders, painters and contractors. The company, whose problems have made investors wary of China’s once-flourishing property sector, remained relatively silent as its debt problems led to panic in global markets and among people around the country who had purchased apartments before they were completed.

Construction on more than a million homes stalled, and then, two weeks ago, Evergrande signaled it could no longer go on — officially entering into default after failing to make a final debt payment to foreign investors. Now, the developer has pledged to start paying its workers again and to deliver homes, part of a push to restore confidence in the company and the sector.

“We will sprint at full speed,” Xu Jiayin, Evergrande’s billionaire founder, told top executives on Sunday, according to a statement. He did not provide any details about where the money would come from, nor did he say anything about the failure to pay foreign creditors.

Despite the company’s bullishness, the challenges it faces remain enormous.Some home buyers say they are still in the dark about their unfinished apartments. Former employees and contractors continue to wait for back payments. Dozens of lawsuits from business partners that have piled up in court remain unresolved. Property sales across China, meanwhile, have fallen for five consecutive months.

A few weeks ago, government technocrats stepped in to help steer the company. The head of China’s Ministry of Housing and Urban-Rural Development said last week that Beijing was committed to “guaranteeing home deliveries, protecting people’s livelihoods and maintaining social stability.” With just a few days left in the month, Mr. Xu pledged on Sunday to deliver 39,000 apartment units by the end of the year.

The company has also said that it has restarted partnerships with more than 80 percent of its long-term suppliers of materials, and indicated that it would soon be able to repay its debt and begin sales of new apartments.

Evergrande’s sudden rush of promises has created more questions than answers for the home buyers, suppliers, contractors and creditors who have yet to hear directly from the company. Some people have started to track which of Evergrande’s hundreds of property projects have actually restarted construction.

Li Menghe, the chairman of Qingdao Wanhe Construction & Decoration Group, a glass supplier to Evergrande, has begun using his official Weibo account to post daily details on the hundreds of projects that have revved up again in recent days. Home buyers respond to his posts with more questions as they try to figure out if their apartments are likely to be completed.

One home buyer asked about the on-and-off construction progress for one of Evergrande’s residential projects in the province of Shandong.

“Brother, there is no money in the supervised account,” Mr. Li replied, referring to the escrow account where Evergrande was supposed to place the money it received upfront from the sale of the apartments. He did not explain how he knew this, or respond to a request for comment. But in some government complaint forums online, local officials have told home buyers that money in developers’ escrow accounts is missing.

Zhang Yao, a yoga instructor who taught at Evergrande Healthy Land, a health and wellness park in the central province of Henan, said she was asked to resign in September but is still owed $750. Ms. Zhang, 29, said she had been paid through an employment agency but had recently confronted an Evergrande manager, who was unable to give her a date for when the company would pay her.

She said the manager told her that Evergrande’s own employees had not been paid since October. A representative for the company did not respond to a request for comment.

In September, Evergrande employees joined worried home buyers in protesting outside company offices around China. Some were later detained or visited by the local police. As many as 80 percent of Evergrande employees were at one point asked to put up money to help fund the company’s operations.

Mr. Cao, an Evergrande home buyer who requested The New York Times use only his surname for fear of being visited by the police, said he had put a down payment on a $160,000 apartment in Jiangxi Province that was nearly completed and was supposed to be delivered in January. He doesn’t expect the apartment will be done in time because there are only around 20 workers each day on the construction site, he said.

Understand the Evergrande Crisis

Card 1 of 6

What is Evergrande? The Evergrande Group, a sprawling Chinese real estate giant, has the distinction of being the world’s most debt-saddled developer. It was founded in 1996 and rode China’s real estate boom that urbanized large swathes of the country, and has millions of apartments in hundreds of cities.

How much does it owe? Evergrande has more than $300 billion in financial obligations, hundreds of unfinished residential buildings and angry suppliers who have shut down construction sites. Things got so bad that the company paid its overdue bills with unfinished properties and asked employees to lend it money.

How did the company get into financial trouble? For decades, China’s real estate market operated unrestrained. But recently, Beijing started taking measures, including new restrictions on home sales, to tame the sector. Evergrande borrowed heavily as it grew and expanded into new businesses, and eventually ended up with more debt than it could pay off.

How has the Chinese government addressed the crisis? Beijing sat on the sidelines for months as Evergrande neared financial collapse. It wasn’t until December that the company said officials from state-backed institutions had joined a risk committee to help restructure the business.

Where do things stand with Evergrande now? For months, the real estate giant averted default by making 11th-hour payments on its bonds. But on Dec. 9, a major credit ratings firm declared Evergrande in default after it failed to meet a payment deadline. What is next for the company, bankruptcy, a fire sale or business as usual, has yet to be determined.

“I think the contractors still haven’t been fully paid,” he said. “If they had the money, they should have worked faster for sure.”

Amid the uncertainty, Evergrande’s colorful founder, once known for wearing a flashy gold-buckled Hermès belt, has been largely absent from public view. In early September, he posed behind top executives signing a “military order” pledging to deliver homes. (Over the following months, Evergrande would finish less than 10,000 units.) In a memo leaked later that month, he promised employees they would soon “walk out of the darkness.”

Last week, Evergrande published new photographs of Mr. Xu presiding over a meeting during which he called on executives to keep delivering homes. Then came dozens of photos of suddenly completed apartment projects. Home buyers were photographed happily signing documents that would allow them to finally take possession of their long-awaited apartments.

Some online commentators expressed disbelief that Evergrande could suddenly go from the brink of collapse to business as usual, or bristled at the idea that buyers should celebrate receiving the homes for which they had already paid.

“Today people become so grateful and feel they owe the developer a big favor,” remarked Michael Yu, a popular influencer on Douyin, the Chinese version of TikTok. “What happened to people’s bottom line these days?”

With Evergrande under the guidance of government officials, some home buyers and investors are likely to feel more hopeful. This week, the company delivered 1,419 apartments at its World City development as part of its push to finish 39,000 homes by the end of the year. But Evergrande is still on the hook for an estimated 1 million more.

The China Evergrande Centre building sign is seen in Hong Kong, China December 7, 2021. REUTERS/Tyrone Siu/File Photo

Register now for FREE unlimited access to Reuters.com

Register

HONG KONG, Dec 30 (Reuters) – Shares of China Evergrande Group (3333.HK) tumbled on Thursday after the embattled real estate developer did not pay offshore coupons due earlier this week.

Evergrande, whose $19 billion in international bonds are in cross-default after missing a deadline to pay coupons earlier this month, had new coupon payments worth $255 million due on Tuesday for its June 2023 and 2025 notes. ,

At least some investors holding the two bonds have not yet received the coupons, according to three sources with knowledge of the matter. Both the payments have a 30-day grace period.

Register now for FREE unlimited access to Reuters.com

Register

Evergrande’s shares ended down 9.1% on Thursday, while the benchmark Hang Seng index (.HSI) edged up 0.1%.

Bloomberg News reported earlier that the due date passed with no sign of payment by the property developer.

Evergrande’s Thursday decline wiped out gains from earlier this week, when the market cheered the initial progress made by the firm in resuming construction work.

Company Chairman Hui Ka Yan vowed in a meeting on Sunday to deliver 39,000 units of properties in December, compared with fewer than 10,000 in each of the previous three months. read more

“(The non-payments) show Evergrande is still not doing okay even though it is delivering homes,” said Thomas Kwok, head of equity business of CHIEF Securities in Hong Kong.

The market confidence in Evergrande and the China property sector is weak, as there could be more defaults with many bonds due in January, Kwok added.

Evergrande has more than $300 billion in liabilities and is scrambling to raise cash by selling assets and shares to repay suppliers and creditors.

The fate of Evergrande and other indebted Chinese property companies has gripped financial markets in recent months amid fears of knock-on effects, with Beijing repeatedly seeking to reassure investors.

Register now for FREE unlimited access to Reuters.com

Register

Editing by Richard Pullin, Stephen Coates, Shounak Dasgupta and Neil Fullick

Our Standards: The Thomson Reuters Trust Principles.