Central bank under pressure to respond to surge in prices

Fed chief to speak at 2:30 p.m. EST (1930 GMT)

WASHINGTON, Dec 15 (Reuters) – The Federal Reserve, signaling its inflation target has been met, on Wednesday said it would end its pandemic-era bond purchases in March, paving the way for three quarter-percentage-point interest rate increases by the end of 2022 as it exits from policies enacted at the start of the health crisis.

In new economic projections released following the end of a two-day policy meeting, officials forecast that inflation would run at 2.6% next year, compared to the 2.2% projected as of September, and the unemployment rate would fall to 3.5%.

As a result, officials at the median projected the Fed’s benchmark overnight interest rate would need to rise from its current near-zero level to 0.90% by the end of 2022, with continued increases in 2023 to 1.6% and in 2024 to 2.1% required to pull inflation back to the central bank’s 2% target.

Register now for FREE unlimited access to reuters.com

Register

Eventual rate hikes, the Fed said, would now hinge solely on the path of the job market.

“With inflation having exceeded 2 percent for some time, the Committee expects it will be appropriate to maintain” the current near-zero interest rates until labor markets have returned to full employment, the Fed said in a statement that began to pin down more thoroughly the central bank’s “normalization” of monetary policy following nearly two years of extraordinary efforts to nurse the economy through the fallout of the pandemic.

That is still underway, with the new Omicron coronavirus variant adding to uncertainty about the course of the economy.

But the Fed, at this point, said economic growth is expected to be 4.0% next year, an increase over the 3.8% projected in September.

Fed Chair Jerome Powell is scheduled to hold a news conference at 2:30 p.m. EST (1930 GMT) to elaborate on the new policy statement and answer questions about the central bank’s economic outlook.

Register now for FREE unlimited access to reuters.com

Register

Reporting by Howard Schneider

Editing by Paul Simao

Our Standards: The Thomson Reuters Trust Principles.

TOKYO, Dec 15 (Reuters) – The Japanese government overstated construction orders data received from builders for years, Prime Minister Fumio Kishida said on Wednesday, an admission that could dent credibility of official statistics widely used by investors and economists.

It was not clear why the government started the practice of rewriting the data. It is also unclear how gross domestic product (GDP) figures may have been affected, though analysts expected any impact to be minimal, particularly as the builders involved were likely to be smaller firms.

“It is regrettable that such a thing has happened,” Kishida said. “The government will examine as soon as possible what steps it can take to avoid such an incident from happening again.”

Register now for FREE unlimited access to reuters.com

Register

He made the comment in a parliamentary session after the Asahi newspaper reported the Ministry of Land, Infrastructure, Transport and Tourism had been “rewriting” data received from about 12,000 select companies since 2013 at a pace of about 10,000 entries per year.

Kishida said “improvements” had been made to the figures since January 2020 and that there was no direct impact on GDP data for fiscal year 2020 and 2021.

While the impact on past GDP numbers may be small, the revelation is likely to raise questions about the reliability of data that is a cornerstone for economists and investors looking to understand and forecast trends in the world’s third-largest economy.

It is also not the first time that issues have been raised about government data, including a flaw in health ministry data in 2018.

“The biggest problem is not the effect on the GDP per se but the damage to reliability of (official) statistics,” said Saisuke Sakai, senior economist at Mizuho Research and Technologies.

“We can’t help doubting this kind of issue could happen across government ministries,” Sakai said.

SLOPPY

The survey compiles public and private construction orders which in the 2020 fiscal year totalled roughly 80 trillion yen ($700 billion), and is among data used to calculate GDP.

For the survey, the ministry collects monthly orders data from construction companies through local prefecture authorities.

Companies that were late in submitting data would often send in several months’ worth of figures at once, the Asahi said. In these instances, the ministry would instruct local authorities to rewrite the orders for the combined months as the figure for the latest, single month.

“Overall GDP data is unlikely to change much,” said Akiyoshi Takumori, chief economist at Sumitomo Mitsui DS Asset Management.

Considering Japan has hundreds of thousands of construction companies, the ratio of those concerned is very small, he said.

“How much influence do they have? The kind of sloppy company – which puts out numbers late – is probably not a big one.”

Land Minister Tetsuo Saito, a member of the Komeito party – the junior partner of the ruling coalition – confirmed the practice in parliament, calling it “extremely regrettable”.

Asked about the issue, the government’s top spokesperson said only that the land ministry had been instructed to analyse “as soon as possible” what led to the practice.

“We will first wait for the results of that investigation,” Chief Cabinet Secretary Hirokazu Matsuno told a news conference when asked whether past GDP figures, the government’s monthly economic report or other data may need to be revised.

The rewriting of the data, which may be in breach of law, continued until this March, the Asahi said.

($1 = 113.7100 yen)

Register now for FREE unlimited access to reuters.com

Register

Reporting by Tetsushi Kajimoto, Kantaro Komiya, Leika Kihara and Chang-Ran Kim; Editing by Christopher Cushing and David Dolan

Our Standards: The Thomson Reuters Trust Principles.

RIYADH, Dec 12 (Reuters) – Saudi Arabia said on Sunday it expected to post its first budget surplus in nearly a decade next year, as it plans to restrict public spending despite a surge in oil prices that helped to refill state coffers hammered by the pandemic.

After an expected fiscal deficit of 2.7% of gross domestic product this year, Riyadh estimates it will achieve a surplus of 90 billion riyals ($23.99 billion), or 2.5% of GDP, next year – its first surplus since it went into a deficit after oil prices crashed in 2014.

“The surpluses will be used to increase government reserves, to meet the coronavirus pandemic needs, strengthen the kingdom’s financial position, and raise its capabilities to face global shocks and crises,” Crown Prince Mohammed bin Salman was quoted as saying by Saudi state press agency SPA.

Register now for FREE unlimited access to reuters.com

Register

The world’s biggest oil exporter plans to spend 955 billion riyals next year, a nearly 6% expenditure cut year on year, according to a budget document.

Riyadh plans to reduce military spending next year by around 10% from its 2021 estimates, the budget showed, a sign that the cost of the military conflict in neighbouring Yemen has started to ease.

Revenues jumped this year by almost 10% to 930 billion riyals from the budgeted 849 billion, driven by higher crude prices and oil production hikes as global energy demand recovered.

Next year, the kingdom expects revenues of 1.045 trillion riyals.

“We are totally now decoupling the government expenditure from the revenue”, Finance Minister Mohammed al-Jadaan told Reuters.

“We are telling our people and the private sector or economy at large that you can plan with predictability. Budget ceilings are going to continue in a stable way regardless of how the oil price or revenues are going to happen”.

‘INVESTMENT BURDEN’

Saudi Minister of Finance Mohammed al-Jadaan gestures during an interview with Reuters at the Ministry of Finance in Riyadh, Saudi Arabia, December 12, 2021. Picture taken December 12, 2021. REUTERS/Ahmed Yosri

Read More

The largest Arab economy shrank last year as the coronavirus crisis hurt its burgeoning non-oil economic sectors, while record-low oil prices weighed on its finances, widening the 2020 budget deficit to 11.2% of GDP.

But the economy bounced back this year as COVID-19 restrictions were eased globally and domestically.

Saudi Arabia forecast 2.9% GDP growth this year followed by 7.4% growth in 2022, according to the budget.

The kingdom does not disclose the oil price it assumes to calculate its budget.

Monica Malik, chief economist at Abu Dhabi Commercial Bank, had estimated it was likely basing its budget on an oil price assumption that could be as low as $50-$55 per barrel, based on previous official revenue forecasts.

“There was a 15.7% increase in government revenue for 2022 vs the pre-budget. I think the assumption is now for a price of over $70 per barrel with the sharp increase in oil price”, she said.

Saudi Arabia’s ability to maintain fiscal diligence depends partly on the increasing roles of entities like the Public Investment Fund (PIF) or the National Development Fund in backing Prince Mohammed’s ambitious investment plans.

Saudi Arabia plans more than $3 trillion in investment in the domestic economy by 2030, a target that economists have said will be tough to meet. read more

“The budget’s expected surplus in 2022 comes not only on the back of higher oil prices and production, but also on the back of scaling back COVID-related spending as well as continuing with transferring the investment burden to the state funds led by PIF”, said Mohamed Abu Basha, head of macroeconomic analysis at EFG Hermes.

($1 = 3.7513 riyals)

Register now for FREE unlimited access to reuters.com

Register

Reporting by Yousef Saba, Aziz El Yaakoubi, Davide Barbuscia and Saeed Azhar; Writing by Davide Barbuscia; Editing by William Maclean, Barbara Lewis and Peter Cooney

Our Standards: The Thomson Reuters Trust Principles.

Food, gasoline and rents lead broad increase in prices

CPI jumps 6.8% on year-on-year basis

Core CPI rises 0.5%; surges 4.9% on year-on-year basis

WASHINGTON, Dec 10 (Reuters) – U.S. consumer prices rose further in November amid strong gains in the cost of food and a range of other goods, leading to the largest annual increase in more than 39 years and potentially giving the Federal Reserve ammunition to quickly wind down its bond purchases.

The report from the Labor Department on Friday followed on the heels of a slew of data this month showing a rapidly tightening labor market. With supply bottlenecks showing little sign of easing and companies raising wages as they compete for scarce workers, high inflation could persist well into 2022.

The increased cost of living, the result of shortages caused by the relentless COVID-19 pandemic, is hurting President Joe Biden’s approval rating. High inflation and a strengthening economy have raised the risk of an early Fed interest rate increase.

Register now for FREE unlimited access to reuters.com

Register

“The biggest problem for the Fed is the mounting evidence of a strong pick-up in cyclical price pressures,” said Paul Ashworth, chief economist at Capital Economics in Toronto.

“Although we think headline inflation has now peaked, it will decline only gradually over the first half of next year and, crucially, because of that building cyclical pressure we expect core inflation to remain above the Fed’s target for a prolonged period.”

The consumer price index rose 0.8% last month after surging 0.9% in October. The broad-based increase was led by gasoline prices, which rose 6.1%, matching October’s gain. With crude oil prices declining recently, gasoline prices have likely peaked.

Food prices rose 0.7%. The cost of food at home increased 0.8%, driven by increases in the price of fruits and vegetables, meat and cereals and bakery products. It also cost more to eat away from home.

In the 12 months through November, the CPI accelerated 6.8%. That was the biggest year-on-year rise since June 1982 and followed a 6.2% advance in October.

Economists polled by Reuters had forecast that the CPI would climb 0.7% and increase 6.8% on a year-on-year basis.

TIGHTENING LABOR MARKET

Shoppers browse in a supermarket while wearing masks to help slow the spread of coronavirus disease (COVID-19) in north St. Louis, Missouri, U.S. April 4, 2020. REUTERS/Lawrence Bryant/File Photo

The government reported last week that the unemployment rate fell to a 21-month low of 4.2% in November. Tightening labor market conditions were underscored by a report on Thursday showing new applications for unemployment benefits dropped to the lowest level in more than 52 years last week.

Other data this week showed there were 11 million job openings at the end of October and Americans quit jobs at near-record rates.

“With supply shortages likely to stick around until next year and service-sector prices trending higher, inflation is going to get worse before it gets better,” said Sam Bullard, a senior economist at Wells Fargo in Charlotte, North Carolina.

Fed Chair Jerome Powell has said the U.S. central bank should consider speeding up the winding down of its monthly bond purchases at its policy meeting next week. Many economists are expecting an early Fed interest rate increase.

Excluding the volatile food and energy components, the CPI rose 0.5% last month after gaining 0.6% in October. The so-called core CPI was supported by rents, with owners’ equivalent rent of primary residence, which is what a homeowner would receive from renting a home, rising a solid 0.4%.

Prices for used cars and trucks increased 2.5% for a second straight month. New motor vehicle prices rose 1.1%, marking the eighth consecutive month of gains. A global semiconductor shortage has undercut motor vehicle production.

Airline fares rebounded 4.7%. But further increases are unlikely following the emergence of the Omicron variant of COVID-19, which could make some people hesitant to travel by air. The United States is already experiencing a resurgence in coronavirus infections, driven by the Delta variant.

The so-called core CPI jumped 4.9% on a year-on-year basis, the largest rise since June 1991, after increasing 4.6% in the 12 months through October.

The Fed tracks the personal consumption expenditures (PCE) price index, excluding the volatile food and energy components, for its flexible 2% inflation target. The core PCE price index surged 4.1% in the 12 months through October, the most since January 1991. Data for November will be released later this month.

“A continued trend higher in core inflation creates further hawkish risks for a Fed that has recently become more focused on the inflation side of its mandate, and suggests a rising likelihood of an even earlier first rate hike,” said Veronica Clark, an economist at Citigroup in New York.

Register now for FREE unlimited access to reuters.com

Register

Reporting by Lucia Mutikani

Editing by Chizu Nomiyama and Paul Simao

Our Standards: The Thomson Reuters Trust Principles.

A restaurant advertising jobs looks to attract workers in Oceanside, California, U.S., May 10, 2021. REUTERS/Mike Blake/File Photo

Register now for FREE unlimited access to reuters.com

Register

Job openings increase 431,000 to 11 million in October

Hiring falls 82,000; quits decline 205,000

WASHINGTON, Dec 8 (Reuters) – U.S. job openings surged in October while hiring decreased, suggesting a worsening worker shortage, which could hamper employment growth and the overall economy.

The Labor Department’s monthly Job Openings and Labor Turnover Survey, or JOLTS report, on Wednesday also showed a steady decline in layoffs, another sign that the jobs market was tightening. While the number of people voluntarily quitting their jobs fell, it remained quite high.

“Under normal circumstances, a near record number of job openings would be something worth celebrating,” said Jennifer Lee, a senior economist at BMO Capital Markets in Toronto. “But no employer is in a celebratory mood. It is difficult to fill orders or meet customer demands if there are not enough people to do the actual work.”

Register now for FREE unlimited access to reuters.com

Register

Job openings, a measure of labor demand, increased by 431,000 to 11.0 million on the last day of October. This was the second-highest on record. Economists polled by Reuters had forecast 10.4 million vacancies.

The surge was led by the accommodation and food services industry, where vacancies increased by 254,000 jobs. There were 45,000 job openings in the nondurable goods manufacturing industry, while vacancies increased by 42,000 in the educational services sector. But job openings decreased by 115,000 in state and local government, excluding education.

Regionally, the rise in job openings was more pronounced in the South, with moderate gains in the West and Midwest. Vacancies fell in the Northeast. The job openings rate rose to 6.9% from 6.7% in September.

Hiring dropped by 82,000 jobs to 6.5 million in October. The finance and insurance industry accounted for the decline, with a 96,000 drop in payrolls. There were, however, increases in hiring in educational services as well as state and local government education. The hiring rate was unchanged at 4.4%.

There were about 1.5 job openings per unemployed worker in October.

Reuters Graphics

The government reported last Friday that nonfarm payrolls increased by 210,000 jobs in November, the fewest since last December, after rising 546,000 in October. The unemployment rate fell to a 21-month low of 4.2%. read more

Though employment is 3.9 million jobs below the peak in February 2020, economists believe that number probably is not a true reflection of the labor market’s health as the shortfall includes people who have retired.

The JOLTS report showed layoffs fell by 35,000 to 1.361 million. The layoffs rate was unchanged at 0.9% for a third straight month.

Quits decreased by 205,000 to a still-high 4 million in October. The decline was in several industries, with large drops in transportation, warehousing and utilities as well as finance and insurance, and arts, entertainment and recreation.

But 21,000 more people quit their jobs in state and local government, excluding education. There were also more quits in mining and logging. The quits rate fell to 2.8% from 3.0% in September amid a large drop in the leisure and hospitality sector.

Reuters Graphics

“The quits rate in those industries dropped by half a percentage point, signaling some easing in job hopping,” said Nick Bunker, director of research at Indeed Hiring Lab. “In addition to the slowdown in wage growth in the sector seen in recent jobs reports, this trend suggests maybe the advantageous situation for workers in this sector might deteriorate in the months ahead if the current situation continues.”

The quits rate is normally viewed by policymakers and economists as a measure of job market confidence. The still-high quits rate suggests wage inflation will likely remain uncomfortably high for a while. Inflation is way above the Federal Reserve’s flexible 2% target.

Register now for FREE unlimited access to reuters.com

Register

Reporting by Lucia Mutikani; Editing by Andrea Ricci

Our Standards: The Thomson Reuters Trust Principles.

Nov 24 (Reuters) – A growing number of Federal Reserve policymakers indicated they would be open to speeding up the elimination of their bond-buying program if high inflation held and move more quickly to raise interest rates, minutes of the U.S. central bank’s last policy meeting showed.

The readout released on Wednesday was the latest indication that anxiety about rising inflation at the Fed has now taken root, with many officials at the Nov. 2-3 meeting also suggesting elevated price pressures could prove more persistent.

The durability and broadening in price pressures has taken the White House and the central bank by surprise and prompted both to respond. U.S. President Joe Biden and Fed Chair Jerome Powell stressed earlier this week that they would take steps to tackle the rising costs of everyday items, including food, gasoline and rent.

Register now for FREE unlimited access to reuters.com

Register

Although the surge in inflation in late spring and over the summer was portrayed as transitory, concern within the Fed has mounted as readings have continued to remain elevated into the fall.

“Various participants noted that the (policy-setting) Committee should be prepared to adjust the pace of asset purchases and raise the target range for the federal funds rate sooner than participants currently anticipated if inflation continued to run higher than levels consistent with the Committee’s objectives,” the Fed said in the minutes.

Fed policymakers unanimously decided at last month’s meeting to begin reducing the central bank’s $120 billion in monthly purchases of Treasuries and mortgage-backed securities, a program introduced in early 2020 to help nurse the economy through the COVID-19 pandemic. A number outright favored a faster taper of the bond-buying program during those deliberations, the minutes showed.

The original pace would see the asset purchases tapered completely by next June. Since then, however, there have been increasing calls by some policymakers to accelerate the timeline in the face of the continued high inflation readings and stronger job gains, in order to give the Fed greater flexibility to raise its benchmark overnight interest rate from the current near-zero level earlier next year if needed.

Investors’ reaction to the release of the minutes was largely muted, with the S&P 500 index (.SPX) up about 0.2% in late afternoon trading. Yields on the shorter-dated Treasuries most sensitive to Fed policy expectations held steady at slightly higher levels, while the dollar remained near its highest mark since July 2020 against a basket of major trading partners’ currencies.

“The (policy committee) has clearly woken up to the realisation that, even if it falls back somewhat, inflation is likely to remain above target for some considerable time,” said Paul Ashworth, chief U.S. economist at Capital Economics.

‘WOULD NOT HESITATE’

A number of other policymakers at the Fed’s November meeting, however, still advocated for a more patient approach, wanting more data in hand, although all agreed the Fed “would not hesitate to take appropriate actions to address inflation pressures that posed risks to its longer-run price stability and employment objectives.”

But with further robust economic data released over the past three weeks, all signs point to an acceleration of the bond-buying taper now being firmly on the table at the Fed’s next policy meeting on Dec. 14-15.

Data released on Wednesday showed the number of Americans filing new claims for unemployment benefits fell to the lowest level since 1969 last week, while the Fed’s preferred measure of inflation continued to run at more than twice the central bank’s 2% flexible average goal in October.

San Francisco Fed President Mary Daly, one of the central bank’s most cautious policymakers, also said on Wednesday she is open to a quicker wind-down of the bond-buying program if jobs and inflation data remain steady and that she could see the Fed’s policy-setting committee raising rates once or twice next year.

Investors currently see a 53% probability that the Fed’s overnight lending rate will rise in May of 2022, up from 45% on Tuesday, according to CME Group’s FedWatch program.

Inflation in October rose at its fastest annual pace in 31 years, testing the Fed’s working assumption for most of the year that the pandemic-induced burst would be temporary as supply bottlenecks eased and demand rotated from goods to services.

Some other policymakers have said recently they too are now more comfortable with an interest rate hike earlier next year than previously anticipated, noting that the current pace of job gains would put the Fed on track to be near or at its maximum employment goal by the middle of 2022.

Register now for FREE unlimited access to reuters.com

Register

Reporting by Lindsay Dunsmuir; Editing by Paul Simao

Our Standards: The Thomson Reuters Trust Principles.

OPEC+ has rebuffed repeated U.S. calls for more crude

Biden under political pressure as inflation picks up

OPEC+ meets on Dec. 2 but no sign of a change of tack

India, Britain detail contributions to oil release

WASHINGTON, Nov 23 (Reuters) – The administration of U.S. President Joe Biden announced on Tuesday it will release millions of barrels of oil from strategic reserves in coordination with China, India, South Korea, Japan and Britain, to try to cool prices after OPEC+ producers repeatedly ignored calls for more crude.

Biden, facing low approval ratings amid rising inflation ahead of next year’s congressional elections, has grown frustrated at repeatedly asking the Organization of the Petroleum Exporting Countries and its allies, known as OPEC+, to pump more oil without any response.

“I told you before that we’re going to take action on these problems. That’s exactly what we’re doing,” Biden said in remarks broadcast from the White House.

Register now for FREE unlimited access to reuters.com

Register

“It will take time, but before long you should see the price of gas drop where you fill up your tank, and in the longer-term we will reduce our reliance on oil as we shift to clean energy,” he said.

Crude oil prices recently touched seven-year highs, and consumers are feeling the pain of the increase in fuel costs. Retail gasoline prices are up more than 60% in the last year, the fastest rate of increase since 2000, largely because people have returned to the roads as pandemic-induced restrictions have eased and demand has rebounded.

Under the plan, the United States will release 50 million barrels, the equivalent of about two and a half days of U.S. demand. India, meanwhile, said it would release 5 million barrels, while Britain said it would allow the voluntary release of 1.5 million barrels of oil from privately held reserves.

Japan will hold auctions for about 4.2 million barrels of oil, about 1 or 2 days worth of its demand, out of its national stockpile by the end of the year, the Nikkei newspaper reported on Wednesday.

Details on the amount and timing of the release of oil from South Korea and China were not announced. Seoul said it would decide after discussions with the United States and other allies.

The price of oil rebounded on Tuesday, after falling for several days as rumors of the plans made their way into the market. Some analysts also attributed the market’s rebound to the lack of firm details out of China, though Reuters reported last week that the country has been working on such a release. Brent crude futures rose 3.3% on Tuesday to $82.31 a barrel.

It was the first time that the United States had coordinated such a move with some of the world’s largest Asian oil consumers, officials said.

OPEC+, which includes Saudi Arabia and other U.S. allies in the Gulf, as well as Russia, has rebuffed requests to pump more at its monthly meetings. It meets again on Dec. 2 to discuss policy but has so far shown no indication it will change tack.

The group has been struggling to meet existing targets under its agreement to gradually increase production by 400,000 barrels per day (bpd) each month – a pace Washington sees as too slow – and it remains worried that a resurgence of coronavirus cases could again drive down demand.

A maze of crude oil pipes and valves is pictured during a tour by the Department of Energy at the Strategic Petroleum Reserve in Freeport, Texas, U.S. June 9, 2016. REUTERS/Richard Carson/File Photo

Read More

Recent high oil prices have been caused by a sharp rebound in global demand, which cratered early in the pandemic in 2021, and analysts have said that releasing reserves may not be enough to curb further rises.

“It’s not large enough to bring down prices in a meaningful way and may even backfire if it prompts OPEC+ to slow the pace at which it is raising output,” said Caroline Bain, chief commodities economist at Capital Economics Ltd.

The administration has also pointed to a notable gap between the price of unfinished gasoline futures and the retail cost of gasoline, which has widened to about $1.14 a gallon from roughly 78 cents in mid-October. The White House urged the Federal Trade Commission to investigate the issue last week.

Biden’s political opponents, meanwhile, seized on the announcement to criticize his administration’s efforts to decarbonize the U.S. economy and discourage new fossil fuel development on federal lands.

“Tapping the Strategic Petroleum Reserve will not fix the problem. We are experiencing higher prices because the administration and Democrats in Congress are waging a war on American energy,” said Senator John Barrasso, the ranking Republican on the Senate energy committee.

The release from the U.S. Strategic Petroleum Reserve would be a combination of a loan and a sale to companies, U.S. officials said. The 32 million-barrel loan will take place over the next several months, while the administration would accelerate a sale of 18 million barrels already approved by Congress to raise funds for the budget.

WARNING TO OPEC

The effort by Washington to team up with major Asian economies to lower energy prices acts as a warning to OPEC and other big producers that they need to address concerns about high crude prices, up more than 50% so far this year.

“It sends a signal to OPEC+ that the consuming nations are not going to get pushed around any more by them,” said John Kilduff, partner at Again Capital LLC in New York. “OPEC+ has been stingy with their output for months now.”

Suhail Al-Mazrouei, energy minister of the United Arab Emirates, one of OPEC’s biggest producers, said before details of the release of U.S. reserves were announced that he saw “no logic” in lifting UAE supply for global markets.

An OPEC+ source said releasing reserves would complicate calculations for OPEC+, as it monitors the market on a monthly basis. However, they and several market analysts said the release was not as big as the headline figure suggested. They said Britain and India were releasing modest amounts and the United States had already announced some releases, and so the additional quantity was less than expected.

The United States historically has worked on coordinated stocks releases with the Paris-based International Energy Agency (IEA), a bloc of 30 industrialised energy consuming nations.

Japan and South Korea are IEA members. China and India are only associate members.

Register now for FREE unlimited access to reuters.com

Register

Reporting by Timothy Gardner in Washington

Additional reporting by Sonali Paul in Melbourne, Ghaida Ghantous in Dubai, Ahmad Ghaddar in London, OPEC team, Jarrett Renshaw in Philadelphia, Alexandra Alper and Jeff Mason in Washington, Jessica Resnick-Ault in New York and Aaron Sheldrick in Tokyo

Writing by Edmund Blair, Alexander Smith and Richard Valdmanis

Editing by David Gaffen, Carmel Crimmins, Cynthia Osterman and Matthew Lewis

Our Standards: The Thomson Reuters Trust Principles.

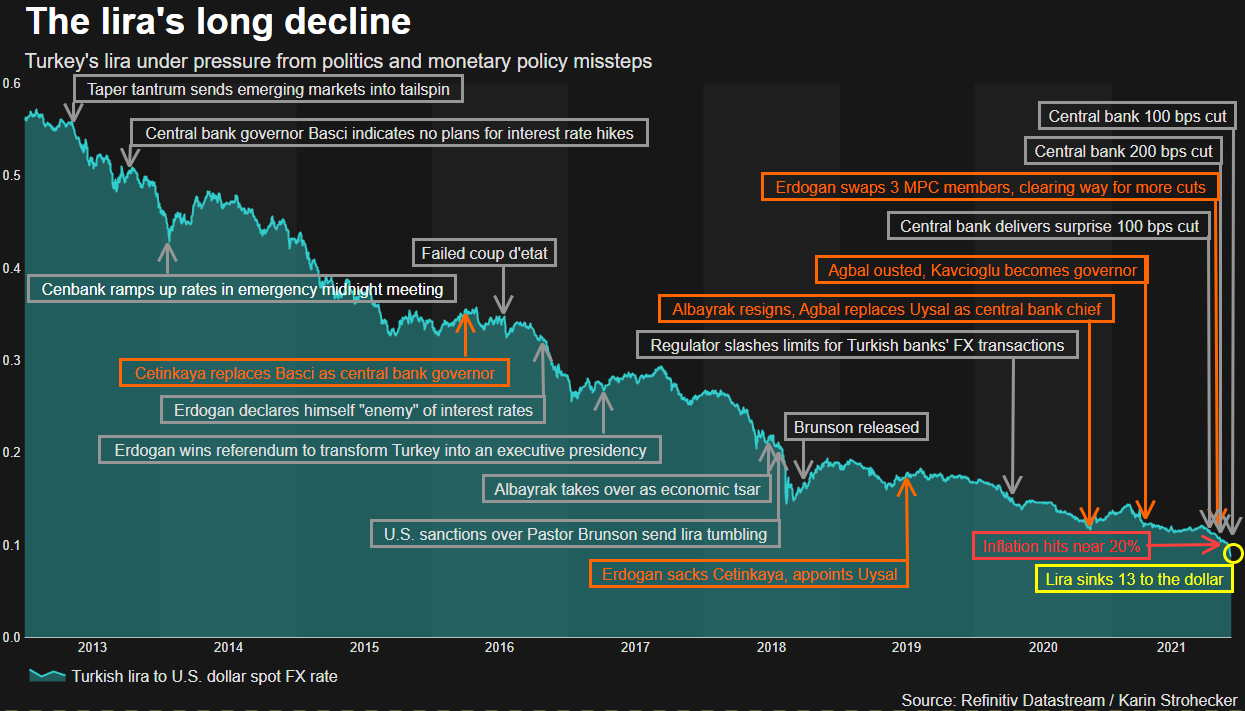

Lira has shed 45% vs dollar this year, worst in world

Central bank has slashed policy rate 400 points since Sept

Turks say household budgets, future plans in turmoil

Ex-central banker calls for end to ‘irrational experiment’

Erdogan insists tighter policy will not lower inflation

ISTANBUL, Nov 23 (Reuters) – Turkey’s lira nose-dived 15% on Tuesday in its second-worst day ever after President Tayyip Erdogan defended recent sharp rate cuts, and vowed to win his “economic war of independence” despite widespread criticism and pleas to reverse course.

The lira tumbled to as low as 13.45 to the dollar, plumbing record troughs for an 11th straight session, before paring some losses. It has shed 45% of its value this year, including a near 26% decline since the beginning of last week.

Erdogan has applied pressure on the central bank to pivot to an aggressive easing cycle that aims, he says, to boost exports, investment and jobs – even as inflation soars to near 20% and the currency depreciation accelerates, eating deeply into Turks’ earnings. read more

Register now for FREE unlimited access to reuters.com

Register

Many economists called the rate cuts reckless while opposition politicians appealed for early elections. Turks told Reuters the dizzying currency collapse was upending their household budgets and plans for the future.

While authorities have not intervened to stem the selloff, two sources said Erdogan met with central bank Governor Sahap Kavcioglu on Tuesday but gave no further details. The bank did not comment on the lira’s plunge.

Former central bank deputy governor Semih Tumen, who was dismissed last month in the latest of Erdogan’s rapid leadership overhaul, called for an immediate return to policies which protect the lira’s value.

“This irrational experiment which has no chance of success must be abandoned immediately and we must return to quality policies which protect the Turkish lira’s value and the prosperity of the Turkish people,” he said on Twitter.

Tuesday’s slide was the lira’s worst since the height of a currency crisis in 2018 that led to a sharp recession, and brought on three years of sub-par economic growth and double-digit inflation.

Though the lira recovered half its losses by 1413 GMT, at 12.485 to the dollar, the last 11 days has been its worst run since 1999. Over just three hours of volatile trading on Tuesday, its value bounced to 13 from 12 to the dollar.

The central bank has slashed rates by a total of 400 points since September, leaving real yields deeply negative as virtually all other central banks have begun tightening, or are preparing to do so.

Turkey rates and inflation

SLIDING POLLS

The lira has been by far the worst performer globally this year due mostly to what some analysts have called a premature economic “experiment” by the president who has ruled Turkey for nearly two decades.

Erdogan’s AK Party is sliding in opinion polls ahead of elections scheduled for no later than mid-2023, reflecting sharply higher costs of living.

“Prices are rising too fast. I don’t want to buy certain products because they’ve got too expensive,” said Kaan Acar, 28, a hotel executive in southern Turkey’s Kalkan resort, adding he was thinking of cancelling a trip abroad due to the rising cost.

“The fault lies with President Erdogan, the AKP government, and those who for years turned a blind eye and supported them.”

Investors appeared to flee as volatility gauges spiked to the highest levels since March, when Erdogan abruptly sacked the hawkish former central bank chief and installed Kavcioglu, who like the president is a critic of high rates.

Against the euro, the currency weakened to a fresh record low beyond 15 on Tuesday.

The 10-year benchmark bond yield rose above 21% for the first time since the start of 2019. Sovereign dollar bonds suffered sharp falls with many longer-dated issues down 2 cents, Tradeweb data showed.

As the lira plunged, Turkey’s main share index (.XU100) rose more than 1% due to suddenly cheap valuations. However bank stocks dropped, with the banking index down 2.5%.

Lira’s plunge over the years

EMERGENCY HIKES

The central bank cut its policy rate last Thursday by 100 basis points to 15%, well below inflation of nearly 20%, and signalled further easing.

Erdogan received support on Tuesday from his parliamentary ally, nationalist MHP leader Devlet Bahceli, who said high interest rates limit production and that there was no alternative to a policy focused on investments.

“Turkey needs to rid itself of the hunchback of interest rates,” Bahceli said in a speech to his party in parliament.

Erdogan defended the policy late on Monday and said high rates would not lower inflation, an unorthodox view he has repeated for years. read more

“I reject policies that will contract our country, weaken it, condemn our people to unemployment, hunger and poverty,” he said after a cabinet meeting, prompting a late-day slide in the lira.

Analysts said emergency rate hikes would be needed soon, while speculation about a cabinet overhaul involving the more orthodox finance minister, Lutfi Elvan, has also weighed.

Societe Generale predicted an “emergency” hike as soon as next month, with the policy rate rising to about 19% by the end of the first quarter of 2022.

Ilan Solot, global market strategist at Brown Brothers Harriman, said Erdogan would likely wait until a “breaking point” before reversing course.

“Right now locals seem content to keep their dollars in the local system. If they start to move money elsewhere, to Germany, to Austria, it’s another story,” Solot said.

“At that point we are talking capital controls. There are not enough dollar reserves, not enough dollars in the system to handle that. Then we will have a conversation about a real currency crisis,” he added.

Register now for FREE unlimited access to reuters.com

Register

Additional reporting by Ali Kucukgocmen in Istanbul, Ece Toksabay in Ankara and Karin Strohecker, Marc Jones and Tommy Wilkes in London; Writing by Jonathan Spicer; Editing by Gareth Jones and Susan Fenton

Our Standards: The Thomson Reuters Trust Principles.

WASHINGTON, Nov 22 (Reuters) – U.S. President Joe Biden on Monday nominated Federal Reserve Chair Jerome Powell for a second four-year term, positioning the former investment banker to continue the most consequential revamp of monetary policy since the 1970s and finish guiding the economy out of the pandemic crisis.

Lael Brainard, the Federal Reserve board member who was the other top candidate for the job, will be vice chair, the White House said.

Combined, the nominations pair two monetary policy veterans and collaborators on a recent overhaul of Fed policy, which shifted the emphasis to jobs from the preeminent focus on inflation established some four decades ago. Their challenge will be to keep U.S. job growth underway while also ensuring recent strong inflation doesn’t become entrenched.

Register now for FREE unlimited access to reuters.com

Register

“We’ve gone from an economy that was shut down to an economy that’s leading the world in economic growth,” Biden said in remarks at the White House with the nominees.

Citing Powell’s “steady leadership” that calmed panicked markets, and his belief in monetary policies that support maximum employment, Biden said “I believe Jay is the right person to see us through.”

The United States is still dealing with the impacts of the pandemic, including inflation, he said but the country has made “enormous progress” including adding nearly 6 million jobs since he was sworn in and increasing wages – positive signs that are a testament to the Federal Reserve.

“I respect Jay’s independence,” Biden said, directly addressing critics from his own Democratic party who wanted him to bump Powell, a Republican, for a Democrat. “At this moment of both enormous potential and enormous uncertainty for our economy, we need stability and independence at the Federal Reserve.”

Powell, 68, and Brainard, 59, will both need to be confirmed in their Fed leadership roles by the Senate, currently controlled by Biden’s Democratic party but closely divided. The president has for now left open several other Fed positions, including that of vice chair for supervision, that he may fill as soon as next month and that could be used to toughen bank regulation, improve diversity, and make other changes his supporters have urged for the Fed.

But for the Fed’s core monetary policy – managing inflation and setting interest rates as the economy reopens from the pandemic – Biden opted for continuity.

“They are veterans and mature public servants and there has been very little difference between them” on monetary policy said Adam Posen, president of the Peterson Institute for International Economics.

Together Powell, a moderate Republican elevated by former President Donald Trump, and Brainard, who served in prior Democratic administrations, “gives potentially non-partisan credibility to a more realistic assessment of inflation risks” the United States faces.

That reassessment could mean interest rate increases coming sooner than later if inflation, which both promised to fight, proves more persistent than expected.

“We know that high inflation takes a toll on families,” Powell said in brief remarks at the White House event where Biden announced the nominations.

Brainard also pledged to support a growing economy “that includes everyone,” and a Fed that “serves all Americans in every community.”

Federal Reserve Chair Jerome Powell listens as U.S. President Joe Biden nominates him for a second four-year term in the Eisenhower Executive Office Building’s South Court Auditorium at the White House in Washington, U.S., November 22, 2021. REUTERS/Kevin Lamarque

Read More

U.S. stocks hit record highs after the news. Treasury bond yields also rose and the dollar strengthened.

Powell’s reappointment had been encouraged by a cross-section of investors and economists with both conservative and liberal leanings, and was welcomed by Congress members of both parties.

The Fed’s aggressive actions at the start of the coronavirus pandemic in early 2020 were hailed as staving off a potential Depression. Later, some lauded his focus on jobs in the new policy framework launched just over a year ago, and others argued it would be too risky to oust the Fed chair during a sensitive transition from the emergency measures taken during the health crisis.

Reuters Graphics

CHANCE TO CEMENT A LEGACY

Powell’s second term would begin in early February, and the coming months will be crucial in determining whether his legacy will be as the Fed chair who elevated employment to the center of Fed policy, or as the one who let inflation surge and reestablish itself as a chronic problem.

Powell, who joined the Fed as a governor in 2012, did not anticipate being named chair when Trump was elected. With a pre-Fed career that had included eight years as a partner at The Carlyle Group, one of the world’s largest private equity firms, and no formal economics training, he had instead eyed the vice chair for supervision position eventually filled by Randal Quarles.

He was confirmed as Fed chair on an 84-13 vote, with Kamala Harris, now Biden’s vice president, among those opposing him.

He soon ran afoul of Trump, who hurled unprecedented public broadsides against Powell over Twitter and in frequent media appearances. At one point Trump labeled Powell an “enemy” of the United States for raising interest rates and explored whether he could fire him.

Powell not only survived but arguably grew in the job.

Initially hawkish as a governor, upon assuming the helm for U.S. monetary policy he considered himself a student at first, paying particular attention to arguments over whether the Fed’s focus on inflation had disadvantaged workers. The years since the 2007 to 2009 financial crisis had convinced many that was the case.

In November 2018, Powell launched a policy review that culminated in August 2020 with the adoption of an approach allowing economic expansions to run longer and “hotter,” with temporarily higher rates of inflation. Ideally that would lead to job gains that reach broadly into society and narrow the gaps in unemployment among different demographic groups.

It was an approach that conformed to what seemed then to be the changing nature of the U.S. economy, with embedded low inflation and low interest rates, and adapted as well to the demands of a pandemic crisis that threatened a permanent hole in the U.S. job market.

Just over a year into that new approach, however, inflation is running at levels not seen in decades as resurgent demand for goods and services outstrips the supply of materials and labor in an economy still shaking off the rust of pandemic shutdowns.

“The new leadership team faces some very tough calls in the period ahead,” wrote Evercore ISI vice chair Krishna Guha.

Register now for FREE unlimited access to reuters.com

Register

Reporting by Howard Schneider and Jeff Mason;

Editing by Dan Burns, Heather Timmons and Andrea Ricci

Our Standards: The Thomson Reuters Trust Principles.

A street sign for Wall Street is seen outside the New York Stock Exchange (NYSE) in Manhattan, New York City, U.S. December 28, 2016. REUTERS/Andrew Kelly

Register now for FREE unlimited access to reuters.com

Register

NEW YORK, Nov 19 (Reuters) – Some investors believe the stars are aligning for small-cap stocks, as the category stands to benefit from cheap valuations, robust economic growth and a relatively benign impact from looming tax policy changes.

About $2.4 billion has flowed into U.S. small-cap equity funds so far this month, already the biggest monthly inflow since March, according to data provider EPFR. That had helped fuel an 8% gain in the S&P 600 small-cap index (.SPCY) as of earlier this week since late October, doubling the large-cap S&P 500’s (.SPX) performance in that period. The Russell 2000 (.RUT), a broader small-cap index, gained about 7% over that time.

The small-cap indexes pared gains somewhat this week amid fears of a COVID-19 re-emergence.

Register now for FREE unlimited access to reuters.com

Register

Small caps, which have a median market capitalization of $1.2 billion in the Russell 2000, rallied in the early months of 2021 as investors bet that smaller firms would benefit more from a broad U.S. economic reopening. They floundered in subsequent months, when technology stocks took the market’s reins amid worries over whether the Delta variant of the coronavirus would stifle the economic rebound. The Russell 2000 is up 19% this year against a 25% rise for the S&P 500.

With a blistering S&P 500 rally stretching valuations on large-cap stocks and above-trend U.S. growth expected next year, some investors now believe small caps are a bargain.

The forward price-to-earnings ratio of the Russell 2000 compared to the large-cap Russell 1000 (.RUI) recently stood at 24% below its long-term average, while small caps also trade at historical discounts on other measures such as price-to-book and price-to-sales, according to BofA Global Research.

“Smaller-cap stocks on a relative basis just look much more attractive,” said Ryan Jacob, chief investment officer of Jacob Asset Management.

His firm’s growth stock funds “probably have our highest weightings ever” in small-cap shares compared to large, Jacob said.

RBC strategists said the U.S. economy is expected to expand 4% next year, compared with its long-term average of 2.5%, and believe small caps are a “pure play” on domestic growth. Analysts at BofA Global Research said the disparity in valuations between larger companies and smaller ones suggests high single-digit price returns annually for the Russell 2000 over the next decade compared with slightly negative annual returns for the S&P 500.

Chuck Carlson, chief executive officer at Horizon Investment Services in Hammond, Indiana, said his firm has added more small-cap exposure in the past four months, including shares of shipping company Matson (MATX.N) and semiconductor firm Onto Innovation (ONTO.N).

“After trading pretty much sideways for seven months, you had a pretty nice breakout,” Carlson said. “We like the fundamentals.”

The improving picture for smaller companies comes as a relief to investors looking for ways to diversify out of the megacap technology stocks that have led markets higher for most of the last decade, with the top five companies alone comprising more than 23% weight in the S&P 500.

“Now you don’t have to be in a FAANG stock to get some reasonable growth,” said Mike Petro, portfolio manager of the Putnam Small Cap Value Fund, using a common acronym for massive tech and growth stocks such as Apple (AAPL.O) and Amazon (AMZN.O). “You could be in some forgotten, little small-cap stock and get reasonable nominal growth on that.”

Jacob, of Jacob Asset Management, has pared back holdings in megacap stocks Alphabet (GOOGL.O) and Facebook parent Meta Platforms (FB.O), while favoring smaller companies such as OptimizeRx (OPRX.O) and Digital Turbine (APPS.O).

Some investors remain wary of small caps, which over the past decade have lagged overall, with the Russell 2000 rising 230% against a 285% gain for the S&P 500.

Signs that yet another wave of COVID-19 is taking a greater hold in the United States, as it has in some European countries, could once again push investors out of economically sensitive stocks and into technology companies, which are expected to better weather short-term growth fluctuations.

Strategists at the Wells Fargo Investment Institute this week urged investors to take profits on gains in “lower-quality” small-cap stocks and move into larger-capitalization companies, saying the economy is entering the middle phase of its expansion where growth historically has slowed.

Others, however, believe they could be a haven of sorts if tax policy changes backed by the Biden administration are put into law, in particular a minimum 15% tax on companies making over $1 billion.

Should that happen, “the impact on small-caps could be less than on large-caps,” said analysts at Ned Davis Research, which recently began favoring small-cap stocks.

Register now for FREE unlimited access to reuters.com

Register

Reporting by Lewis Krauskopf; Editing by Ira Iosebashvili and Jonathan Oatis

Our Standards: The Thomson Reuters Trust Principles.