NEW YORK, April 25 (Reuters) – Elon Musk clinched a deal to buy Twitter Inc (TWTR.N) for $44 billion cash on Monday in a transaction that will shift control of the social media platform populated by millions of users and global leaders to the world’s richest person.

It is a seminal moment for the 16-year-old company that emerged as one of the world’s most influential public squares and now faces a string of challenges.

Discussions over the deal, which last week appeared uncertain, accelerated over the weekend after Musk wooed Twitter shareholders with financing details of his offer.

Register now for FREE unlimited access to Reuters.com

Register

Under pressure, Twitter started negotiating with Musk to buy the company at the proposed $54.20 per share price. read more

“Free speech is the bedrock of a functioning democracy, and Twitter is the digital town square where matters vital to the future of humanity are debated,” Musk said in a statement.

Twitter’s shares were up about 6% following the news.

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Greg Roumeliotis in New York, additional reporting by Krystal Hu;

Editing by Mark Potter and Matthew Lewis

Our Standards: The Thomson Reuters Trust Principles.

NEW DELHI, March 15 (Reuters) – Amazon.com Inc has gone on the attack in its bitter dispute with two Indian retailers, accusing them of fraud in Indian newspaper ads on Tuesday after Reliance Industries (RELI.NS) suddenly took over many of Future Retail (FRTL.NS) stores.

Amazon has been contesting the planned $3.4 billion sale of Future Group’s retail assets to Reliance, first announced in 2020, and the case is currently before the Indian Supreme Court.

Reliance, India’s biggest conglomerate and retailer run by the country’s richest man, began taking over the prized real estate with utmost stealth on Feb.25 when its staff showed up at many of Future biggest stores to assume control, sources have told Reuters. read more

Register now for FREE unlimited access to Reuters.com

Register

In ads headlined “PUBLIC NOTICE” in leading Indian newspapers on Tuesday, Amazon said: “these actions have been done in a clandestine manner by playing a fraud on the constitutional courts in India.”

Future and Reliance did not immediately respond to a request for comment.

Amazon’s public outcry comes even though on March 3 it offered to hold talks. The ongoing talks have raised hopes the dispute could be resolved. read more

Future has said in filings this month that it could not pay rent at many outlets given its distressed financial situation and that Reliance, which had taken over many of its leases, had issued it with termination notices.

Amazon is concerned that Reliance is continuing to take over Future stores even as the talks continue, according to a source with direct knowledge of the matter who was not authorised to speak to media and declined to be identified.

The newspaper ads were aimed at alerting all stakeholders, including Future’s lenders, that the transfer of assets to Reliance is legally prohibited, the source added.

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Aditya Kalra and Abhirup Roy; Editing by Edwina Gibbs

Our Standards: The Thomson Reuters Trust Principles.

“We are shocked by the loss of life in Ukraine,” CEO says

LONDON, Feb 28 (Reuters) – Shell (SHEL.L) will exit all its Russian operations, including a major liquefied natural gas plant, it said on Monday, becoming the latest major Western energy company to quit the oil-rich country following Moscow’s invasion of Ukraine.

The decision comes a day after rival BP abandoned its stake in Russian oil giant Rosneft (ROSN.MM) in a move that could cost the British company over $25 billion. Norway’s Equinor (EQNR.OL) also plans to exit Russia. read more

Shell said in a statement it will quit the flagship Sakhalin 2 LNG plant in which it holds a 27.5% stake, and which is 50% owned and operated by Russian gas giant Gazprom .

Register now for FREE unlimited access to Reuters.com

Register

Shell said the decision to exit Russian joint ventures will lead to impairments. Shell had around $3 billion in non-current assets in these ventures in Russia at the end of 2021, it said.

“We are shocked by the loss of life in Ukraine, which we deplore, resulting from a senseless act of military aggression which threatens European security,” Shell Chief Executive Ben van Beurden said in a statement.

Rival BP’s Chief Executive Bernard Looney called an urgent meeting with his leadership team on Thursday, just hours after the first Russian bombs fell on Ukrainian capital Kyiv last week, two BP sources told Reuters.

During that previously unreported meeting, Looney made it clear the company’s investment in Rosneft had become untenable, the sources said.

“There was only one decision we could make,” one of the BP insiders said. “The exit was the only viable way.”

Looney held two more board meetings at the weekend, after which board members voted to immediately exit the Rosneft stake, the sources said.

Looney also spoke to British Business Secretary Kwasi Kwarteng on Friday, when Kwarteng expressed his concern about BP’s interests in Russia. Kwarteng welcomed BP’s decision to exit on Twitter on Sunday.

SHELL

Kwarteng had a similar message for Shell on Monday.

“Shell have made the right call to divest from Russia,” he said on Twitter, adding that he had spoken to van Beurden earlier on Monday.

The Sakhalin 2 project, located off Russia’s northeastern coast is huge, producing around 11.5 million tonnes of LNG per year, which is exported to major markets including China and Japan.

For Shell, the world’s largest LNG trader, leaving the project deals a blow to its plans to supply gas to fast-growing markets in the coming decades.

Shell said the Russia exit will not affect its plans to switch to low-carbon and renewables energy.

The company also plans to end its involvement in the Nord Stream 2 Baltic gas pipeline linking Russia to Germany, which it helped finance as a part of a consortium of companies. Germany last week halted the project. read more

Shell will also exit the Salym Petroleum Development, another joint venture with Gazprom.

Together, Salym and Sakhalin 2 contributed $700 million to Shell’s net earnings in 2021.

“Right decision by the Board of Shell to exit its Russian ventures,” Adam Matthews, chief responsible investment officer for the Church of England Pensions Board, which invests in Shell, said in a LinkedIn post.

“Following BP’s decision the focus is on those that have yet to take such a step,” Matthews said.

Norway’s Equinor, majority owned by the Norwegian state, said earlier on Monday that it would start divesting from its joint ventures in Russia. That came after the country’s sovereign wealth fund, the world’s largest, said on Sunday it would divest its Russian assets.

Other Western companies including global bank HSBC and the world’s biggest aircraft leasing firm AerCap said they plan to exit Russia as Western governments ratchet up economic sanctions on Moscow. read more

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Ron Bousso and Shanima A in Bengaluru; Editing by Jonathan Oatis, Simon Webb and Richard Pullin

Our Standards: The Thomson Reuters Trust Principles.

LONDON, Feb 11 (Reuters) – The platform which sold an NFT of Jack Dorsey’s first tweet for $2.9 million has halted most transactions because people were selling tokens of content that did not belong to them, its founder said, calling this a “fundamental problem” in the fast-growing digital assets market.

Sales of NFTs, or non-fungible tokens, soared to around $25 billion in 2021, leaving many baffled as to why so much money is being spent on items that do not physically exist and which anyone can view online for free.

NFTs are crypto assets that record the ownership of a digital file such as an image, video or text. Anyone can create, or “mint”, an NFT, and ownership of the token does not usually confer ownership of the underlying item. read more

Register now for FREE unlimited access to Reuters.com

Register

Reports of scams, counterfeits and “wash trading” have become commonplace.

The U.S.-based Cent executed one of the first known million-dollar NFT sales when it sold the former Twitter CEO’s tweet as an NFT last March. But as of Feb. 6, it has stopped allowing buying and selling, CEO and co-founder Cameron Hejazi told Reuters.

“There’s a spectrum of activity that is happening that basically shouldn’t be happening – like, legally” Hejazi said.

While the Cent marketplace “beta.cent.co” has paused NFT sales, the part specifically for selling NFTs of tweets, which is called “Valuables”, is still active.

Hejazi highlighted three main problems: people selling unauthorised copies of other NFTs, people making NFTs of content which does not belong to them, and people selling sets of NFTs which resemble a security.

He said these issues were “rampant”, with users “minting and minting and minting counterfeit digital assets”.

“It kept happening. We would ban offending accounts but it was like we’re playing a game of whack-a-mole… Every time we would ban one, another one would come up, or three more would come up.”

“MONEY CHASING MONEY”

Such problems may come into greater focus as major brands join the rush towards the so-called “metaverse”, or Web3. Coca-Cola (KO.N) and luxury brand Gucci are among companies to have sold NFTs, while YouTube said it will explore NFT features.

While Cent, with 150,000 users and revenue “in the millions”, is a relatively small NFT platform, Hejazi said the issue of fake and illegal content exists across the industry.

“I think this is a pretty fundamental problem with Web3,” he said.

The biggest NFT marketplace, OpenSea, valued at $13.3 billion after its latest round of venture funding, said last month more than 80% of the NFTs minted for free on its platform were “plagiarized works, fake collections and spam”.

OpenSea tried limiting the number of NFTs a user could mint for free, but then reversed this decision following a backlash from users, the company said in a Twitter thread, adding that it was “working through a number of solutions” to deter “bad actors” while supporting creators.

“It is against our policy to sell NFTs using plagiarized content,” an OpenSea spokesperson said.

“We are working around the clock to ship products, add features, and refine our processes to meet the moment.”

To many NFT-enthusiasts, the decentralised nature of blockchain technology is appealing, allowing users to create and trade digital assets without a central authority controlling the activity.

But Hejazi said his company was keen on protecting content-creators, and may introduce centralised controls as a short-term measure in order to re-open the marketplace, before exploring decentralised solutions.

It was after the Dorsey NFT sale that Cent started to get a sense of what was going on in NFT markets.

“We realized that a lot of it is just money chasing money.”

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Elizabeth Howcroft, Editing by Louise Heavens and Andrew Heavens

Our Standards: The Thomson Reuters Trust Principles.

People walks past a logo of SoftBank Corp on a street in Tokyo, Japan, August 6, 2015. REUTERS/Yuya Shino

Register now for FREE unlimited access to Reuters.com

Register

Son said he was surprised by registration -source

SoftBank stake in Alibaba worth about $82 billion

Shares in Alibaba and SoftBank jumped on Wednesday

Focus on potential asset sales after Arm deal collapse

Group’s LTV ratio is rising as value of assets fall

TOKYO, Feb 9 (Reuters) – Japan’s SoftBank Group Corp (9984.T) said on Wednesday there was no link between Alibaba registering a U.S. share facility and any specific plans to sell down its stake in the Chinese e-commerce giant.

SoftBank’s shares jumped almost 6% in Tokyo, while Alibaba’s Hong Kong-listed shares were up almost 7%.

“The registration of the ADR conversion facility, including its size, is not tied to any specific future transaction by SBG,” SoftBank said in a statement to Reuters.

Register now for FREE unlimited access to Reuters.com

Register

SoftBank has previously used its Alibaba shares as collateral for loans and trimmed its stake using derivatives to capture upside from any rise in the company’s stock price.

After Alibaba (9988.HK), last week filed to register an additional 1 billion American Depository Shares (ADS), Citigroup analysts had said this might “suggest potential selling intention by SoftBank”.

In a fresh research note on Wednesday, Citi said Alibaba might have registered in advance a large number of ADS to support future plans of shareholders to convert the company’s Hong Kong stocks to those listed in New York.

SoftBank Chief Executive Masayoshi Son told analysts he was “surprised” and had not requested the Alibaba filing, a person familiar with the matter said on condition of anonymity.

Despite its 25% stake in Alibaba being worth about $82 billion, SoftBank is valued at just $84 billion and there has been speculation that the Japanese firm may monetize more of the holding, which began with a $20 million investment in 2000.

Alibaba’s shares have fallen about 60% from highs in October 2020, amid a regulatory crackdown against tech firms in China.

SoftBank’s fund raising plans were dealt a major setbackthis week after it abandoned plans to sell chip designer Arm to Nvidia (NVDA.O). The group is still investing through its Vision Fund unit and buying back shares.

SoftBank’s shares are down by about half from highs in March last year. The group squeezed out a profit in the October-December quarter after an upswing in valuations in Vision Fund’s private assets offset falling shares in its listed portfolio.

The group’s loan-to-value ratio is being closely watched after it rose to 22% from 19% three months earlier as the net value of SoftBank’s assets fell and debt rose. Son has pledged to keep the ratio below 25% in normal times.

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Sam Nussey; Editing by Gerry Doyle and Alexander Smith

Our Standards: The Thomson Reuters Trust Principles.

Unilever signals it would pursue deal for GSK unit

Says committed to ‘strict financial discipline’

Jan 17 (Reuters) – Unilever (ULVR.L) signalled on Monday it would pursue a deal for GSK’s (GSK.L) consumer business, calling it a “strong strategic fit”, but Unilever shares slid more than 8%, highlighting investors’ doubts about its 50-billion-pound ($68.4 billion) offer.

GlaxoSmithKline confirmed over the weekend that it had rejected three bids from the Dove soap maker for the consumer healthcare business, which is home to brands such as Sensodyne toothpaste, Emergen-C vitamin supplement and Panadol painkiller.

GSK, led by Emma Walmsley, has hired Goldman Sachs (GS.N) and Citigroup (C.N) to review Unilever’s approach but it will not engage in talks unless Unilever bumps up its offer, sources familiar with the matter said.

Register now for FREE unlimited access to Reuters.com

Register

GSK’s shares jumped 6% to their highest level since May 2020. It said on Saturday Unilever’s proposal “fundamentally undervalued” the consumer business, adding that it would stick to its plan of listing the division this year.

“Initial feedback on the deal from investors over the weekend has been almost uniformly negative,” Jefferies analysts said in a note. Others noted Unilever’s share price fall indicated a lack of confidence in its management and concern over the price.

The Marmite spread maker, however, defended the bid for the GSK consumer business, in which U.S. drugs company Pfizer (PFE.N) owns a 32% stake.

“The acquisition would create scale and a growth platform for the combined portfolio in the U.S., China and India, with further opportunities in other emerging markets,” Unilever said, pointing to synergies in the oral care and vitamin supplements business.

GSK and Pfizer would open negotiations with Unilever’s boss Alan Jope if the consumer goods giant was ready to improve its bid to more than 60 billion pounds, a source familiar with Pfizer’s strategy said.

The source called the business a “legitimate standalone candidate”, adding its market value could rise to almost $100 billion once the business was spun out and listed.

“Right now there is more value in a spin-off but if Unilever is ready to go north of 60 billion pounds then a dialogue could start,” he said.

GSK declined to comment and Pfizer did not immediately respond to a request for comment on the fate of GSK’s consumer business.

EXECUTION

GSK laid out plans for a separate listing of the consumer arm in June last year, following pressure from investors to explore a shake-up of the company and focus on its pharmaceuticals business.

A Unilever buyout of the consumer division would be one of the largest ever on the London market, and one of the biggest deals globally since the start of the COVID-19 pandemic.

It would also boost Unilever’s growth strategy, as management has been under pressure to turn around the company’s languishing stock price and cope with high costs and slim margins, but raises questions about its strategy.

Some analysts expressed doubts over Unilever’s ability to sweeten its offer to GSK.

“Given vocal investor concern of late and Unilever’s share price reaction this morning, this could prevent a higher offer from materialising,” said Chris Beckett, head of equity research at Quilter Cheviot.

Reports of buying interest in GSK’s consumer arm, including from private equity players, have been doing the rounds for a while. read more

“It’s a little surprising that (GSK and Pfizer) haven’t ripped Unilever’s arm off at £50bn, as it’s a decent price, with the only question being as to whether it’s the right one,” CMC Markets analyst Michael Hewson said in a note.

“It might be for GlaxoSmithKline and Pfizer, however there is a feeling that for Unilever it could well prove to be too high a price,” Hewson added.

Unilever, which is set to announce an initiative later this month to strengthen its business, said on Monday it was committed to “strict financial discipline” for any acquisitions, adding that such deals would be accompanied by the divestment of lower margin businesses or brands.

($1 = 0.7312 pounds)

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Pushkala Aripaka and Siddharth Cavale in Bengaluru, Keith Weir, Pamela Barbaglia, Carolyn Cohn and Simon Jessop in London and Ludwig Burger in Frankfurt; Editing by Shounak Dasgupta, Jane Merriman and Emelia Sithole-Matarise

Our Standards: The Thomson Reuters Trust Principles.

A Citibank sign is seen outside of a bank outlet in New York March 4, 2009. REUTERS/Lucas Jackson/File Photo

Register now for FREE unlimited access to Reuters.com

Register

NEW YORK, Jan 11 (Reuters) – Citigroup Inc (C.N) will exit its Citibanamex consumer banking business in Mexico, the bank said on Tuesday ending its 20-year retail presence in the country that was the last of its overseas consumer businesses.

Citigroup’s decision to sell or spin off Citibanamex, Mexico’s third biggest bank by assets as of June, is part of chief executive Jane Fraser’s strategy to bring Citigroup’s profitability and share price performance in line with its peers.

After taking up the top job last year, Fraser pledged to simplify Citigroup by exiting non-core businesses, including consumer franchises in 13 markets in Asia, Europe, the Middle East and Africa. While Citigroup’s Mexican exit was not part of the announced plan it is consistent with that “strategy refresh,” Fraser said on Tuesday.

Register now for FREE unlimited access to Reuters.com

Register

Citigroup will retain its institutional client business in Mexico, as it has in other overseas markets. It will focus its consumer banking business on a targeted U.S. retail presence, global wealth management, and payments and lending, it said.

The bank’s acquisition of Banamex for $12.5 billion in 2001 was the largest ever in Mexico at the time and came amid a wave of foreign purchases after an economic crisis devastated the country’s banking sector in the mid-1990s.

Mexican billionaire Ricardo Salinas Pliego, who is ranked as the country’s third-richest man with a family fortune estimated in excess of $15 billion by Forbes, said he was analyzing if it was possible to acquire Citibanamex.

Other possible buyers for Citibanamex could come from Canada, where the big six banks have excess cash to spend on deals. Bank of Nova Scotia (BNS.TO) already has a sizable Mexico business. read more

The local arms of Banco Santander (SAN.MC) and BBVA (BBVA.MC) would also have the cash, while Mexican institutions Banorte and Inbursa could use an acquisition of Citi’s operations to challenge this duo.

An industry laggard hobbled by creaky technology and poor risk-management controls, Citigroup’s seeming inability to fix its operational issues and boost its share price has frustrated shareholders. “Investor exhaustion” plagues the bank, Odeon Capital analyst Dick Bove said last month.

Fraser’s revamp amounts to the biggest overhaul for Citigroup since it was forced to unload assets following the 2007-2009 financial crisis. To date the bank has taken $2 billion in charges exiting Asian markets. read more

Before becoming CEO, Fraser was responsible for the Mexico business and for Citigroup’s global consumer bank. In that role she worked to build on investments the bank made to refurbish the Mexico consumer business which had been known as Banamex.

By disposing of the Mexico consumer businesses, “we’ll be able to direct our resources to opportunities aligned with our core strengths and competitive advantages,” Fraser said in a statement, adding Mexico remains “a priority market” for Citigroup’s institutional businesses.

“We expect Mexico to be a major recipient of global investment and trade flows in the years ahead, and we are confident about the country’s trajectory,” she said.

MERGER BINGE

Citigroup’s acquisition of Banamex was one of several led by Sandy Weill, CEO from 1998-2003, who built the bank into a U.S. giant and, some analysts believe, set it up for its problems.

Institutional investors and analysts, such as Mike Mayo of Wells Fargo, have long called for Citigroup to give up Citibanamex which they saw as drag on its investment returns.

Fraser’s predecessor as CEO, Mike Corbat, had invested more in Citibanamex even after it suffered loan losses in a massive fraud involving a supplier to Mexico’s state oil company.

Citigroup shares rose as much as 1% in after-market trading.

The bank did not estimate the cost of exiting the business or what it might receive in a sale. The business currently uses about $4 billion of tangible common equity.

The Mexico consumer businesses provided about $3.5 billion in revenue in the first three quarters of 2021 and $1.2 billion in pre-tax earnings, Citigroup said. They include $44 billion of Citigroup’s $2.36 trillion of total assets.

Citigroup said the timing of the exit is subject to regulatory approvals in the United States and Mexico.

Register now for FREE unlimited access to Reuters.com

Register

Additional reporting by David French and Noel Randewich; Editing by Howard Goller, Aurora Ellis and Muralikumar Anantharaman

Our Standards: The Thomson Reuters Trust Principles.

A man walks past a wall carrying the logo of Shimao Group, with residential buildings and the financial district of Pudong seen in the background, in Shanghai, China January 1, 2013. Picture taken January 1, 2013. REUTERS/Stringer

Register now for FREE unlimited access to Reuters.com

Register

Shimao puts assets on the block, ratings slashed again

Evergrande extends deadline for bond payment deferral

R&F next in focus with $750 mln debt payment on Thursday

HONG KONG/LONDON, Jan 10 (Reuters) – China’s property sector saw more drama on Monday after reports Shimao – investment grade-rated until a couple of months ago – had put all its projects up for sale, and Evergrande attempted to avoid another high-profile default.

More unwelcome surprises this month have meant no let up in the Chinese property crisis that wiped over a trillion dollars off the sector last year.

Monday’s twists saw Shimao Group’s credit rating cut again by both S&P and Moody’s after it unexpectedly defaulted on a “trust loan” last week, although its shares surged nearly 20% (0813.HK) on reports it was in talks about asset sales with state-backed giant China Vanke. read more

Register now for FREE unlimited access to Reuters.com

Register

China Evergrande (3333.HK), the world’s most indebted developer that first triggered the turmoil last year, said it had moved out of its Shenzhen headquarters to cut costs. read more

The company kept a glimmer of hope alive that its first “onshore” Chinese yuan bond default might still be avoided by extending until Thursday a deadline for bondholders to agree to a six-month, 4.5 billion yuan ($157 million) payment deferral. read more

Chinese property firms have faced unprecedented pressure over the last six months following efforts by Beijing to curb overborrowing in the sector.

Reuters reported last week that the government now plans to make it easier for state-backed property developers to buy up assets of struggling private rivals. read more

But the sector’s cash crunch is expected to intensify too with firms needing to make nearly $40 billion of international bond payments over the next six months according to brokerage Nomura, including almost $1.5 billion this week alone.

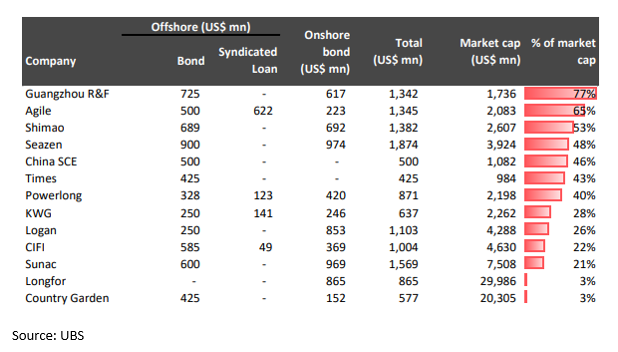

One of those likely to be highlighted alongside Evergrande on Thursday will be Guangzhou R&F Properties (2777.HK). Its bonds have slumped to deeply distressed levels ahead of a $750 million bond payment due that day . It also has a number of unfinished mega projects in global cities like London.

“I think the worst might be yet to come” said Himanshu Porwal, emerging markets corporate credit analyst at Seaport Global.

“A lot will depend on what the Chinese government does in terms of liquidity measures… But it has been four months already so I don’t know what they would be waiting for.”

China high yield crushed by property collapse

NEW LOWS

The woes of recent days have seen ICE’s China high-yield debt index (.MERACYC), which is dominated by homebuilders, hit an all-time low, while Evergrande and fellow-defaulter Kaisa have seen their bonds ejected from J.P. Morgan’s closely followed emerging market corporate debt index.

S&P and Moody’s both cut Shimao’s rating deeper into the junk category on Monday and warned of potential for a further downgrade.

S&P, which had rated Shimao investment grade as recently as November, cut it by a full two notches. It said, “The decline is worse than we previously anticipated. We now assess the company’s liquidity to be weak.”

Moody’s and Fitch also downgraded Yuzhou Group (1628.HK) due to increased refinancing risk while Moody’s withdrew the rating of another firm, Yango, due to “insufficient information.”

Separately, small developer Modern Land (1107.HK), which missed payment for its 12.85% notes due in October said in a filing on Monday that it has received notices from certain noteholders demanding early repayment of their senior notes.

The developer said it has been discussing a waiver with these creditors and has appointed financial advisers to formulate a plan. It is also in talks on a restructuring plan for $1.3 billion of its offshore bonds, the firm added.

Modern Land shares, which resumed trading after being suspended since Oct. 21, sank 40% in Hong Kong to HK$0.23.

“It’s going to be the peak of repayment period and we’ll see more developers default,” said Kington Lin, managing director of the asset management department at Canfield Securities Limited.

“The market is watching how many SOEs (state-owned enterprises) will get more M&A loans to help the developers in distress.”

Chinese property firms face big bills

(This story refiles to add dropped letter in first paragraph)

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Clare Jim and Donny Kwok in Hong Kong, Samuel Shen in Shanghai and Marc Jones in London; ; Editing by Kim Coghill, Shri Navaratnam, Tomasz Janowski and Cynthia Osterman

Our Standards: The Thomson Reuters Trust Principles.

A Tencent logo is seen in Beijing, China September 4, 2020. REUTERS/Tingshu Wang

Register now for FREE unlimited access to Reuters.com

Register

Move comes as Beijing cracks down on technology firms

JD.com shares plunge as much as 11.2%, Tencent up 4%

Tencent has no plans to sell stakes in other firms-source

BEIJING/HONG KONG, Dec 23 (Reuters) – Chinese gaming and social media company Tencent (0700.HK) will pay out a $16.4 billion dividend by distributing most of its JD.com (9618.HK) stake, weakening its ties to the e-commerce firm and raising questions about its plans for other holdings.

The move comes as Beijing leads a broad regulatory crackdown on technology firms, taking aim at their overseas growth ambitions and domestic concentration of market power.

Tencent said on Thursday it will transfer HK$127.69 billion ($16.37 billion) worth of its JD.com stake to shareholders, slashing its holding in China’s second-biggest e-commerce company to 2.3% from around 17% now and losing its spot as JD.com’s biggest shareholder to Walmart (WMT.N).

Register now for FREE unlimited access to Reuters.com

Register

The owner of WeChat, which first invested in JD.com in 2014, said it was the right time for the divestment, given the e-commerce firm had reached a stage where it can self-finance its growth.

Chinese regulators have this year blocked Tencent’s proposed $5.3 billion merger of the country’s top two videogame streaming sites, ordered it to end exclusive music copyright agreements and found WeChat illegally transferred user data.

The company is one of a handful of technology giants that dominate China’s internet space and which have historically prevented rivals’ links and services from being shared on their platforms.

“This seems to be a continuation of the concept of bringing down the walled gardens and increasing competition among the tech giants by weakening partnerships, exclusivity and other arrangements which weaken competitive pressures,” Mio Kato, a LightStream Research analyst who publishes on Smartkarma said of the JD.com stake transfer.

“It could have implications for things like the payments market where Tencent’s relationships with Pinduoduo and JD have helped it maintain some competitiveness with Alipay,” he said.

JD.com shares plunged 11.2% in early trade in Hong Kong on Thursday, the biggest daily percentage decline since its debut in the city in June 2020, before recovering partially to a 7% decline by 0450 GMT. Shares of Tencent, Asia’s most valuable listed company, rose 4%.

Shares of Tencent and JD on Dec 23

The companies said they would continue to have a business relationship, including an ongoing strategic partnership agreement, though Tencent Executive Director and President Martin Lau will step down from JD.com’s board immediately.

Eligible Tencent shareholders will be entitled to one share of JD.com for every 21 shares they hold.

PORTFOLIO DIVESTMENTS?

The JD.com stake is part of Tencent’s portfolio of listed investments valued at $185 billion as of Sept. 30, including stakes in e-commerce company Pinduoduo (PDD.O), food delivery firm Meituan (3690.HK), video platform Kuaishou (1024.HK), automaker Tesla (TSLA.O) and streaming service Spotify (SPOT.N).

Alex Au, managing director at Hong Kong-based hedge fund manager Alphalex Capital Management, said the JD.com sale made both business and political sense.

“There might be other divestments on their way as Tencent heed the antitrust call while shareholders ask to own those interests in minority stakes themselves,” he said.

A person with knowledge of the matter told Reuters Tencent has no plans to exit its other investments. When asked about Pinduoduo and Meituan, the person said they are not as well-developed as JD.com.

Tencent chose to distribute the shares as a dividend rather than sell them on the market in an attempt to avoid a steep fall in JD.com’s share price as well as a high tax bill, the person added.

Kenny Ng, an analyst at Everbright Sun Hung Kai, said the decision was “definitely negative” for JD.com.

“Although Tencent’s reduction of JD’s holdings may not have much impact on JD’s actual business, when the shares are transferred from Tencent to Tencent’s shareholders, the chances of Tencent’s shareholders selling JD’s shares as dividends will increase,” he said.

Technology investor Prosus (PRX.AS), which is Tencent’s largest shareholder with a 29% stake and is controlled by Naspers of South Africa, will receive the biggest portion of JD.com shares.

Walmart owns a 9.3% stake in JD.com, according to the Chinese company. Payments processor Alipay is part of Tencent rival Alibaba Group .

($1 = 7.7996 Hong Kong dollars)

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Sophie Yu in Beijing and Scott Murdoch in Hong Kong; Additional reporting by Xie Yu, Selena Li, Donny Kwok and Eduardo Baptista in Hong Kong and Nikhil Kurian Nainan in Bengaluru; Writing by Jamie Freed; Editing by Subhranshu Sahu and Muralikumar Anantharaman

Our Standards: The Thomson Reuters Trust Principles.

Amazon 2019 Future deal was at heart of ongoing legal disputes

India watchdog suspends deal, says Amazon suppressed info in 2019

Amazon should pay penalty of 2 billion rupees-watchdog

Suspension of deal latest legal twist in Future-Amazon saga

NEW DELHI, Dec 17 (Reuters) – India’s antitrust agency suspended Amazon.com’s (AMZN.O) 2019 deal with Future Group on Friday, potentially denting the U.S. e-commerce giant’s attempts to block the sale of Future’s retail assets to an Indian market leader.

The regulator ruled that the U.S. company had suppressed information while seeking regulatory approval on an investment into Indian retailer Future Group two years ago.

The ruling by the Competition Commission of India (CCI) could have far-reaching consequences for Amazon’s legal battles with now estranged partner Future.

Register now for FREE unlimited access to Reuters.com

Register

Amazon has for months successfully used the terms of its toehold $200 million investment in Future in 2019 to block the Indian retailer’s attempt to sell retail assets to Reliance Industries (RELI.NS) for $3.4 billion.

The regulator’s 57-page order said it considers “it necessary to examine the combination (deal) afresh,” adding its approval from 2019 “shall remain in abeyance” until then.

The CCI’s order said Amazon had “suppressed the actual scope” of the deal and had made “false and incorrect statements” while seeking approvals.

“The approval is suspended. This is absolutely unprecedented,” said Shweta Dubey, a partner at Indian law firm SD Partners, who was formerly a CCI official.

“The order seems to have found new power for CCI to keep the combination approval in abeyance,” she added.

With the 2019 Future deal’s antitrust approval now suspended, it could dent Amazon’s legal position and retail ambitions, while making it easier for Reliance – the country’s largest retailer – to acquire number two player Future, people familiar with the dispute said.

The CCI also imposed a penalty of around 2 billion rupees ($27 million) on the U.S. company, adding that Amazon will be given time to submit information again to seek approvals, the CCI added.

Future Group, however, is unlikely to cooperate with Amazon if it tries to reapply for antitrust clearance after the CCI’s decision, a source with direct knowledge told Reuters.

The Indian company is also set to take CCI’s Friday decision before various legal forums to argue that Amazon has no legal basis to challenge its asset sale, the source added.

Future and Reliance did not respond to a request for comment. Amazon said it is reviewing the order “and will decide on its next steps in due course.”

RETAIL BATTLE

The dispute over Future Retail, which has more than 1,500 supermarket and other outlets, is the most hostile flashpoint between Jeff Bezos’ Amazon and Reliance, run by India’s richest man Mukesh Ambani, as they try to gain the upper hand in winning retail consumers.

Hit by the COVID-19 pandemic, Future last year decided to sell its retail assets to Reliance for $3.4 billion, but Amazon managed to block the sale successfully through legal challenges.

Amazon cited breach of contracts by Future, arguing that terms agreed in 2019 to pay $200 million for a 49% stake in Future’s gift voucher unit prevented its parent, Future Group, from selling its Future Retail Ltd (FRTL.NS) business to certain rivals, including Reliance.

The CCI review of the deal started after Future, which denies any wrongdoing, complained, saying that Amazon was making contradictory statements before different legal forums about the intent of the 2019 transaction.

In June, the CCI told Amazon the U.S. firm in 2019 explained its interest in investing in Future’s gift voucher unit as one that would address gaps in India’s payments industry. But later, the CCI said, Amazon disclosed in other legal forums the foundation of its investment in the Future unit was to obtain special rights over the retail arm, Future Retail.

In the Friday order, CCI said there was “a deliberate design on the part of Amazon to suppress the actual scope and purpose of the” deal.

Ahead of CCI’s decision, Amazon denied concealing any information and warned the watchdog that Future’s bid to unwind the 2019 deal to allow Reliance to consolidate its position “will further restrict competition in the Indian retail market”.

Register now for FREE unlimited access to Reuters.com

Register

Reporting by Aditya Kalra in New Delhi;

Editing by Euan Rocha, Jane Merriman and Louise Heavens

Our Standards: The Thomson Reuters Trust Principles.