- Asia And Europe Markets Dip, Crude Slips To $85 – Global Markets Today While US Was Sleeping – ETC Gavekal Asia Pacific Government Bond ETF (ARCA:AGOV), SmartETFs Asia Pacific Dividend Builder ETF (ARCA:ADIV) Benzinga

- Asia markets see broad sell off as Japan sees surprise trade surplus; Bank of Korea holds rates CNBC

- Morning Bid: Five alive: US yield curve nears historic level Reuters

- US Stocks Close Sharply Lower, Asian Shares Under Pressure; Weak Start On D-Street? | CNBC TV18 CNBC-TV18

- Asia markets set to extend losses after Powell’s comments; Japan inflation slows CNBC

- View Full Coverage on Google News

Tag Archives: Crude

Asia And Eurozone Markets Lower, Crude Oil Trades In Green – Global Markets Today While US Was Sleeping – ETC Gavekal Asia Pacific Government Bond ETF (ARCA:AGOV), SmartETFs Asia Pacific Dividend Builder ETF (ARCA:ADIV) – Benzinga

- Asia And Eurozone Markets Lower, Crude Oil Trades In Green – Global Markets Today While US Was Sleeping – ETC Gavekal Asia Pacific Government Bond ETF (ARCA:AGOV), SmartETFs Asia Pacific Dividend Builder ETF (ARCA:ADIV) Benzinga

- Hong Kong leads Asia-Pacific markets lower; Australia’s central bank keeps interest rate unchanged CNBC

- Asian Markets Trade Lower Following A Mixed Close On Wall Street; D-Street To Open Lower? CNBC-TV18

- Asian stocks slip on rate worries, yen in focus Reuters.com

- Hong Kong stocks slide after long weekend as threat of US rate hike haunts market South China Morning Post

- View Full Coverage on Google News

American-owned tanker offloads oil believed to be Iranian crude near Texas — despite Tehran’s threats – New York Post

- American-owned tanker offloads oil believed to be Iranian crude near Texas — despite Tehran’s threats New York Post

- US tanker unloading suspected embargoed Iranian oil despite Tehran’s warnings The Times of Israel

- A tanker believed to hold sanctioned Iran oil starts offloading near Texas despite Tehran’s threats Yahoo Finance

- Tanker believed to hold sanctioned Iran oil begins to be offloaded near Texas despite Tehran threats Firstpost

- Tanker Believed to Hold Iran Oil Begins to be Offloaded Near Texas Voice of America – VOA News

- View Full Coverage on Google News

Crude Oil drops to a new year low, what’s happening?

Here’s how to make sense of the different figures reported by the Energy Information Administration (EIA).

Macroeconomics

From a macroeconomic point of view, the US dollar index (DXY or USDX) has maintained its downward trend within its recent regression channel, probably still eyeing the next quarterly S2 pivot just located at the $100 mark.

US Dollar Currency Index (DXY), daily chart

As we will see in this article, a certain lack of appetite for petroleum products is fueling the general impression of anemic demand, stifled by hikes in key interest rates by central banks (the Federal Reserve, the European Central Bank, the Bank of England, etc.) around the world combined with the slowing economy.

Geopolitical and fundamental analysis

The price of a barrel of West Texas Intermediate (WTI) closed Wednesday down 3% after falling a moment earlier to its lowest level of the year ($71.75 on the January futures contract). As the geopolitical fears were placed in the background, even the EU’s price cap on Russian oil has not really impacted the market, as I mentioned last week, given that Russia has made investments into its own fleet of oil tankers, so they have the option to deliver their Urals crude oil by putting their own conditions or even simply finding other clients eventually.

Already resolutely on the downside for several days as concerns over supply risk are gradually evaporating, the black gold market was encouraged to continue in this downward momentum by the EIA’s weekly report on US crude oil inventories.

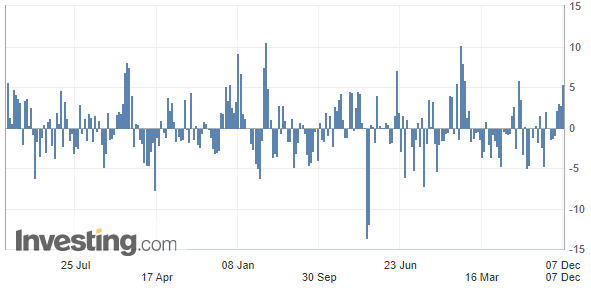

US Crude Oil inventories

(Source: Investing.com)

Operators ignored the significant contraction of 5.187 million barrels in commercial crude reserves to focus on stocks of refined products to get an overview of US petroleum demand.

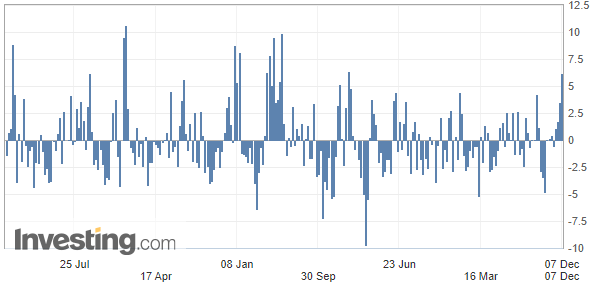

US Gasoline inventories

(Source: Investing.com)

The oil market is sinking due to a significant increase in gasoline stocks, which rose by 5.320

million barrels, nearly doubling expectations (2.7 million barrels).

US EIA weekly distillates stocks

Now, regarding the reserves of distilled products – such as diesel, mainly – they also increased significantly, by 6.159 million barrels versus the 2.2 million barrels forecasted.

(Source: Investing.com)

In fact, this figure has to be compared to the demand for refined products in the United States, which remained, last week, below its level of 2021 at the same time, whereas on average over the past four weeks, the demand for gasoline dropped more than 7% lower than a year ago.

Finally, OPEC+’s decision last Sunday (Dec 4th) to maintain their production and not reduce it further, is another bearish factor.

Technical charts

WTI Crude Oil (CLF23) Futures (January contract, daily chart)

WTI Crude Oil (CLF23) Futures (January contract, 4H chart)

RBOB Gasoline (RBF23) Futures (January contract, daily chart)

Brent Crude Oil (BRNG23) Futures (February contract, daily chart) – Contract for Difference (CFD) UKOIL

That’s all for today, folks! Happy trading!

Investigation found Boston Celtics coach Ime Udoka used crude language in dialogue with female subordinate prior to start of improper relationship

The independent law firm probe into Boston Celtics coach Ime Udoka found that he used crude language in his dialogue with a female subordinate prior to the start of an improper workplace relationship with the woman, an element that significantly factored into the severity of his one-year suspension, sources told ESPN.

Those investigative findings — which described verbiage on Udoka’s part that was deemed especially concerning coming from a workplace superior — contribute to what is likely a difficult pathway back to his reinstatement as Celtics coach in 2023, sources told ESPN.

The power dynamic associated with a superior’s improper relationship with a staff member was the primary finding and policy violation cited in the law firm’s report, which was commissioned by the Celtics and completed early last week, sources said.

At a news conference last week, Celtics owner Wyc Grousbeck said the suspension — which extends through June 30, 2023 — was a product of multiple violations of team policies, and sources told ESPN the Celtics won’t stand in Udoka’s way should he have the chance to become a coaching candidate elsewhere. There are teams that have tried to gather a preliminary understanding of the full explanation for Udoka’s suspension in preparation for possibly evaluating him for future coaching employment, sources told ESPN.

Grousbeck also said Udoka would be receiving a cut in his salary during the suspension.

In his first season, Udoka, 45, led the Celtics to an Eastern Conference championship and NBA Finals berth, where Boston lost in six games to the Golden State Warriors. The Celtics return a team expected again to be a championship favorite, and Udoka had appeared destined for a long runway as the franchise’s coach after replacing Brad Stevens, who moved into the front-office role previously occupied by Danny Ainge during the 2021 offseason.

Grousbeck said during the news conference that no one else within the organization faced discipline as a result of the investigation. The Celtics wouldn’t confirm the nature of the violations, but Stevens, the team’s president of basketball operations, became emotional when describing the number of women employed by the Celtics who were targeted by unfounded social media rumors and allegations.

The Celtics promoted assistant coach Joe Mazzulla to interim coach for the upcoming season. Mazzulla, 34, is well-regarded inside and outside of the Celtics organization and counts Stevens among his most significant supporters. Mazzulla was a finalist for the Utah Jazz head-coaching job over the summer that went to top Celtics assistant Will Hardy.

Grousbeck and Stevens would not elaborate on the criteria Udoka would need to meet to return to coaching the Celtics following his suspension.

Grousbeck defended the Celtics’ decision to suspend Udoka for the entire season, insisting it was the proper response based on the probe’s findings.

“This felt right, but there’s no clear guidelines for any of this,” he said. “It’s conscience and gut feel. … We collectively came to this and got there but it was not clear what to do but it was clear something substantial needed to be done, and it was.”

ESPN’s Tim Bontemps contributed to this report.

Brent crude slides below $85 a barrel as dollar surges

An aerial view of Phillips 66 oil refinery is seen in Linden, New Jersey, United States.

Tayfun Cosku | Anadolu Agency | Getty Images

Brent crude fell below $85 a barrel Monday, as recession fears weighed and the U.S. dollar surged.

Brent futures for November settlement were trading down over 1% around $84.92 at 8 a.m. London time. West Texas Intermediate futures also fell to trade around $77.93.

The U.S. dollar surged to a high not seen since 2002 Monday, while sterling tumbled to a record low against the currency.

On Friday, both Brent and WTI futures fell around 5% to hit their lowest level since January.

It comes as central banks around the world — including the U.S. and the U.K. — continue to hike interest rates in an effort to tackle inflation.

Meanwhile, fears around an economic slowdown continue to mount, with Steve Hanke, professor of applied economics at Johns Hopkins University, putting the chance that the U.S. will fall into recession at 80%.

“If [the Fed] continue[s] the quantitative tightening and move that growth rate and M2 (money supply) into negative territory, it’ll be severe,” Hanke told CNBC’s “Street Signs Asia” on Friday.

This is a breaking news story and will be updated shortly.

Brent crude hits pre-Ukraine invasion lows on recession fears

FILE PHOTO – A PetroChina worker inspects a pump jack at an oil field in Tacheng, Xinjiang Uighur Autonomous Region, China June 27, 2018. REUTERS/Stringer AT

Register now for FREE unlimited access to Reuters.com

LONDON, Aug 4 (Reuters) – Oil prices fell on Thursday, with Brent touching $93.50 a barrel – the lowest since Feb. 21 before Russia’s invasion of Ukraine sent prices soaring – as fears mounted of an economic recession which could sap fuel demand.

Brent crude futures were down $2.88, or 3%, at $93.90 a barrel by 1543 GMT, while West Texas Intermediate (WTI) crude futures fell $2.37, a 2.6% decline, to $88.29.

Brent hit a low of $93.50, the lowest since Feb. 21 while U.S. crude touched its lowest since Feb. 3 at $87.97.

Register now for FREE unlimited access to Reuters.com

The selling followed an unexpected surge in U.S. crude inventories last week. Gasoline stocks, the proxy for demand, also showed a surprise build as demand slowed, the Energy Information Administration said. read more

The demand outlook remained clouded by increasing worries about an economic slump in the United States and Europe, debt distress in emerging market economies, and a strict zero COVID-19 policy in China, the world’s largest oil importer.

“A break below $90 is now a very real possibility which is quite remarkable given how tight the market remains and how little scope there is to relieve that,” said Craig Erlam, senior market analyst at Oanda in London.

“But recession talk is getting louder and should it become reality, it will likely address some of the imbalance.”

Further pressure followed fears that rising interest rates could slow economic activity and limit demand for fuel. The Bank of England (BoE) raised rates on Thursday and warned about recession risks.

An OPEC+ agreement on Wednesday to raise its output target by just 100,000 barrels per day (bpd) in September, equivalent to 0.1% of global demand, was viewed by some analysts as bearish for the market. read more

OPEC heavyweights Saudi Arabia and the UAE are ready to deliver a “significant increase” in oil output should the world face a severe supply crisis this winter, sources familiar with the thinking of the top Gulf exporters said. read more

Register now for FREE unlimited access to Reuters.com

Additional reporting by Laura Sanicola and Emily Chow; Editing by Bernadette Baum

Our Standards: The Thomson Reuters Trust Principles.

Saudis Unwilling To Upset Putin As Biden Begs For More Crude

The world’s largest crude oil exporter, Saudi Arabia, continues to keep close ties with Russia while the top oil consumer, the United States, pleads with major producers—including the Kingdom—to boost supply to the market and help ease consumers’ pain at the pump. While the U.S. and its Western allies are sanctioning Moscow and banning oil imports from Russia, U.S. President Joe Biden is also turning to Saudi Arabia to ask it to pump more oil as Americans pay on average $5 a gallon for gasoline.

The Saudis prefer to keep close ties with Russia in oil policy as the OPEC+ pact and the control over a large portion of global oil supply has benefited both OPEC+ leaders—the Kingdom and Russia—over the past half a decade. Saudi Arabia, however, could use a little thaw in Saudi-U.S. relations under President Biden, who is no longer talking about the world’s top crude exporter as a “pariah” state.

The Saudis are carefully maneuvering to keep Russia as an ally in the OPEC+ group and possibly improve relations with the United States.

President Biden—desperate to see relief for American drivers ahead of the midterm elections—has made a U-turn on Saudi Arabia and is expected this month to visit the Kingdom, which he said on the campaign trail would be treated as a “pariah” state during his presidency. But U.S. gasoline prices at $5 a gallon and the loss of part of the Russian supply have made President Biden reconsider and meet with Crown Prince Mohammed bin Salman.

Related: Europe’s Power Prices Surge As Market Fears Worsening Supply Crunch

Saudi Arabia has publicly reiterated its “warm” ties with Russia on several occasions since Putin invaded Ukraine, and considers keeping Russia in the OPEC+ alliance an important part of its oil policy. With Russia leading a dozen non-OPEC producers in the pact, Saudi Arabia has more sway over global oil markets with the larger OPEC+ group than with OPEC alone.

Russian President Vladimir Putin and Saudi Crown Prince Mohammed bin Salman have discussed their countries’ cooperation in the OPEC+ oil production pact in a few telephone conversations since February, and have vowed to continue their cooperation.

Last month, Russian Deputy Prime Minister Alexander Novak said that Russia could continue its participation in the OPEC+ agreement even after it officially expires at the end of this year. Novak was speaking after a meeting in St Petersburg with Saudi Arabia’s Energy Minister, Prince Abdulaziz bin Salman, who made a surprise appearance at a Russian economic forum.

During that meeting, the Saudi minister said that Saudi-Russian relations were “as warm as the weather in Riyadh.”

Two weeks before that meeting, Russia’s Foreign Minister Sergey Lavrov visited Riyadh and met with his Saudi counterpart Prince Faisal bin Farhan Al Saud. The two ministers said that the OPEC+ alliance is solid, with the level of cooperation within it strong.

The recent OPEC+ decision to accelerate the production increase and roll back all cuts in August, a month earlier than initially planned, was pushed by Saudi Arabia amid U.S. pressure. But the Kingdom had to check with Russia first before proposing the redistribution of the September increase in July and August, sources with knowledge of the behind-the-scenes diplomacy told Reuters this week.

Related: Oil Prices Rebound As Crude Supply Tightens

Both the Saudis and Russia benefit from the OPEC+ deal, so Riyadh wants to keep Russia on board, the sources say.

“The Saudis are enjoying high prices while the Russians need guaranteed support from OPEC+ in the current circumstances,” a source familiar with Russian thinking told Reuters.

“No one is interested in a market collapse,” added the source.

After the production cuts are completely rolled back next month, a more difficult decision for OPEC+ looms: what to do next as Russia is more than 1 million bpd behind target and could lose more supply as the EU embargo on its oil begins at the end of this year.

Neither is OPEC+ as a group anywhere close to reaching its target production, nor has Saudi Arabia much spare capacity left to boost production further, as the U.S. and other major consumers want. Per the OPEC+ deal, the Saudi target (as well as Russia’s) is at 11.004 million bpd for August. The Kingdom has rarely reached this level, and not for a sustained period of time. So, it’s not certain that the Saudis have the ability to pump 11 million bpd or more on a sustainable basis. It’s even less certain that the Kingdom can quickly tap—if it wanted to—into the 12.2 million bpd production capacity it claims it has.

By Tsvetana Paraskova for Oilprice.com

More Top Reads From Oilprice.com:

Oil jumps after Saudi Arabia hikes crude prices

A drilling rig operates in the Permian Basin oil and natural gas production area in Lea County, New Mexico, U.S., February 10, 2019. REUTERS/Nick Oxford/File Photo

Register now for FREE unlimited access to Reuters.com

MELBOURNE, June 6 (Reuters) – Oil prices rose more than $2 in early trade on Monday after Saudi Arabia raised prices sharply for its crude sales in July, an indicator of how tight supply is even after OPEC+ agreed to accelerate its output increases over the next two months.

Brent crude futures were up $1.80, or 1.5%, at $121.52 a barrel at 2319 GMT after touching an intraday high of $121.95, extending a 1.8% gain from Friday.

U.S. West Texas Intermediate (WTI) crude futures were up $1.63, or 1.4%, at $120.50 a barrel after hitting a three-month high of $120.99. The contract gained 1.7% on Friday.

Register now for FREE unlimited access to Reuters.com

Saudi Arabia raised the official selling price (OSP) for its flagship Arab light crude to Asia to a $6.50 premium versus the average of the Oman and Dubai benchmarks, up from a premium of $4.40 in June, state oil produce Aramco (2222.SE) said on Sunday. read more

The move came despite a decision last week by the Organization of the Petroleum Exporting Countries and allies, together called OPEC+, to increase output in July and August by 648,000 barrels per day, or 50% more than previously planned.

“Mere days after opening the spigots a bit wider, Saudi Arabia wasted little time hiking its official selling price for Asia, its primary market…seeing knock-on effects at the futures open across the oil market spectrum,” SPI Asset Management managing partner Stephen Innes said in a note.

Saudi Arabia also increased the Arab Light OSP to northwest Europe to $4.30 above ICE Brent for July, up from a premium of $2.10 in June. However, it held the premium steady for barrels going to the United States at $5.65 above the Argus Sour Crude Index (ASCI).

The OPEC+ move to bring forward output hikes is widely seen as unlikely to meet demand as several member countries, including Russia, are unable to boost output, while demand is soaring in the United States amid peak driving season and China is easing COVID lockdowns.

“While that increase is sorely needed, it falls short of demand growth expectations, especially with the EU’s partial ban on Russian oil imports also factored in,” Commonwealth Bank analyst Vivek Dhar said in a note.

Register now for FREE unlimited access to Reuters.com

Reporting by Sonali Paul in Melbourne; Editing by Sam Holmes

Our Standards: The Thomson Reuters Trust Principles.

Oil jumps after Saudi Arabia hikes crude prices

MELBOURNE (Reuters) – Oil prices rose more than $2 in early trade on Monday after Saudi Arabia raised prices sharply for its crude sales in July, an indicator of how tight supply is even after OPEC+ agreed to accelerate its output increases over the next two months.

Brent crude futures were up $1.80, or 1.5%, at $121.52 a barrel at 2319 GMT after touching an intraday high of $121.95, extending a 1.8% gain from Friday.

U.S. West Texas Intermediate (WTI) crude futures were up $1.63, or 1.4%, at $120.50 a barrel after hitting a three-month high of $120.99. The contract gained 1.7% on Friday.

Saudi Arabia raised the official selling price (OSP) for its flagship Arab light crude to Asia to a $6.50 premium versus the average of the Oman and Dubai benchmarks, up from a premium of $4.40 in June, state oil produce Aramco said on Sunday.

The move came despite a decision last week by the Organization of the Petroleum Exporting Countries and allies, together called OPEC+, to increase output in July and August by 648,000 barrels per day, or 50% more than previously planned.

“Mere days after opening the spigots a bit wider, Saudi Arabia wasted little time hiking its official selling price for Asia, its primary market…seeing knock-on effects at the futures open across the oil market spectrum,” SPI Asset Management managing partner Stephen Innes said in a note.

Saudi Arabia also increased the Arab Light OSP to northwest Europe to $4.30 above ICE Brent for July, up from a premium of $2.10 in June. However, it held the premium steady for barrels going to the United States at $5.65 above the Argus Sour Crude Index (ASCI).

The OPEC+ move to bring forward output hikes is widely seen as unlikely to meet demand as several member countries, including Russia, are unable to boost output, while demand is soaring in the United States amid peak driving season and China is easing COVID lockdowns.

“While that increase is sorely needed, it falls short of demand growth expectations, especially with the EU’s partial ban on Russian oil imports also factored in,” Commonwealth Bank analyst Vivek Dhar said in a note.

(Reporting by Sonali Paul in Melbourne; Editing by Sam Holmes)