Federal Reserve Gov. Christopher Waller said Sunday that financial markets seem to have overreacted to the softer-than-expected October consumer price inflation data last week.

“It was just one data point,” Waller said, in a conversation in Sydney, Australia, sponsored by UBS.

“The market seems to have gotten way out in front over this one CPI report. Everybody should just take a deep breath, calm down. We’ve got a ways to go ” Waller said.

Investors cheered the soft CPI print, released Thursday, driving stocks up to their best week since June. The S&P 500 index

SPX,

+0.92%

closed 5.9% higher for the week.

The data showed that the yearly rate of consumer inflation fell to 7.7% from 8.2%, marking the lowest level since January. Inflation had peaked at a nearly 41-year high of 9.1% in June.

Waller said it was good there was some evidence that inflation was coming down, but noted that there were other times over the past year where it looked like inflation was turning lower.

“We’re going to see a continued run of this kind of behavior and inflation slowly starting to come down, before we really start thinking about taking our foot off the brakes here,” Waller said.

“We’ve got a long, long way to go to get inflation down. Rates are going keep going up and they are going to stay high for awhile until we see this inflation get down closer to our target,” he added.

The Fed is focused on how high rates need to get to bring inflation down, and that will depend solely on inflation, he said.

Waller said “the worst thing” the Fed could do was stop raising rates only to have inflation explode.

The 7.7% inflation rate seen in October “is enormous,” he added.

The Fed signaled at its last meeting earlier this month that it might slow down the pace of its rate hikes in coming meetings.

The central bank has boosted rates by almost 400 basis points since March, including four straight 0.75-percentage-point hikes that had been almost unheard of prior to this year.

“We’re looking at moving in paces of potentially 50 [basis points] at the next meeting or the next meeting after that,” Waller said.

The Fed will hold its next meeting on Dec. 13-14, and then again on Jan. 31-Feb. 1.

At the same time, Powell said the Fed was likely to raise rates above the 4.5%-4.75% terminal rate that they had previously expected.

“The signal was ‘quit paying attention to the pace and start paying attention to where the endpoint is going to be,’” Waller said.

In the wake of the CPI report, investors who trade fed funds futures contracts see the Fed’s terminal rate at 5%-5.25% next spring and then quickly falling back to 4.25%-4.5% by November. That’s well below the levels prior to the CPI data.

Billionaire Dallas Maverick’s owner Mark Cuban recently offered his perspective on the implosion of crypto platform FTX late this week.

“‘That’s somebody running a company that’s just dumb-as-fucking greedy.’”

— Mark Cuban

Cuban, speaking on Friday at a conference in Washington, D.C. hosted by Sports Business Journal, shared the view that avarice was at the root of the downfall of one-time crypto darling Sam Bankman-Fried, whose firm FTX Group just filed for chapter 11 bankruptcy.

“So what does Sam Bankman [Fried] do, he’s just–‘gimme more, gimme more, gimme more.’ So I’m gonna borrow money, loan it to an affiliated company and hope and pretend to myself that the FTT tokens that are in there on my balance sheet are gonna to sustain their value.”

Check out: Mark Cuban says buying metaverse real estate is ‘the dumbest shit ever

FTX’s collapse marks a stunning turnabout for a company, which was once valued at $26 billion, and whose founder, Bankman-Fried was viewed by many in the crypto industry as a venerable actor in the Wild West of digital exchanges.

On Thursday, the 30-year-old entrepreneur tweeted: “I f—ked up, and should have done better,” referencing the collapse of his exchange.

Embattled FTX, short billions of dollars, sought bankruptcy protection after the exchange experienced the crypto equivalent of a bank run. FTX, an affiliated hedge fund Alameda Research, and dozens of other related companies also filed a bankruptcy petition in Delaware on Friday morning. Boasting a nearly $16 billion fortune recently, Sam Bankman Fried’s net worth had all but evaporated in the wake of the FTX implosion, according to the Bloomberg Billionaires Index.

The price of FTX’s native token FTT went down about 88.8% over the past seven days to around $2.74, according to CoinMarketCap data.

The U.S. Justice Department and the Securities and Exchange Commission are looking into the crypto exchange to determine whether any criminal activity or securities offenses were committed.

Regulators and are examining whether FTX used customer deposits to fund bets at Alameda Research, a no-no in traditional markets, according to reports.

Cuban, who is one of the stars of the investing show “Shark Tank” and owns the NBA’s Dallas Mavericks, is a big investor in crypto and blockchain-related platforms. According to a CNBC report, he has said that 80% of his investments that aren’t on Shark Tank are crypto-centric.

See: Tom Brady, Steph Curry and Kevin O’Leary set to lose big from FTX bankruptcy filing

For his part, Cuban is part of a class-action lawsuit accused of misleading investors into signing up for accounts with crypto platform Voyager Digital, which filed for bankruptcy in July. The suit alleges that Cuban touted his support for Voyager and referred to it “as close to risk-free as you’re gonna get in the crypto universe.”

Cuban mentioned Voyager in his Friday interview. Representatives for the billionaire investor didn’t immediately respond to a request for comment.

The Mavericks owner took to Twitter on Saturday to say that the crypto implosions “have been banking blowups. Lending to the wrong entity, misvaluations of collateral, arrogant arbs, followed by depositor runs.”

Cuban’s net worth is $4.6 billion, according to Forbes.

Twitter users have complained a lot about Elon Musk’s early moves after taking control of the social network, but their complaints seem tiny compared with what Tesla Inc. investors have had to suffer.

As the U.S. focused on election returns Tuesday evening, Tesla

TSLA,

-7.17%

Chief Executive Musk tried to slip through disclosure of his long-awaited stock sales, revealing that he had sold nearly $4 billion of Tesla stock in the previous three trading sessions. Musk did not publicly address the stock sales nor his intentions to sell more within 24 hours of the disclosure, even while tweeting roughly 20 times in that period.

[MarketWatch asked him on Twitter to address the sales twice, and did not receive a reply; Tesla disbanded its media-relations department years ago.]

The sales fueled a further downturn in shares of the electric-vehicle maker on Wednesday, when the stock fell 7.2% to $177.59, its lowest closing price since November 2020. Tesla is currently down 49.6% on the year, which would be far and away the worst year yet for the stock — the previous record annual decline was 2016, when it fell 11%.

The problems for Tesla investors go far beyond Musk selling its stock so that he could overpay for a company with limited growth prospects and a host of other problems, but the poor optics certainly start there.

“He sold caviar to buy a $2 slice of pizza,” said Dan Ives, a Wedbush Securities analyst.

Ives was one of several on Wall Street to predict Musk would need to sell more shares to either close a gap in his financing of the $44 billion deal to buy the social-media company, or provide additional operating funds. In a telephone conversation Wednesday, he said the Twitter move is “a nightmare that just won’t end for Tesla investors.”

One reason it isn’t ending is that Musk’s need for cash in relation to Twitter is not done with the recent sales, portending more in the future. Musk said in a tweet late last week that Twitter had a “massive drop in revenue” due to activists pressuring advertisers to pull their ads, and he will have to continue paying the employees he did not lay off while servicing a debt load that analysts have estimated will cost him $1 billion a year, much more than Twitter has cleared in profit in the past two years. Twitter reported a net loss of $221 million in 2021, and a net loss of $1.13 billion for 2020.

Read more about Elon Musk potentially pumping Tesla stock ahead of a sale

“The first two weeks of ownership have been a ‘Friday the 13th‘ horror show,” Ives said, adding that the verification plan and mass layoffs of 50% of employees — and then trying to rehire some of the engineers, developers and cybersecurity experts — was “really stupid.” And, according to CNBC, Musk has also pulled more than 50 Tesla engineers, many from the Autopilot team, to work at Twitter.

“But it’s consistent with how this thing has been handled,” Ives said, adding that Musk is “way over his skis” with the Twitter acquisition.

Amid all the chaos of his first two weeks running Twitter, how much time has Musk had to run his other companies? Musk was already splitting his Tesla time with SpaceX, The Boring Company, Neuralink and many other endeavors, and now he has taken on the gargantuan task of turning a social-media company that has never been highly profitable, nor valuable, into something worth the $44 billion he paid.

The effort, Ives said, has “tarnished his brand,” which in turn has a big risk of hurting Tesla. Many investors have bought into the Tesla story because they believe Musk is a genius and they back his vision of electrifying the automotive industry. Twitter does not meld into that vision, except as a platform to spout his opinions, vitriol and promote more wacky concepts.

Since Musk began his quest to buy the company, he has endured more criticism than ever before, with even some fans starting to throw shade or question his decisions. Investor Gary Black, managing partner of the Future Fund LLC, for example, pointed out that Tesla’s top engineers should not be running Twitter, where the news was getting worse.

Tesla is not a company that can just run itself at this point. Musk has claimed he did not want to be chief executive but that there was no one else to take over the car company, which is why he has served as CEO for years. It’s not clear, though, how much effort he actually has made at trying to recruit someone. Now, as Tesla faces its usual multitude of issues, he is off spending his time trying to turn Twitter into a payments company, or maybe a subscription company, or maybe an “everything app,” or whatever he comes up with tomorrow.

“Musk needs to look in the mirror and end this constant merry-go-round of Twitter overhang on the Tesla story, with his focus back on the golden child Tesla, which needs his time more than ever given the soft macro, production/delivery issues in China, and EV competition increasing from all corners of the globe,” Ives wrote in a note Wednesday, in which he reiterated an outperform rating on Tesla stock.

For Twitter to reach anywhere close to the valuation Musk paid for it, it’s going to need a ton of attention from a focused leader, but how can Musk be that leader and give Tesla the attention it deserves? The answer is he cannot, and is very likely to give the attention that Tesla needs to Twitter instead after committing $44 billion (not all of it his) to that endeavor. Tesla investors will be left staring at the sea of red that this year has wrought, and wondering if its leader is about to sell more shares to fund his other effort.

The past week offered a tale of two markets, with gains for the Dow Jones Industrial Average putting the blue-chip gauge on track for its best October on record while Big Tech heavyweights suffered a shellacking that had market veterans recalling the dot-com bust in the early 2000s.

“You have a tug of war,” said Dan Suzuki, deputy chief investment officer at Richard Bernstein Advisors LLC (RBA), in a phone interview.

For the technology sector, particularly the megacap names, earnings were a major drag on performance. For everything else, the market was short-term oversold at the same time optimism was building over expectations the Federal Reserve and other major global central banks will be less aggressive in tightening monetary policy in the future, he said.

Read: Market expectations start to shift in direction of slower pace of rate hikes by Fed

What’s telling is that the interest-rate sensitive tech sector would usually be expected to benefit from a moderation of expectations for tighter monetary policy, said Suzuki, who contends that tech stocks are likely in for a long period of underperformance versus their peers after leading the market higher over the last 12 years, a performance capped by soaring gains following the onset of COVID-19 pandemic in 2020.

RBA has been arguing that there was “a major bubble within major portions of the equity market for over a year now,” Suzuki said. “We think this is the process of the bubble deflating and we think there’s probably further to go.”

The Dow

DJIA,

+2.59%

surged nearly 830 points, or 2.6%, on Friday to end at a two-month high and log a weekly gain of more than 5%. The blue-chip gauge’s October gain was 14.4% through Friday, which would mark its strongest monthly gain since January 1976 and its biggest October rise on record if it holds through Monday’s close, according to Dow Jones Market Data.

While it was a tough week for many of Big Tech’s biggest beasts, the tech-heavy Nasdaq Composite

COMP,

-8.39%

and tech-related sectors bounced sharply on Friday. The tech-heavy Nasdaq swung to a weekly gain of more than 2%, while the S&P 500

SPX,

+2.46%

rose nearly 4% for the week.

Big Tech companies lost more than $255 billion in market capitalization in the past week. Apple Inc.

AAPL,

+7.56%

escaped the carnage, rallying Friday as investors appeared okay with a mixed earnings report. A parade of disappointing earnings sank shares of Facebook parent Meta Platforms Inc.

META,

+1.29%,

Google parent Alphabet Inc.

GOOG,

+4.30%

GOOGL,

+4.41%,

Amazon.com Inc.

AMZN,

-6.80%

and Microsoft

MSFT,

+4.02%.

Mark Hulbert: Technology stocks tumble — this is how you will know when to buy them again

Together, the five companies have lost a combined $3 trillion in market capitalization this year, according to Dow Jones Market Data.

Opinion: A $3 trillion loss: Big Tech’s horrible year is getting worse

Aggressive interest rate increases by the Fed and other major central banks have punished tech and other growth stocks the most this year, as their value is based on expectations for earnings and cash flow far into the future. The accompanying rise in yields on Treasurys, which are viewed as risk-free, raises the opportunity cost of holding riskier assets like stocks. And the further out those expected earnings stretch, the bigger the hit.

Excessive liquidity — a key ingredient in any bubble — has also contributed to tech weakness, said RBA’s Suzuki.

And now investors see an emerging risk to Big Tech earnings from an overall slowdown in economic growth, Suzuki said.

“A lot of people have the notion that these are secular growth stocks and therefore immune to the ups and downs of the overall economy — that’s not empirically true at all if you look at the history of profits for these stocks,” he said.

Tech’s outperformance during the COVID-inspired recession may have given investors a false impression, with the sector benefiting from unique circumstances that saw households and businesses become more reliant on technology at a time when incomes were surging due to fiscal stimulus from the government. In a typical slowdown, tech profits tend to be very economically sensitive, he said.

The Fed’s policy meeting will be the main event in the week ahead. While investors and economists overwhelmingly expect policy makers to deliver another supersize 75 basis point, or 0.75 percentage point, rate increase when the two-day gathering ends on Wednesday, expectations are mounting for Chairman Jerome Powell to indicate a smaller December may be on the table.

However, all three major indexes remain in bear markets, so the question for investors is whether the bounce this week will survive if Powell fails to signal a downshift in expectations for rate rises next week.

See: Another Fed jumbo rate hike is expected next week and then life gets difficult for Powell

Those expectations helped power the Dow’s big gains over the past week, alongside solid earnings from a number of components, including global economic bellwether Caterpillar Inc.

CAT,

+3.39%.

Overall, the Dow benefited because it’s “very tech-light, and it’s very heavy in energy and industrials, and those have been the winners,” Art Hogan, chief market strategist at B. Riley Wealth Management told MarketWatch’s Joseph Adinolfi on Friday. “The Dow just has more of the winners embedded in it and that has been the secret to its success.”

Meanwhile, the outperformance of the Invesco S&P 500 Equal Weight ETF

RSP,

+2.08%,

up 5.5% over the week, versus the market-cap-weighted SPDR S&P 500 ETF Trust

SPY,

+2.38%,

underscored that while tech may be vulnerable to more declines, “traditional parts of the economy, including sectors that trade at a lower valuation, are proving resilient since the broad markets bounced nearly two weeks ago,” said Tom Essaye, founder of Sevens Report Research, in a Friday note.

“Stepping back, this market and the economy more broadly are starting to remind me of the 2000-2002 setup, where extreme tech weakness weighed on the major indices, but more traditional parts of the market and the economy performed better,” he wrote.

Suzuki said investors should remember that “bear markets always signal a change of leadership” and that means tech won’t be taking the reins when the next bull market begins.

“You can’t debate that we’ve already got a signal and the signal is telling up that next cycle not going to look anything like the last 12 years,” he said.

Some investors are on edge that the Federal Reserve may be overtightening monetary policy in its bid to tame hot inflation, as markets look ahead to a reading this coming week from the Fed’s preferred gauge of the cost of living in the U.S.

“Fed officials have been scrambling to scare investors almost every day recently in speeches declaring that they will continue to raise the federal funds rate,” the central bank’s benchmark interest rate, “until inflation breaks,” said Yardeni Research in a note Friday. The note suggests they went “trick-or-treating” before Halloween as they’ve now entered their “blackout period” ending the day after the conclusion of their November 1-2 policy meeting.

“The mounting fear is that something else will break along the way, like the entire U.S. Treasury bond market,” Yardeni said.

Treasury yields have recently soared as the Fed lifts its benchmark interest rate, pressuring the stock market. On Friday, their rapid ascent paused, as investors digested reports suggesting the Fed may debate slightly slowing aggressive rate hikes late this year.

Stocks jumped sharply Friday while the market weighed what was seen as a potential start of a shift in Fed policy, even as the central bank appeared set to continue a path of large rate increases this year to curb soaring inflation.

The stock market’s reaction to The Wall Street Journal’s report that the central bank appears set to raise the fed funds rate by three-quarters of a percentage point next month – and that Fed officials may debate whether to hike by a half percentage point in December — seemed overly enthusiastic to Anthony Saglimbene, chief market strategist at Ameriprise Financial.

“It’s wishful thinking” that the Fed is heading toward a pause in rate hikes, as they’ll probably leave future rate hikes “on the table,” he said in a phone interview.

“I think they painted themselves into a corner when they left interest rates at zero all last year” while buying bonds under so-called quantitative easing, said Saglimbene. As long as high inflation remains sticky, the Fed will probably keep raising rates while recognizing those hikes operate with a lag — and could do “more damage than they want to” in trying to cool the economy.

“Something in the economy may break in the process,” he said. “That’s the risk that we find ourselves in.”

‘Debacle’

Higher interest rates mean it costs more for companies and consumers to borrow, slowing economic growth amid heightened fears the U.S. faces a potential recession next year, according to Saglimbene. Unemployment may rise as a result of the Fed’s aggressive rate hikes, he said, while “dislocations in currency and bond markets” could emerge.

U.S. investors have seen such financial-market cracks abroad.

The Bank of England recently made a surprise intervention in the U.K. bond market after yields on its government debt spiked and the British pound sank amid concerns over a tax cut plan that surfaced as Britain’s central bank was tightening monetary policy to curb high inflation. Prime minister Liz Truss stepped down in the wake of the chaos, just weeks after taking the top job, saying she would leave as soon as the Conservative party holds a contest to replace her.

“The experiment’s over, if you will,” said JJ Kinahan, chief executive officer of IG Group North America, the parent of online brokerage tastyworks, in a phone interview. “So now we’re going to get a different leader,” he said. “Normally, you wouldn’t be happy about that, but since the day she came, her policies have been pretty poorly received.”

Meanwhile, the U.S. Treasury market is “fragile” and “vulnerable to shock,” strategists at Bank of America warned in a BofA Global Research report dated Oct. 20. They expressed concern that the Treasury market “may be one shock away from market functioning challenges,” pointing to deteriorated liquidity amid weak demand and “elevated investor risk aversion.”

Read: ‘Fragile’ Treasury market is at risk of ‘large scale forced selling’ or surprise that leads to breakdown, BofA says

“The fear is that a debacle like the recent one in the U.K. bond market could happen in the U.S.,” Yardeni said, in its note Friday.

“While anything seems possible these days, especially scary scenarios, we would like to point out that even as the Fed is withdrawing liquidity” by raising the fed funds rate and continuing quantitative tightening, the U.S. is a safe haven amid challenging times globally, the firm said. In other words, the notion that “there is no alternative country” in which to invest other than the U.S., may provide liquidity to the domestic bond market, according to its note.

YARDENI RESEARCH NOTE DATED OCT. 21, 2022

“I just don’t think this economy works” if the yield on the 10-year Treasury

TMUBMUSD10Y,

4.228%

note starts to approach anywhere close to 5%, said Rhys Williams, chief strategist at Spouting Rock Asset Management, by phone.

Ten-year Treasury yields dipped slightly more than one basis point to 4.212% on Friday, after climbing Thursday to their highest rate since June 17, 2008 based on 3 p.m. Eastern time levels, according to Dow Jones Market Data.

Williams said he worries that rising financing rates in the housing and auto markets will pinch consumers, leading to slower sales in those markets.

Read: Why the housing market should brace for double-digit mortgage rates in 2023

“The market has more or less priced in a mild recession,” said Williams. If the Fed were to keep tightening, “without paying any attention to what’s going on in the real world” while being “maniacally focused on unemployment rates,” there’d be “a very big recession,” he said.

Investors are anticipating that the Fed’s path of unusually large rate hikes this year will eventually lead to a softer labor market, dampening demand in the economy under its effort to curb soaring inflation. But the labor market has so far remained strong, with an historically low unemployment rate of 3.5%.

George Catrambone, head of Americas trading at DWS Group, said in a phone interview that he’s “fairly worried” about the Fed potentially overtightening monetary policy, or raising rates too much too fast.

The central bank “has told us that they are data dependent,” he said, but expressed concerns it’s relying on data that’s “backward-looking by at least a month,” he said.

The unemployment rate, for example, is a lagging economic indicator. The shelter component of the consumer-price index, a measure of U.S. inflation, is “sticky, but also particularly lagging,” said Catrambone.

At the end of this upcoming week, investors will get a reading from the personal-consumption-expenditures-price index, the Fed’s preferred inflation gauge, for September. The so-called PCE data will be released before the U.S. stock market opens on Oct. 28.

Meanwhile, corporate earnings results, which have started being reported for the third quarter, are also “backward-looking,” said Catrambone. And the U.S. dollar, which has soared as the Fed raises rates, is creating “headwinds” for U.S. companies with multinational businesses.

Read: Stock-market investors brace for busiest week of earnings season. Here’s how it stacks up so far.

“Because of the lag that the Fed is operating under, you’re not going to know until it’s too late that you’ve gone too far,” said Catrambone. “This is what happens when you’re moving with such speed but also such size, he said, referencing the central bank’s string of large rate hikes in 2022.

“It’s a lot easier to tiptoe around when you’re raising rates at 25 basis points at a time,” said Catrambone.

‘Tightrope’

In the U.S., the Fed is on a “tightrope” as it risks over tightening monetary policy, according to IG’s Kinahan. “We haven’t seen the full effect of what the Fed has done,” he said.

While the labor market appears strong for now, the Fed is tightening into a slowing economy. For example, existing home sales have fallen as mortgage rates climb, while the Institute for Supply Management’s manufacturing survey, a barometer of American factories, fell to a 28-month low of 50.9% in September.

Also, trouble in financial markets may show up unexpectedly as a ripple effect of the Fed’s monetary tightening, warned Spouting Rock’s Williams. “Anytime the Fed raises rates this quickly, that’s when the water goes out and you find out who’s got the bathing suit” — or not, he said.

“You just don’t know who is overlevered,” he said, raising concern over the potential for illiquidity blowups. “You only know that when you get that margin call.”

U.S. stocks ended sharply higher Friday, with the S&P 500

SPX,

+2.37%,

Dow Jones Industrial Average

DJIA,

+2.47%

and Nasdaq Composite each scoring their biggest weekly percentage gains since June, according to Dow Jones Market Data.

Still, U.S. equities are in a bear market.

“We’ve been advising our advisors and clients to remain cautious through the rest of this year,” leaning on quality assets while staying focused on the U.S. and considering defensive areas such as healthcare that can help mitigate risk, said Ameriprise’s Saglimbene. “I think volatility is going to be high.”

Stocks ended the first full week of the earnings season on a strong note Friday, pushing the Dow Jones Industrial Average

DJIA,

+2.47%,

S&P 500

SPX,

+2.37%

and Nasdaq Composite

COMP,

-0.81%

to their strongest weekly gains since June. It gets more hectic in the week ahead, with 165 S&P 500 companies, including 12 Dow components, due to report results, according to FactSet, making it the busiest week of the season.

The bar for earnings was set high last year as the global economy reopened from its pandemic-induced state. “Fast forward to this year, and earnings are facing tougher comparisons on a year-over-year basis. Add in the elevated risk of a recession, still hot inflation, and an aggressive Fed tightening cycle, and it is of little surprise that the sentiment surrounding the current 3Q22 earnings season is cautious,” said Larry Adam, chief investment officer for the private client group at Raymond James, in a Friday note.

“We have reason to believe the 3Q22 earnings season will be better than feared and could become a positive catalyst for equities just as the 2Q22 results were,” he wrote.

Read: Stocks are attempting a bounce as earnings season begins. Here’s what it will take for the gains to stick.

Better-than-feared earnings were credited with helping to fuel a stock-market rally from late June to early August, with equities bouncing back sharply from what were then 2020 lows before succumbing to fresh rounds of selling that, by the end of September, took the S&P 500 to its lowest close since November 2020.

While earnings weren’t the only factor in the past week’s gains, they probably didn’t hurt.

The number of S&P 500 companies reporting positive earnings surprises and the magnitude of these earnings surprises increased over the past week, noted John Butters, senior earnings analyst at FactSet, in a Friday note.

Even with that improvement, however, earnings beats are still running below long-term averages.

Through Friday, 20% of the companies in the S&P 500 had reported third-quarter results. Of these companies, 72% reported actual earnings per share, or EPS, above estimates, which is below the 5-year average of 77% and below the 10-year average of 73%, Butters said. In aggregate, companies are reporting earnings that are 2.3% above estimates, which is below the 5-year average of 8.7% and below the 10-year average of 6.5%.

Meanwhile, the blended-earnings growth rate, which combines actual results for companies that have reported with estimated results for companies that have yet to report, rose to 1.5% compared with 1.3% at the end of last week, but it was still below the estimated earnings growth rate at the end of the quarter at 2.8%, he said. And both the number and magnitude of positive earnings surprises are below their 5-year and 10-year averages. On a year-over-year basis, the S&P 500 is reporting its lowest earnings growth since the third quarter of 2020, according to Butters.

The blended-revenue growth rate for the third quarter was 8.5%, compared with a revenue growth rate of 8.4% last week and a revenue growth rate of 8.7% at the end of the third quarter.

Next week’s lineup accounts for over 30% of the S&P 500’s market capitalization, Adam said. And with the tech sector accounting for around 20% of the index’s earnings, reports from Visa Inc.

V,

+1.68%,

Google parent Alphabet Inc.

GOOG,

+0.94%

GOOGL,

+1.16%,

Microsoft Corp.

MSFT,

+2.53%,

Amazon.com Inc.

AMZN,

+3.53%

and Apple Inc.

AAPL,

+2.71%

will be closely watched.

Away from the backward-looking numbers, guidance from executives on the path ahead will be crucial against a backdrop of recession fears, Adam wrote, noting that so far guidance has remained resilient, with the net percentage of companies raising rather than lowering their outlook remaining positive.

“For example, the ‘Summer of Revenge Travel’ was known to benefit the airlines, but commentary from United

UAL,

+3.56%,

American

AAL,

+1.86%

and Delta Airlines

DAL,

+1.34%

suggests demand remains strong for the months ahead and into 2023. Ultimately, the broader based and better the forward guidance, the higher the confidence in our $215 S&P 500 earnings target for 2023,” Adam said.

The soaring U.S. dollar

DXY,

-0.89%,

which remains not far off a two-decade high set at the end of last month, also remains a concern.

See: How the strong dollar can affect your financial health

“While the degree of the impact depends on the blend of costs versus sales overseas and how much of the currency risk is hedged, a stronger dollar typically impairs earnings,” Adam wrote.

With little or no progress made on bringing inflation down, the Federal Reserve needs to continue raising interest rates, Cleveland Fed President Loretta Mester said Tuesday.

“At some point, you know, as inflation comes down, them my risk calculation will shift as well and we will want to either slow the rate increases, hold for some time and assess the cumulative impact on what we’ve done,” Mester told reporters after a speech to the Economic Club of New York.

“But at this point, my concerns lie more on – we haven’t seen progress on inflation , we have seen some moderation- but to my mind it means we still have to go a little bit further,” Mester said.

In her speech, the Cleveland Fed president said the central bank needed to be wary of wishful thinking about inflation that would lead the central bank to pause or reverse course prematurely.

“Given current economic conditions and the outlook, in my view, at the point the larger risks come from tightening too little and allowing very high inflation to persist and become embedded in the economy,” Mester said.

She said she thinks inflation will be more persistent than some of her colleagues.

As a result, her preferred path for the Fed’s benchmark rate is slightly higher than the median forecast of the Fed’s “dot-plot,” which points to rates getting to a range of 4.5%-4.75% by next year.

Mester, who is a voting member of the Fed’s interest-rate committee this year, repeated she doesn’t expect any cuts in the Fed’s benchmark rate next year. She stressed that this forecast is based on her current reading of the economy and she will adjust her views based on the economic and financial information for the outlook and the risks around the outlook.

Opinion: Fed is missing signals from leading inflation indicators

Mester said she doesn’t rely solely on government data on inflation because some of it was backward looking. She said supplements her research with talks with business contacts about their price-setting plans and uses some economic models.

The Fed is also helped by some real-time data, she added.

“I don’t see the signs I’d like to see on the inflation,” she added,

Mester said she didn’t see any “big, pending risks” in terms of financial stability concerns.

“There is no evidence that there is disorderly market functioning going on at present,” she said.

U.S. stocks were mixed on Tuesday afternoon with the Dow Jones Industrial Average

DJIA,

+0.12%

up a bit but the S&P 500 in negative territory. The yield on the 10-year Treasury note

TMUBMUSD10Y,

3.936%

inched up to 3.9%

A Wall Street hat trick may not be on the cards, with stocks in the red for Wednesday.

A two-day rally was never a guaranteed exit out of the bear woods anyway, as some say signs of a durable bottom are still missing.

Enter our call of the day, from the chief market technician at TheoTrade, Jeffrey Bierman, who has made a string of prescient calls on what has been a roller coaster year for the index thus far. He’s also a professor of finance at Loyola University Chicago and DePaul University.

Bierman, who uses quant and fundamental analysis to determine market direction, sees the S&P 500

SPX,

-1.62%

finishing the year between 4,000 and 4,200, maybe around 4,135. “Fourth-quarter seasonality favors bulls following a weak third quarter. Not to mention most stocks are priced for no growth,” he told MarketWatch in a Monday interview.

In December 2021, he forecast the S&P 500 might see a 20% decline within six months, toward 3,900 — it hit 3,930 in early May. In June, he forecast a rally and recovery to 4,300 — the index hit 4,315 by mid-August.

Speaking to MarketWatch on Aug. 25, Bierman saw a retest of around 3,600 for the index, citing an often rough September for stocks. It closed out last month at a new 2022 low of 3,585.

“I think we’re going to end up for the quarter. [The market is] deeply oversold and some stocks are completely mispriced in terms of their valuation metrics,” said Bierman, who is looking squarely at retail and technology sectors.

“The valuations on half the chip stocks are trading below a multiple of seven. I’ve never seen that ever…but what that means is when the semiconductor sector comes back, the multiple expansion is gonna be like a volcanic eruption to the upside,” he said of the sector known for its boom/bust cycles.

For example, he owns Intel

INTC,

-2.53%,

which hit a five-year low on Friday. Eventually, the company that has invested $20 billion in a new U.S. plant will come roaring back alongside rivals like Advanced Micro

AMD,

-4.65%.

“People will look back on this and go ‘Oh, my God, I can’t believe Intel was at five times earnings,’ which is insanity for this stock.”

For the S&P 500 as a whole next twelve months price/earnings is currently 16.13 times, so Intel’s would be less than half of the broader index, according to FactSet

As for retail, he’s been looking at Urban Outfitters

URBN,

-1.06%,

Macy’s

M,

-1.94%

and Nordstrom

JWN,

-0.67%,

all places where millennials don’t shop, but the middle class does, with the all-important holiday shopping period dead ahead.

“There are 100,000 people being hired to work part time at these companies, and their margins are not coming down at all,” with no markdowns and decent sales, he said, noting those companies are being priced at a multiple of 5 times forward earnings.

“It means that you don’t think that Macy’s can put together for the Christmas quarter a comparative quarter, year over year of greater than 5%? If you don’t then don’t buy it, but I do,” said Bierman. “That’s why I’m willing to stick my neck out and buy these things. I bought Abercrombie & Fitch

ANF,

-3.78%

at 10 times earnings…I’ve never seen it that low.”

For those who aren’t comfortable picking stocks, he says they can still get exposure through exchange-traded funds, such as SPDR S&P Retail

XRT,

-2.58%

or the Technology Select Sector SPDR ETF

XLK,

-1.70%.

Bierman adds that investors need to be careful not to be overly concentrated in the top stocks, given “10 stocks accounted for 45% of the Nasdaq and the fact that 25% of the S&P almost accounted for about 50% of the S&P movement.”

“Everbody’s concentrated in 10 stocks that can still fall another 30% or 40%, like Apple and Microsoft. The idea of concentration risk is that everybody owns Apple, everybody owns Amazon,” he said.

And that could force the hand of passive and active managers heavily invested in those big names, driving a 10% drop for markets that “washes away all other stocks.”

The markets

Stocks

DJIA,

-1.21%

SPX,

-1.62%

COMP,

-2.19%

are in the red, and bond yields

TMUBMUSD10Y,

3.783%

TMUBMUSD02Y,

4.199%

are up, along with the dollar

DXYN, .

Silver

SI00,

-5.00%

is retracing some of this week’s big gains, and bitcoin

BTCUSD,

-2.62%

is also off, trading at just over $20,000. Hong Kong stocks

HSI,

+5.90%

surged 6% in a catch-up move following a holiday. New Zealand’s central bank hiked rates a half point, the fifth increase in a row.

The buzz

Oil prices

CL.1,

-0.02%

BRN00,

+0.28%

are flat as OPEC+ reportedly agreed to cut oil production by 2 million barrels a day. Some say don’t be too impressed by any output reduction.

Amazon

AMZN,

-2.34%

will reportedly freeze corporate hires in its retail business for the remainder of 2022.

Mortgage applications fell to the lowest pace in 25 years in the latest week.

The ADP private-sector payrolls report showed 208,000 jobs added in September. The trade deficit narrowed, which should be good news for third-quarter GDP. The Institute for Supply Management’s services index is due at 10 a.m. Atlanta Fed President Raphael Bostic will also speak.

Expect the spotlight to stay on Twitter

TWTR,

-2.53%

after Tesla

TSLA,

-5.16%

CEO Elon Musk committed to the $44 billion deal. But will it feel like a win once he owns it?

Plus: Elon Musk’s legal battle with Twitter may be over, but his war with the SEC continues

EU countries agreed to impose new sanctions on Russia after the illegal annexation of four Ukraine regions. Those moves will include an expected price cap on Russian oil.

South Korea’s missile fired in response to North Korea’s weapon launch over Japan, crashed and burned.

Best of the web

Russians fleeing Putin’s mobilization are finding haven in poor, remote countries.

Consumers are throwing away perfectly good food because of ‘best before’ labels.

The CEO of an election software company has been arrested on accusations of ID theft.

Top tickers

These were the top-searched tickers on MarketWatch as of 6 a.m. Eastern:

Ticker

Security name

TSLA,

-5.16%

Tesla

GME,

-7.59%

GameStop

AMC,

-9.56%

AMC Entertainment

TWTR,

-2.53%

Twitter

NIO,

-5.92%

NIO

AAPL,

-1.77%

Apple

APE,

-8.40%

AMC Entertainment preferred shares

BBBY,

-8.52%

Bed Bath & Beyond

AMZN,

-2.34%

Amazon

DWAC,

-0.64%

Digital World Acquisition Corp.

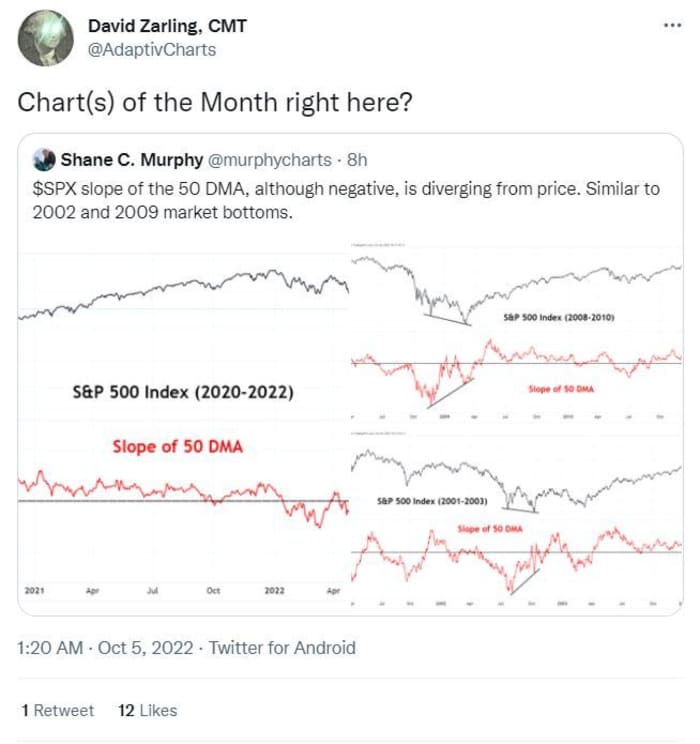

The chart

More market-bottom talk:

Twitter

Random reads

All about the investment manager who caught Yankees’ superstar Aaron Judge’s record-breaking home run.

An iPhone in a 162-year old painting? The internet is stumped.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Listen to the Best New Ideas in Money podcast with MarketWatch reporter Charles Passy and economist Stephanie Kelton

Hashtags about a stock-market crash may be trending on Twitter, but the selloff that has sent U.S. equities into a bear market has been relatively orderly, say market professionals. But it’s likely to get more volatile — and painful — before the market stabilizes.

It was indeed a white-knuckle ride for investors Friday as the Dow Jones Industrial Average

DJIA,

-1.62%

plunged more than 800 points and the S&P 500 index

SPX,

-1.72%

traded below its 2022 closing low from mid-June before trimming losses ahead of the bell. The Dow sank to its lowest close since November 2020, leaving it on the brink of joining the S&P 500 in a bear market.

Why is the stock market falling?

Rising interest rates are the main culprit. The Federal Reserve is raising its benchmark interest rate in historically big increments — and plans to keep raising them — as it attempts to pull inflation back to its 2% target. As a result, Treasury yields have soared. That means investors can earn more than in the past by parking money in government paper, raising the opportunity cost of investing in riskier assets like stocks, corporate bonds, commodities or real estate.

Historically low interest rates and ample liquidity provided by the Fed and other central banks in the wake of the 2008 financial crisis and the 2020 pandemic helped drive demand for riskier assets such as stocks.

That unwinding is part of the reason why the selloff, which isn’t limited to stocks, feels so harsh, said Michael Arone, chief investment strategist for the SPDR business at State Street Global Advisors.

“They’ve struggled with the idea that stocks are down, bonds are down, real estate is starting to suffer. From my viewpoint it’s the fact that interest rates are rising so rapidly, resulting in declines across the board and volatility across the board,” he said, in a phone interview.

How bad is it?

The S&P 500 index ended Friday down 23% from its record close of 4,796.56 hit on Jan. 3 this year.

That’s a hefty pullback, but it’s not out of the ordinary. In fact, it’s not even as bad as the typical bear-market retreat. Analysts at Wells Fargo studied 11 past S&P 500 bear markets since World War II and found that the downdrafts, on average, lasted 16 months and produced a negative 35.1% bear-market return.

A decline of 20% or more (a widely used definition of a bear market) has occurred in 9 of the 42 years going back to 1980, or about once every five years, said Brad McMillan, chief investment officer for Commonwealth Financial Network, in a note.

“Significant declines are a regular and recurring feature of the stock market,” he wrote. “In that context, this one is no different. And since it is no different, then like every other decline, we can reasonably expect the markets to bounce back at some point.”

What’s ahead?

Many market veterans are bracing for further volatility. The Fed and its chairman, Jerome Powell, signaled after its September meeting that policy makers intend to keep raising interest rates aggressively into next year and to not cut them until inflation has fallen. Powell has warned that getting inflation under control will be painful, requiring a period of below-trend economic growth and rising unemployment.

Many economists contend the Fed can’t whip inflation without sinking the economy into a recession. Powell has signaled that a harsh downturn can’t be ruled out.

“Until we get clarity on where the Fed is likely to end” its rate-hiking cycle, “I would expect to get more volatility,” Arone said.

Meanwhile, there may be more shoes to drop. Third-quarter corporate earnings reporting season, which gets under way next month, could provide another source of downside pressure on stock prices, analysts said.

“We’re of the view that 2023 earnings estimates have to continue to decline,” wrote Ryan Grabinski, investment strategist at Strategas, in a note. “We have our 2023 recession odds at about 50% right now, and in a recession, earnings decline by an average of around 30%. Even with some extreme scenarios—like the 2008 financial crisis when earnings fell 90% — the median decline is still 24%.”

The consensus 2023 earnings estimate has only come down 3.3% from its June highs, he said, “and we think those estimates will be revised lower, especially if the odds of a 2023 recession increase from here,” Grabinski wrote.

What to do?

Arone said sticking with high quality value stocks that pay dividends will help investors weather the storm, as they tend to do better during periods of volatility. Investors can also look to move closer to historical benchmark weightings, using the benefits of diversification to protect their portfolio while waiting for opportunities to put money to work in riskier parts of the market.

But investors need to think differently about their portfolios as the Fed moves from the era of easy money to a period of higher interest rates and as quantitative easing gives way to quantitative tightening, with the Fed shrinking its balance sheet.

“Investors need to pivot to thinking about what might benefit from tighter monetary policy,” such as value stocks, small-cap stocks and bonds with shorter maturities, he said.

How will it end?

Some market watchers argue that while investors have suffered, the sort of full-throttle capitulation that typically marks market bottoms has yet to materialize, though Friday’s selloff at times carried a whiff of panic.

The Fed’s aggressive interest rate rises have stirred market volatility, but haven’t caused a break in the credit markets or elsewhere that would give policy makers pause.

Meanwhile, the U.S. dollar remains on a rampage, soaring over the past week to multidecade highs versus major rivals in a move driven by the Fed’s policy stance and the dollar’s status as a safe place to park.

A break in the dollar’s relentless rally “would suggest to me that the tightening cycle and some of the fear — because the dollar is a haven — is starting to subside,” Arone said. “We’re not seeing that yet.”

Ford Motor Co. shares dropped more than 4% in the extended session Monday after the company said inflation and parts shortages will leave it with more unfinished vehicles than it had expected, reminding Wall Street supply-chain snags are far from over for auto makers.

Ford

F,

+1.43%

said it expects to have between 40,000 and 45,000 vehicles in inventory at the end of the third quarter “lacking certain parts presently in short supply.”

The auto maker also said that based on its recent negotiations, payments to suppliers will run about $1 billion higher than expected for the quarter, thanks to inflation. The company reaffirmed its outlook for the year, however.

Ford’s warning “is evidence that auto parts shortages and supply-chain issues are still ongoing,” CFRA analyst Garrett Nelson told MarketWatch.

Many investors had started to believe “these problems were in the rearview mirror with inventories starting to recover from the record lows of the last year or so,” Nelson said.

The unfinished vehicles include high-demand, high-margin models of popular trucks and SUVs, Ford said. That will cause some shipments and revenue to shift to the fourth quarter.

“Ironically, Ford may have become a victim of its own success in that its recent U.S. sales growth has outperformed peers by a wide margin,” Nelson said. Its third-quarter production “apparently wasn’t able to keep pace with demand.”

Ford reiterated expectations of full-year 2022 adjusted earnings before interest and taxes of between $11.5 billion and $12.5 billion, despite the shortages and the higher payments to suppliers, it said.

Ford called for third-quarter adjusted EBIT of between $1.4 billion and $1.7 billion.

Shares of Ford ended the regular trading day up 1.4%. The company has embarked on a reorganization to pivot to electric vehicles, and last month confirmed layoffs in connection with its new structure.

Ford is slated to report third-quarter financial results on Oct. 26, when it said it expects to “provide more dimension about expectations for full-year performance.”

Analysts polled by FactSet expect the auto maker to report adjusted earnings of 51 cents a share, which would match the third-quarter 2021 adjusted EPS, on revenue of $38.8 billion.

The quarterly sales would compare with $35.7 billion in revenue in the year-ago period.

Shares of Ford slid 4.4% after hours, and have lost 28% so far this year, compared with losses of 18% for the S&P 500 index

SPX,

+0.69%.

The news comes a week after FedEx Corp.

FDX,

+1.17%

roiled markets and raised fears of an economic slowdown by withdrawing its outlook for the year and warning that the year was likely to become worse for the business.