Shell made a recordprofit of almost $40 billion in 2022, more than double what it raked in the previous year after oil and gas prices soared following Russia’s invasion of Ukraine.

Europe’s largest oil company by revenue reported adjusted full-year earnings of $39.9 billion on Thursday — more than double the $19.3 billion it posted in 2021 — driven by a strong performance in its gas trading business.The company’s stock was up 1.7% in London.

The company reported $9.8 billion in profit in the fourth quarter. Just over 40% of Shell’s full-year earnings came from its integrated gas business, which includes liquified natural gas trading operations.

Shell CEO Wael Sawan said the results “demonstrate the strength of Shell’s differentiated portfolio, as well as our capacity to deliver vital energy to our customers in a volatile world.”

The earnings are the latest in a series of record-setting results by the world’s biggest energy companies, which have enjoyed bumper profits off the back of soaring oil and gas prices.

ExxonMobil this week posted record full-year earnings of $59.1 billion. Last month, Chevron

(CVX) reported a record full-year profit of $36.5 billion.

That has led to renewed calls for higher taxation. Governments in the European Union and the United Kingdom have already imposed windfall taxes on oil company profits, with the proceeds used to help households struggling with rising energy bills.

Shell said it expected to pay an additional $2.3 billion in tax related to the EU windfall tax and the UK energy profits levy. The company paid $13 billion in tax globally in 2022.

Shell

(RDSA) also announced another $4 billion share buyback program and confirmed it would lift its dividend per share by 15% for the fourth quarter.

Meta shares jumped on Wednesday after the social media company’s sales for the final quarter of 2022 came in better than expected and it authorised an additional $40bn in share buybacks.

Meta, which owns Facebook, Instagram and WhatsApp, reported revenues of $32.2bn, a 4 per cent decline from the year before but at the top end of its guidance. It was also slightly above analysts’ estimates of a drop to $31.7bn, according to S&P Capital IQ.

The company also announced an additional $40bn for share buybacks. Meta shares jumped about 19 per cent in after-hours trading. If that gain holds, it would add about $76bn to its market value, according to Bloomberg data.

The results present a rosier picture for Meta, which has been squeezed over the past year by the economic slowdown that prompted marketers to cut their spending, along with heightened competition from TikTok and challenges in tailoring and measuring ad campaigns following Apple’s privacy changes.

Monthly active users on one or more of its apps rose 4 per cent to 3.74bn in the fourth quarter, while user numbers for the Facebook app specifically rose 2 per cent to 2.96bn.

However, its profits took a substantial knock in the quarter due to billions of dollars of restructuring costs as it seeks to wrestle its finances under control rising impatience from investors over its costly metaverse bet.

Net income in the fourth quarter dropped 55 per cent to $4.7bn, compared with consensus estimates for a drop to $6bn. Meta blamed a restructuring cost of $4.2bn in the quarter related to facilities consolidation, job cuts and the cancellation of multiple data centres.

In a call with investors, chief executive Mark Zuckerberg said that his “management theme” for the company in 2023 was “efficiency”.

The company would focus on removing some layers of middle management, cut low-performing projects and deploying artificial intelligence tools to help its engineers be more productive, he said.

“2022 was a challenging year. But I think we ended up having made good progress on our main priorities and setting ourselves up to deliver better results this year, as long as we keep pushing on efficiency,” Zuckerberg added.

Meta, which expanded its headcount rapidly since the start of the coronavirus pandemic, has sought to bring down costs as Wall Street has increasingly questioned its lossmaking efforts to build an avatar-filled digital world known as the metaverse. As with its many other virtual and augmented reality projects, they are not expected to generate returns for many years.

In November, Meta announced its biggest headcount reductions, dismissing 11,000 staffers, or about 13 per cent of total employees. It also introduced other measures such as reducing budgets and employee perks, and shrinking its “real estate footprint”.

On Wednesday, the company forecast revenues for the current quarter of between $26bn-$28.5bn. It also anticipates 2023 expenses in the range of $89bn-$95bn, down from the prior outlook of $94bn-$100bn, due to “slower anticipated growth in payroll expenses and cost of revenue”.

It expects a further $1bn in restructuring charges, down from a previous estimate of $2bn.

Chevron Corp.’s blockbuster $75 billion share buyback has drawn the ire of Joe Biden, whose call for more investment in pumping oil — alongside a new 1% tax on buybacks — doesn’t seem to have done much to steer cash into unloved fossil fuels and away from short-term investor sweeteners. Corporate America spent an estimated $1 trillion on buybacks last year.

European politicians will likely feel similarly irate and helpless as corporate payouts rebound in wartime. Big Oil’s expected $200 billion profit haul — and related buybacks announced by Shell Plc, BP Plc and TotalEnergies SE — only looks like the tip of the iceberg in a region that’s seen profits and payouts jump but where capital spending looks shaky. While windfall taxes have been slapped on the energy sector, expect calls for a buyback tax — which in the US could raise $74 billion over a decade — to grow.

After all, shareholder-friendly splurges are now a trans-Atlantic phenomenon. European companies now buy back more of their market capitalization than US peers: Buybacks reached 27.2 billion euros ($30 billion) and 55.2 billion pounds ($68.4 billion) at top French and UK firms respectively in 2022, according to data from Natixis and AJ Bell. Luxury-goods heavyweight LVMH, defense firm BAE Systems Plc and distiller Diageo Plc are among those joining in; corporations were the biggest buyers of European stocks last year, according to Goldman Sachs Group Inc. strategists.

Buybacks are seen by advocates as a better way to allocate capital when the other options, like mergers or expansion, look less profitable. In the case of Big Oil, that might make sense in a world where the risk premium on fossil-fuel projects has gone up. Likewise, in ESG-unfriendly sectors like defense, or tightly regulated areas like financial services, pressure to compete with other investments means a need to ramp up shareholder sweeteners. And, on balance, it works for them— one index tracking European firms buying back shares is outperforming the broader market.

But the problems start when the size and pace of these payouts eclipse the growth of more socially useful spending like capital investment, research and development or wages. While the push to invest more in supply chains means we are no longer in the capex drought of the 2010s, post-pandemic investment has rebounded more slowly than profits and is likely to stall alongside economic growth this year. Meanwhile, wartime inflation, which has fattened profit margins while squeezing consumers, will remain high — as will pressure to share more of the earnings pie with workers.

The fact that layoffs are mounting also throws a bad light on shareholder bonanzas. Big Tech splashed cash on buybacks last year; now they’re cutting jobs. Salesforce Inc. will spend about as much on restructuring charges as it spent on buying back shares in the third quarter of 2022. For a practice that’s supposedly about efficient capital allocation, repurchasing overvalued shares looks incredibly wasteful. Starbucks Corp.’s halt to buybacks last year also pointed to some business rationale behind investing even in an economic slowdown — such as to defend market share.

Even without succumbing to what’s uncharitably called “Buyback Derangement Syndrome,” there are good reasons to use taxation as a way to nudge behavior in a different direction at a time of stretched government budgets and consumer pocketbooks. The 1% rate seen in the US is little more than a rounding error, and is likely just the start. But UK think tank IPPR estimates its application on FTSE 100 firms would raise 225 million pounds in one year. Already, France is set to see a new flat tax on above-average dividends and buybacks — though, messily, it will come on top of existing levies on stock trades.

The irony of the current situation is that the buyback boom may deflate before generating much in the way of tax revenue. Companies may soon be rewarded by shareholders for sitting on cash or strengthening their balance sheets in an altogether riskier environment. And dividends, while harder to tinker with than buybacks, may end up looking more attractive as a payout.

But if the buybacks keep piling up, at a time when social unrest in Europe is mounting and governments are rolling out clean-tech subsidies, expect Biden’s frustrations to reverberate beyond the White House.

More From Bloomberg Opinion:

• Buy Back, Baby, Buy Back: Elements by Liam Denning

• Biden Is Right to Question Oil Stock Buybacks: Matthew Winkler

• Is Big Tech Safe From Activist Shareholders?: Olson and Hughes

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering digital currencies, the European Union and France. Previously, he was a reporter for Reuters and Forbes.

More stories like this are available on bloomberg.com/opinion

Bitcoin, Ethereum higher, Dogecoin lower early Monday

Cryptocurrency prices were mixed early Monday, with Bitcoin and Etherum higher and Dogecoin trending lower.

At approximately 5:15 a.m. ET, Bitcoin was trading at nearly $16,837 (+0.08%), or higher by $14.

For the week, Bitcoin was trading higher by nearly 0.27%. For the month, the cryptocurrency was lower by nearly 1.8%.

Ethereum was trading at approximately $1,218 (+0.16%), or higher by about $1.9.

For the week, Ethereum was trading higher by slightly more than 2.6%. For the month, it was trading higher by approximately 1.45%.

Dogecoin was trading at $0.075658 (-0.35%), or lower by approximately $0.000248.

For the week, Dogecoin was lower by almost 3.75%. For the month, the crypto was lower by nearly 15.5%.

Gasoline prices hold steady overnight

The price of gasoline held steady over the holiday weekend.

The nationwide price for a gallon of gasoline on Monday held at $3.102, the same price as Sunday, according to AAA. The average price of a gallon of gasoline on Saturday was $3.097.

One week ago, a gallon of gasoline cost $3.142. A month ago, that same gallon of gasoline cost $3.566. A year ago, the price for a gallon of regular gasoline was $3.29.

Gas hit an all-time high of $5.016 on June 14.

Diesel has slipped below $5.00 per gallon to $4.684, but that is still a far cry from the $3.576 of a year ago.

U.S. President Joe Biden gestures as he delivers remarks on the Inflation Reduction Act of 2022 at the White House in Washington, July 28, 2022.

Elizabeth Frantz | Reuters

The new 1% excise tax on corporate stock buybacks — a late addition to President Joe Biden’s sweeping tax, health and climate package — adds a new levy to the controversial practice.

But there are mixed views on how it may affect investors.

The Inflation Reduction Act provision levies a 1% excise tax on the market value of net corporate shares repurchased starting in 2023.

How stock buybacks work

When a profitable public company has excess cash, it can purchase shares of its own stock on the public market or make an offer to shareholders, known as a stock buyback or share repurchase.

It’s a way of returning cash to shareholders, explained Amy Arnott, portfolio strategist at Morningstar, and more widely used than dividends, a portion of company profits regularly sent back to investors.

More from Personal Finance: These are priorities for the nearly $80 billion in IRS funding IRS interest jumps soon. What you’ll get for a missing refund These are the best colleges for financial aid

If overall shares are reduced, stock buybacks may also boost earnings per share, one method of measuring a company’s financial performance.

However, critics have argued buybacks often come with the new issuance of stock options for executives and other employees. Adding new shares can negate some, or all, of share reduction benefits for regular investors from buybacks.

‘Buyback monsters’ drive the trend

With low interest rates boosting profits and values, S&P 500 companies bought back a record $881.7 billion of their own stock in 2021, up from $519.8 billion in 2020, according to S&P Global data.

A significant percentage comes from a handful of so-called “buyback monsters,” with five companies — Apple, Google parent Alphabet, Facebook parent Meta, Microsoft and Bank of America — making up one-quarter of the dollar value of stock buybacks over the past year.

How the 1% tax on stock buybacks may affect investors

While the full impact on the stock market isn’t yet known, experts have mixed opinions on how the provision may affect individual portfolios.

“I don’t think it should have a major impact on investors,” Arnott said. But at the margins, companies with excess cash may be “slightly more likely” to pay dividends than buy back shares, she said.

It’s estimated that a 1% tax on share repurchases may trigger a 1.5% increase in corporate dividend payouts, according to the Tax Policy Center.

And increased dividends may have an unexpected impact, depending on where investors are holding these assets, said Alex Durante, federal tax economist at the Tax Foundation.

“People with taxable accounts may potentially be impacted,” he said.

Of course, the shift from buybacks to dividends may also change the expected tax revenue, Durante added.

The provision is expected to raise about $74 billion over the next decade, according to recent estimates from the Joint Committee on Taxation.

However, since the new law won’t kick in until Jan. 1, 2023, some experts predict companies will accelerate “tax-free” stock buybacks through 2022, especially with stock prices still well below previous values.

General Motors on Friday announced it will resume and boost share repurchases to $5 billion, up from $3.3 billion previously left from the program. And Home Depot on Thursday announced a $15 billion share buyback program.

High prices, margins lift majors to best quarters in history

Exxon earnings surpass previous record set in 2012

July 29 (Reuters) – The two largest U.S. oil companies, Exxon Mobil Corp (XOM.N) and Chevron Corp (CVX.N), posted record revenue on Friday, bolstered by surging crude oil and natural gas prices and following similar results for European majors a day earlier.

The U.S. pair, along with UK-based Shell (SHEL.L) and France’s TotalEnergies (TTEF.PA), combined to earn nearly $51 billion in the most recent quarter, almost double what the group brought in for the year-ago period.

Exxon outpaced its rivals with a $17.9 billion quarterly profit, the most for any international oil major in history.

Register now for FREE unlimited access to Reuters.com

Register

Chevron, Shell and Total ran to catch up with Exxon’s aggressive buyback program, which was kept unaltered.

The four returned a total of $23 billion to shareholders in the quarter, capitalizing on high margins derived from selling oil and gas. The fifth major, BP Plc (BP.L), reports next week. read more

The companies posted strong results in their production units, helped by the surge in benchmark Brent crude oil futures , which averaged around $114 a barrel in the quarter.

High crude oil prices can cut into margins for integrated oil majors, as they also bear the cost of crude used for refined products. However, following Russia’s invasion of Ukraine and numerous shutdowns of refineries worldwide in the wake of the coronavirus pandemic, refining margins exploded in the second quarter, outpacing the gains in crude and adding to earnings.

“The strong second-quarter results reflect a tight global market environment, where demand has recovered to near pre-pandemic levels and supply has attritted,” said Exxon Chief Executive Darren Woods, in a call with analysts. “Growing supply will not happen overnight.”

A combination of file photos shows the logos of five of the largest publicly traded oil companies; BP, Chevron, Exxon Mobil, Royal Dutch Shell, and Total. REUTERS/File Photo

Read More

The results from the majors are sure to draw fire from politicians and consumer advocates who say the oil companies are capitalizing on a global supply shortage to fatten profits and gouge consumers. U.S. President Joe Biden last month said Exxon and others were making “more money than God” at a time when consumer fuel prices surged to records. read more

Earlier this month, Britain passed a 25% windfall tax on oil and gas producers in the North Sea. U.S. lawmakers have discussed a similar idea, though it faces long odds in Congress. read more

A windfall tax does not provide “incentive for increased production, which is really what the world needs today,” said Exxon Chief Financial Officer Kathryn Mikells, in an interview with Reuters.

The companies say they are merely meeting consumer demand, and that prices are a function of global supply issues and lack of investment. The majors have been disciplined with their capital and are resisting ramping up capital expenditure due to pressure from investors who want better returns and resilience during a down cycle.

“In the short term (cash from oil) goes to the balance sheet. There’s no nowhere else for it to go,” Chevron CFO Pierre Breber told Reuters.

Worldwide oil output has been held back by a slow return of barrels to the market from the Organization of the Petroleum Exporting Countries and allies, including Russia, as well as labor and equipment shortages hampering a swifter increase in supply in places like the United States.

Exxon earlier this year more than doubled its projected buyback program to $30 billion through 2022 and 2023. Shell said it would buy back $6 billion in shares in the current quarter, while Chevron boosted its annual buyback plans to a range of $10 billion to $15 billion, up from $5 billion to $10 billion.

Exxon shares were up 4.5% to $96.87 in afternoon trading. Chevron shares rose more than 8% to $163.68.

Register now for FREE unlimited access to Reuters.com

Register

Reporting By Sabrina Valle; writing by David Gaffen; Editing by Kirsten Donovan and Marguerita Choy

Our Standards: The Thomson Reuters Trust Principles.

Q1 was crappy as IPOs imploded, investment banking took a hit, mortgage activity fizzled, other stuff happened.

By Wolf Richter for WOLF STREET.

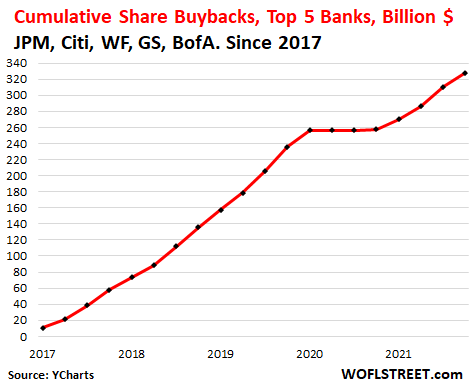

Of the big five banks and bank holding companies in the US by total assets – JP Morgan, Bank of America, Wells Fargo, Citigroup, and Goldman Sachs Group – four reported Q1 earnings so far, and BofA will do so next week. Those earnings reports were marked by a sharp decline in revenues and net income, with all kinds of complications in between. And as a group their shares continued their jagged decline that started in November last year.

The WOLF STREET index of the big five banks’ market capitalization has plunged 23.5% since its recent peak in October 2021 (data via YCharts):

This debacle occurred amid enormous share buybacks. These banks have been regularly featured among the largest share buyback queens in the US, except during the pandemic, when they halted the practice for three quarters.

In the five years from 2017 through 2021, the five banks have incinerated, wasted, and destroyed $328 billion in cash on repurchasing their own shares to prop up their stocks, and now their stocks have nothing to show for it (data via YCharts):

Q1 was crappy as IPOs imploded, mortgage activity fizzled, other stuff happened.

JPMorgan Chase [JPM] kicked off the quarterly banking show on Wednesday morning when it reported that its net income plunged by 42% to $8.3 billion in Q1 compared to Q1 last year. Revenues fell 5% to $30.7 billion, on a 35% plunge in revenues in its investment banking division.

Over the two trading days since the earnings release on Wednesday morning, JP Morgan’s shares tanked 4.1% and are down 25% from their 52-week high in January.

In preparation for rate-hike-induced financial stress on borrowers, it set aside $902 million for loan loss reserves, compared to a $5.2-billion benefit a year ago from releasing loan loss reserves it had set up during the pandemic. And it booked $582 million in net charge-offs, bringing the total credit costs to $1.5 billion.

Its Corporate & Investment Bank profits got hit by a $524 million loss, “driven by funding spread widening as well as credit valuation adjustments relating to both increases in commodities exposures and markdowns of derivatives receivables from Russia-associated counterparties,” it said in the earnings release.

During the earnings call, CEO Jamie Dimon said that the bank sees “significant geopolitical and economic challenges ahead due to high inflation, supply chain issues, and the war in Ukraine.”

Goldman Sachs [GS] reported that revenues plunged 27% in Q1, to $12.9 billion, and net income plunged by 42% to $3.9 billion.

Goldman Sachs share were down just a tad on Thursday, and are down 24.5% from their 52-week high in early November.

Investment banking revenue plunged by 36% to $2.4 billion. It set aside $561 million for credit losses, compared to a benefit of $70 million a year earlier. Asset management revenue collapsed by 88% to $546 million, “primarily reflecting net losses in Equity investments and significantly lower net revenues in Lending and debt investments.”

But at its consumer and wealth management division, revenues grew by 21% to $2.10 billion. And its global market revenues ticked up 4% to $7.87 billion. And yes, given the turmoil in the commodities markets, currency markets, and bond markets, revenues at FICC (Fixed Income, Currency and Commodities) jumped 21% to $4.71 billion.

“The rapidly evolving market environment had a significant effect on client activity as risk intermediation came to the fore and equity issuance came to a near standstill,” the earnings release said.

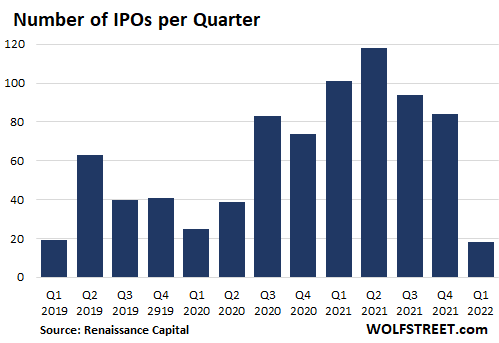

IPOs were crappy all around.

By “equity issuance came to a near standstill,” Goldman is talking about IPOs and SPACs, many of which have imploded spectacularly over the past 12 months. I’m now tracking some of them, including those where Goldman Sachs was the lead underwriter, in the WOLF STREET category of Imploded Stocks.

IPOs are massive fee generators for investment banks. But the collapse of these newly listed stocks has now essentially killed the appetite for new IPOs, which are only fun in a relentless hype-and-hoopla market. In Q1, according to Renaissance Capital, there were only 18 IPOs, including only two in March, down from 118 IPOs in Q2 last year:

Citigroup [C] reported that revenues declined 2.5% to $19.2 billion. Net income plunged 46% to $4.3 billion, on higher operating expenses (+15%) and credit losses of $755 million, compared to a benefit of $2.05 billion a year earlier.

The problem isn’t consumers in the US; they’re doing fine, Citibank said in its earnings release: “We continue to see the health and resilience of the U.S. consumer through our cost of credit and their payment rates. We had good engagement in key drivers such as cards loan growth and vigorous purchase sales growth, so we like where this business is headed.”

The big culprit was investment banking, including IPOs: “the current macro backdrop impacted Investment Banking as we saw a contraction in capital market activity. This remains a key area of investment for us,” Citigroup said.

Its shares rose 1.6% on Thursday but are down 36% from their 52-week high in June.

Wells Fargo [WFC] reported that revenues dropped 5% to $17.6 billion. Net income plunged 21% to $3.67 billion.

One of the culprits was mortgage lending activity, which plunged by 33% in the quarter on surging mortgage rates. “The Federal Reserve has made it clear that it will take actions necessary to reduce inflation and this will certainly reduce economic growth,” and “the war in Ukraine adds additional risk to the downside,” Wells Fargo said in the earnings release.

Shares tanked 4.5% on Thursday and have dropped 23% in two months from their 52-week high in early February.

Bank of America [BAC] will report earnings on Monday. In anticipation, its shares fell 3.2% on Thursday and have plunged 25% from the 52-week high in February.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

That shriek shareholders heard this past week was not only caused by the deep dive in Meta Platforms’ (NASDAQ:FB) market cap after it reported poor earnings and guidance, but an ear-piercing sound as a result of an elevated buyback that left some bewildered.

While the more than $220 billion decline may go down as the largest drop in value in stock market history, market capitalizations fluctuate. However, the company may have made an even more egregious error that has largely gone unnoticed: spending nearly $20 billion in actual cash on share repurchases during the fourth quarter of last year that provided little, if any value.

During the period between last October and December, the Mark Zuckerberg-led Meta (FB) spent $19.2 billion buying back company stock, significantly larger than the $10 billion that Morgan Stanley analyst Brian Nowak estimated. That helped bring down the average diluted share count 3% year-over-year.

According to the company’s annual report filed with the Securities and Exchange Commission, Meta (FB) bought back 21.7 million shares in October at an average price of $326.20, and in November, it purchased 21.6 million more shares, at an average price of $335.09. Lastly, in December, it bought back 14.73 million shares at an average of $329.97.

Altogether, Meta spent the final three months of 2021 buying bac 58 million shares of stock at prices that might not be seen again for months, perhaps years.

To put Meta’s purchases in a little more context, the company’s shares closed at $237.09 on Friday, and are now down 30% since the start of the year.

Share repurchases may be seen as “shareholder friendliness,” as Nowak pointed out – and they usually are, if a company has too much cash on its hands after running its business. But, buying back an elevated amount of stock during a quarter, only to have that period’s results destroy nearly 25% of the company’s value can look like a colossal waste of money.

For context, Meta bought back roughly $24.5 billion in the first three quarters of 2021 combined. So to spend $19.2 billion, or roughly 1.5 times the “record-high repurchase amount” it spent during the third-quarter, according to Evercore ISI analyst Mark Mahaney, is eye opening, to say the least.

The sizable share repurchase amount is given added scrutiny, especially when Meta has conceded that it is being hampered via three different avenues: ByteDance (BDNCE) TikTok is competing with it for attention; Apple’s (NASDAQ:AAPL) iOS changes are hurting the effectiveness of Meta’s advertising, causing it to rebuild its ad infrastructure, according to Chief Operating Officer Sheryl Sandberg; and lastly, its own products, like Reels, are seeing increased engagement over other products, but Reels presently monetizes at a lesser rate than News Feed or Stories.

It’s possible that Meta will be able to overcome these headwinds, though Nowak said that is more likely to occur over the long-term. For the time being, however, Nowak said there could be some “uncertainty around near-term ‘22 ad revenue estimates” as the company focuses on Reels engagement and not monetization.

The nearly $20 billion spent on buybacks could also have been spent in a variety of different manners, including ramping up spending in the metaverse that Zuckerberg has talked so much about, and which caused the company to change course last year after being primarily known as a social network.

Meta is not going to go broke anytime soon, as it ended the quarter with roughly $48 billion in cash and equivalents and generated $12.7 billion in free cash flow. But, J.P. Morgan analyst Mark Mahaney sad there is now a “dramatic fundamentals gap” between Meta and its closest competitor in advertising, Alphabet (NASDAQ:GOOG).

And with Mahaney conceding that “FB is now facing a [Netflix]-like negative inflection point” and the stock “could well be dead money for several months,” it seems foolish of the company to have spent $20 billion on stock buybacks that ultimately, provided little, if any value to shareholders.

Last month, the European Union approved Meta Platform’s (FB) acquisition of Kustomer, a customer-service startup that competes with the likes of Zendesk (NYSE:ZEN).

Shell petrol station logo on Sept. 29, 2021 in Birmingham, United Kingdom.

Mike Kemp | In Pictures | Getty Images

Oil giant Shell on Thursday reported a sharp upswing in full-year profit, beating analyst expectations on rebounding commodity prices.

The British oil major posted adjusted earnings of $19.29 billion for the full-year 2021. That compared with a profit of $4.85 billion the previous year. Analysts polled by Refinitiv had expected full-year 2021 net profit to come in at $17.8 billion.

For the final quarter of 2021, Shell reported adjusted earnings of $6.4 billion.

Shell CEO Ben van Beurden described 2021 as a “momentous year” for the company and said progress made in the last 12 months would enable the firm “to be bolder and move faster.”

“We delivered very strong financial performance in 2021, and our financial strength and discipline underpin the transformation of our company,” he added.

Shell also announced an $8.5 billion share buyback program in the first half of 2022 and said it expects to increase its dividend by 4% to $0.25 per share in the first quarter. Share buybacks totaled $3.5 billion in 2021.

Net debt was reduced to $52.6 billion by the end of 2021, a fall of $23 billion when compared to 2020.

Global oil demand roared back in 2021, with gasoline and diesel use surging as consumers resumed travel and business activity recovered amid the coronavirus pandemic. Indeed, the International Energy Agency has noted mobility indicators remain robust even as Covid-19 is once again causing record infections.

It marks a dramatic shift from 2020 when the oil and gas industry endured a dreadful 12 months by virtually every measure.

Shares of Shell rose 0.6% during early morning deals in London. The firm’s stock price is up over 20% year-to-date but remains below pre-pandemic levels.

Earlier this month, Shell said in a trading update that it would pursue its share buyback program “at pace” after selling its Permian shale business in the U.S. The decision was taken at the company’s first board meeting held in the U.K. at the end of last year.

Shareholders of Shell voted on Dec. 10 to approve plans for the company to simplify its share structure and shift its tax residence to the U.K. from the Netherlands. The oil major also officially dropped “Royal Dutch” from its name, part of its identity since 1907.

Activist pressure

Energy majors are seeking to reassure investors they have gained a more stable footing two years after Covid-19 first shook markets, and as shareholders and activists pile pressure on the firm’s executives to take meaningful climate action.

The world’s largest oil and gas companies have all sought to strengthen their climate targets in recent years, but so far none have given investors confidence their business model is fully aligned to Paris Agreement targets.

To be sure, it is the burning of fossil fuels such as oil and gas that is the chief driver of the climate emergency.

Shell has outlined plans to become a net-zero carbon emissions company by 2050, although Climate Action 100+, the influential investor group, finds the firm’s targets only partially align with the Paris Agreement.

In a landmark ruling last year, a Dutch court ordered the oil major to take much more aggressive action to drive down its carbon emissions. Shell was ruled to be responsible for its own carbon emissions and those of its suppliers, known as Scope 3 emissions, and must reduce its emissions by 45% by 2030.

It was thought to be the first time in history a company has been legally obliged to align its policies with the Paris Agreement.

Shell is appealing the ruling, a move that has been sharply criticized by climate activists.

Companies in the S&P 500 repurchased $234.5 billion in shares during the third quarter, topping the previous record of $223 billion in the fourth quarter of 2018, according to preliminary data from S&P Dow Jones Indices. The wave of share repurchases has helped propel U.S. stock indexes to dozens of records in 2021. The S&P 500 is up 25% this year, notching 67 record closes.

More buybacks are coming. Howard Silverblatt, senior index analyst at S&P Dow Jones Indices, said he projects that S&P 500 buybacks will reach $236 billion in the fourth quarter.

S&P 500 component

Microsoft Corp.

said in September that its board had approved a plan to repurchase up to $60 billion of its stock. Car-rental company

Hertz Global Holdings Inc.

recently said it would buy back as much as $2 billion of its stock, while tech company

Dell Technologies Inc.

is planning a $5 billion share-repurchase program.

Buybacks are just one of the forces behind the stock market’s rally. Asset prices have continued to benefit from the monetary and fiscal support that policy makers put in place to help the economy get through the pandemic. And analysts have consistently underestimated corporate earnings, which are expected to grow 45% in 2021 for companies in the S&P 500.

Investors this week will scrutinize signals out of the Federal Reserve’s two-day policy meeting, where officials may accelerate the process of winding down a bond-buying stimulus program. Central-bank officials could also shed more light on their expectations for interest-rate increases next year.

Microsoft has approved the repurchase of up to $60 billion of its stock. Its HoloLens headset.

Photo:

Thanassis Stavrakis/Associated Press

S&P 500 buybacks plunged from nearly $199 billion in the first quarter of 2020 to just under $89 billion in the second, as companies reeling from the onset of the pandemic moved to conserve cash. Share repurchases increased in each following quarter, approaching $199 billion again in the second quarter of 2021.

Repurchases can support stocks by reducing a company’s share count, boosting its per-share profits. And they can boost investor sentiment by suggesting executives are optimistic about their companies’ prospects and confident in their financial position.

“It’s always comforting to have a management team come in and tell you how undervalued they think their shares are,” said

Anne Wickland,

a portfolio manager at Easterly Investment Partners. “It’s a vote of confidence in the longer-term outlook.”

Her team bought shares of

Lockheed Martin Corp.

in the summer, in part because of the defense company’s share-buyback program and dividend yield. Lockheed shares fell 12% on Oct. 26 after the company reported lower-than-expected quarterly sales and revised its full-year sales forecast lower. Ms. Wickland said she believes the shares are undervalued and continues to like them.

Stock buybacks have come under fire from politicians who say companies should use cash to invest in their businesses instead of supporting their share prices. The version of the $2 trillion education, healthcare and climate spending package that passed the House in November would create a 1% tax on the net value of a company’s stock buybacks.

SHARE YOUR THOUGHTS

What is your reaction to this latest streak of stock buybacks? Join the conversation below.

The Senate hasn’t voted yet, but the buyback tax has so far generated less corporate opposition than the bill’s other tax increases. Strategists at BofA Global Research project that the proposed tax would result in a 0.3% reduction to S&P 500 per-share earnings, assuming that companies didn’t change the amount of stock they repurchase.

Several investors said they don’t believe the tax would have much of an effect on companies’ behavior if it became law. “The 1% tax on buybacks is so low that I don’t think it will impact anything,” said

Olivier Sarfati,

head of equities at wealth-management firm GenTrust.