U.S. stocks and government-bond prices rose on Wednesday, clawing back some of their losses after a stretch of declines.

The S&P 500 rose 0.5% in early trading Wednesday. The benchmark gauge lost 1.8% Tuesday, its second decline in three trading days. The technology-heavy Nasdaq Composite Index added around 1% and the Dow Jones Industrial Average rose 0.2%.

Some of the U.S.’s biggest lenders reported rising earnings before the market opened. Bank of America shares rose 2.9% after the lender reported a jump in fourth-quarter profits, while Morgan Stanley’s shares gained 1.7% on profits that topped forecasts. U.S. Bancorp fell almost 6% after the bank holding company posted a rise in compensation costs. This earnings season, Goldman Sachs,

JPMorgan Chase

and

Citigroup

have also reported shelling out more in compensation.

Procter & Gamble

said consumers were undeterred by higher prices, leading to higher revenue and lifting shares of the consumer-goods company 4.2%.

Investors have stepped up bets that major central banks will tighten monetary policy.

Photo:

Wang Ying/Zuma Press

Government-bond prices edged up, pushing down yields. Yields on benchmark 10-year Treasury notes slipped to 1.852% from 1.866% Tuesday, which was their highest level since January 2020. Yields on interest rate-sensitive two-year notes were down to 1.010% from 1.038% Tuesday.

The first few weeks of the year have been tumultuous. In January, many investors started positioning for a world that looks very different from last year. Interest rates are supposed to start rising and some investors are positioning for the Covid-19 pandemic to turn into an endemic.

Investors have stepped up bets that the Federal Reserve and other major central banks will tighten monetary policy in the coming months, withdrawing a pillar of support for markets. Mounting expectations of interest-rate rises follow evidence that the drivers of inflation have broadened beyond the supply-chain shock that fueled price gains for much of 2021.

As a result, many investors have backed away from one of the hottest areas of the market: tech. The Nasdaq Composite was down almost 10% from its high as of Tuesday.

And there are signs that individual investors—a key force behind 2021’s stock-market rally—are cooling on tech, according to analysts at Vanda Research. Retail investors have been buying shares of financials and energy companies while their purchases of highflying stocks like

Advanced Micro Devices

and

Nvidia

have been dwindling, according to Vanda.

The S&P 500’s value index is outperforming its growth index by around 6.8 percentage points this month, on pace for the biggest monthly outperformance since December 2000, according to Dow Jones Market Data.

Recent volatility is“really all about inflation and how aggressive central banks are going to be to counteract it,” said

Brian O’Reilly,

head of market strategy at Mediolanum Asset Management, adding that inflation could also curtail economic growth by knocking consumption. ”Certainly, the market is nervous at the moment.”

Europe’s most closely watched government bond yield turned positive for the first time since 2019. The yield on 10-year German bund rose as high as 0.021% Wednesday after trading in negative territory for over 30 months. It then eased to 0.010%. Ten-year U.K. yields, meanwhile, reached their highest level since March 2019 after data showed inflation hitting a 30-year high.

To keep out Covid-19, China closed some border gates late last year, leaving produce to rot in trucks. Restrictions like these and rules at some Chinese ports, the gateways for goods headed to the world, could cascade into delays in the global supply chain. Photo composite: Emily Siu

Oil prices rose again after touching seven-year highs Tuesday. Most-active U.S. crude futures rose around 1% to $85.55 a barrel, extending a rally driven in part by the potential for supply disruptions in Russia and the Middle East.

Overseas stock markets were mixed following Tuesday’s selloff on Wall Street. The Stoxx Europe 600 rose 0.7%, as gains for retail and resource stocks offset losses for food, drink and insurance companies. Asian stocks came under pressure, with Japan’s Nikkei 225 skidding 2.8%. China’s Shanghai Composite Index slipped 0.3%.

Write to Joe Wallace at joe.wallace@wsj.com and Gunjan Banerji at gunjan.banerji@wsj.com

The pain is piling up for equity investors after the long U.S. holiday weekend, with bond yields at levels not seen since early 2020, and oil prices tapping 2014 highs.

The pace of Federal Reserve monetary policy tightening amid the highest inflation in about 40 years, a bumpy start to the corporate earnings reporting season and pandemic uncertainties are just a few things on the worry list. Technology stocks

COMP,

-1.12%

are set to take the biggest hit on Tuesday, as a rapid rise in short term interest rates tends to make their future cash flows less valuable.

While a Deutsche Bank chart (below) reveals more tech-bubble worries, our call of the day makes a case for one of the biggest tech stalwarts, Apple

AAPL,

-0.43%,

saying the iPhone maker has an ace in the hole that few are paying attention to.

That call comes from investment adviser Wedgewood Partners, who kick off their fourth-quarter 2021 client letter with a warning about market volatility for 2022, triggered by central bankers who are about to usher in some market chaos by pulling the plug on years of cheap money. Even Chinese President Xi Jinping was heard warning the Fed not to hike interest rates at a virtual Davos on Tuesday.

However, the adviser also sees opportunities ahead as selling picks up speed, and they plan to stick to Apple, which they’ve owned for 16 years.

While Wedgewood said it couldn’t foresee the many products the company unveiled, “we did know that Apple’s vertically integrated [software and hardware] product development strategy was unique and extremely capable of creating products and experiences that customers thought worthwhile enough to spend growing amounts of time and money on,” said the adviser.

Today, that strategy remains intact, but more important Apple is commanding a key new realm, having developed over a dozen custom processors and integrated circuits, since launching its “A-series” processors. For example, one it produced in 2017 provided the iPhone X with enough power to operate FaceID 3-D algorithms, used to unlock phones and make digital payments.

“Apple has effectively created a semiconductor business that rivals and even surpasses some of the most established semiconductor-focused businesses in the industry,” said Wedgewood. “Apple continues to differentiate through vertical integration, which has been a hallmark of Apple’s long-term strategy to grow and capture superior profitability. It is difficult to predict what new products will be unveiled; however, we think this strategy should continue to serve shareholders quite well.”

Other top positions recommended by Wedgewood include telecom group Motorola

MSI,

-1.73%,

another tech stalwart Microsoft

MSFT,

-0.23%

and retailer Tractor Supply

TSCO,

-1.14%.

Here’s a final comment from Wedgewood about the stock storm it sees brewing. “The graphic below reminds us that when speculation reigns, markets can go far higher than what seems sober,” but when they fall “markets will repeat their long history of falling faster and further than what seems sober.”

Wedgewood Partners

“Long term investors should root for such downside. Such times are opportunities to improve portfolios. Our pencils are sharpened for opportunities as Mr. Market serves them up.”

The markets

Microsoft shares are slipping after the tech group confirmed it will buy Activision Blizzard

ATVI,

+27.39%

in a $68.7 billion cash deal. The gaming group’s shares are flying, along with those of rival Electronics Arts

EA,

+6.72%.

Goldman Sachs

GS,

-7.72%

added to a disappointing batch of bank results from last week, with shares down as earnings came up short, with Charles Schwab

SCHW,

-4.29%

also falling on gloomy results. Kinder Morgan

KMI,

-0.14%

and Alcoa

AA,

-1.43%

are still to come.

Airbnb shares

ABNB,

-2.49%

are slumping after ratings and target cut from an analyst who sees multiple headwinds and too-few catalysts.

The New York Empire state manufacturing index for January fell well short of expectations. A National Association of Home Builders index for the same month is still ahead.

An unpublished study by an Israeli hospital showed second Pfizer

PFE,

-1.78%

-BioNTech

BNTX,

-7.77%

or Moderna

MRNA,

-4.70%

boosters aren’t halting omicron infections. Separately, Moderna’s CEO Stephane Bancel said his company is working on a combined flu/COVID booster, while White House chief medical advise Dr. Anthony Fauci, said it’s too soon to tell if omicron will bring us out of the pandemic.

Another study says COVID infections are turning children into fussy eaters due to parosmia disorders that distort their sense of smell. And China state media says packages from the U.S. and Canada had helped spread omicron, as Hong Kong gets ready to cull thousands of hamsters.

An airline lobby group is warning of “chaos” for U.S. air travelers due to 5G services rolling out this month, in a letter signed by big carriers, UPS

UPS,

-1.55%

and FedEx

FDX,

-1.39%.

Larry Fink, chairman and chief executive of BlackRock

BLK,

-1.72%

said investors need to know where company leaders stand on societal issues.

Retailer Walmart

WMT,

-1.28%

is looking at creating its own cryptocurrency and nonfungible tokens, according to U.S. patent filings.

The markets

Uncredited

The Nasdaq Composite

COMP,

-1.12%

is sprinting ahead with losses, with the Dow

DJIA,

-1.43%

and S&P 500

SPX,

-1.24%

also lower Tuesday led by those for the Nasdaq-100

NQ00,

-1.28%

as bond yields

TMUBMUSD10Y,

1.848%

TMUBMUSD02Y,

1.034%

surge across the curve. Oil prices

BRN00,

+1.06%

CL00,

+1.56%

are surging after Iran-backed Houthi rebels launched a deadly drone attack on a key oil facility in Abu Dhabi. Goldman Sachs also predicted Brent could top $100 a barrel in 2023, while the OPEC left its 2022 global oil-demand forecast unchanged.

Losses spread to Asian

NIK,

-0.27%

and Europe stocks

SXXP,

-0.77%,

with a key German bund yields

TMBMKDE-10Y,

-0.012%

about to turn positive for the first time in three years.

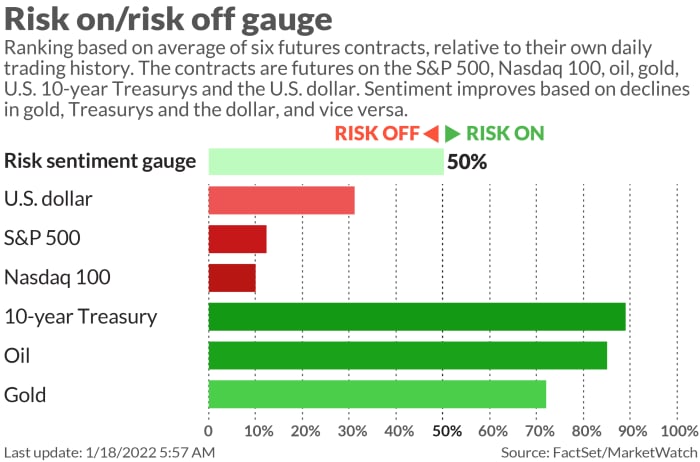

The chart

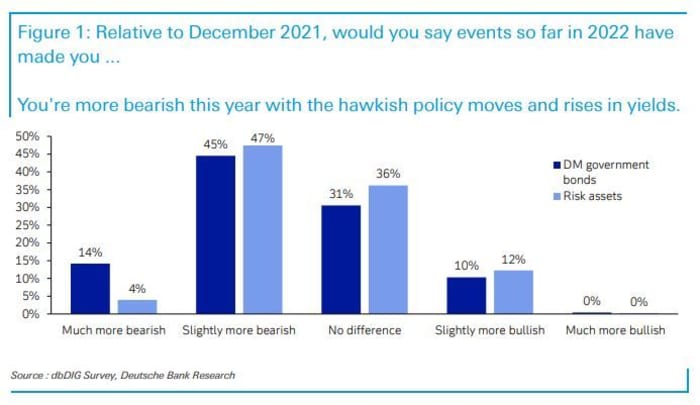

A January survey of more than 500 investors polled by Deutsche Bank shows a slightly gloomier mood. For example, they are more bearish:

Uncredited

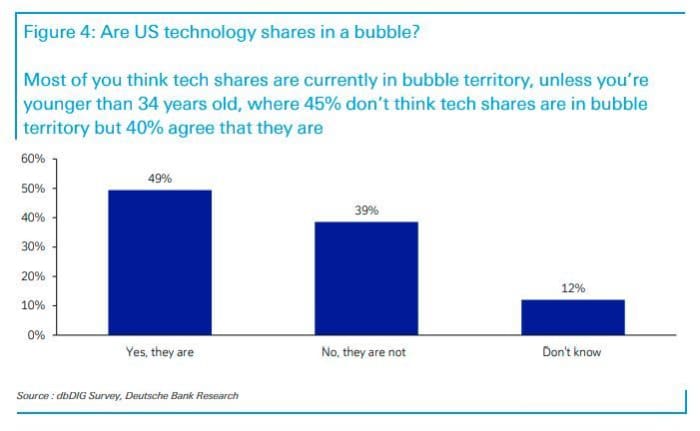

Many, especially those over 34, think tech shares are in a bubble:

Uncredited

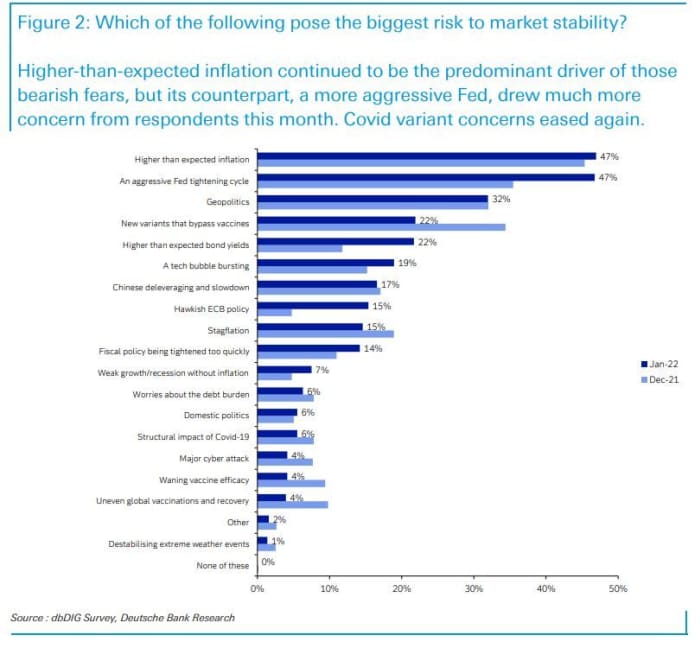

And they continue to see inflation as the biggest risk to markets, but are also fretting a more aggressive Fed:

Uncredited

Here are the top stock tickers on MarketWatch as of 6 a.m. Eastern Time.

Ticker

Security name

TSLA,

+1.47%

Tesla

GME,

-5.61%

GameStop

AMC,

-6.32%

AMC Entertainment

BBIG,

+29.75%

Vinco Ventures

NIO,

-0.71%

NIO

AAPL,

-0.43%

Apple

CENN,

-4.72%

Cenntro Electric Group

NVDA,

-1.57%

Nvidia

BABA,

-0.85%

Alibaba

NVAX,

-4.04%

Novavax

Random reads

Tulsa pastor apologizes for wiping his saliva on a man’s face during a sermon.

The high environmental cost of your beloved fish-oil pills.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Want more for the day ahead? Sign up for The Barron’s Daily, a morning briefing for investors, including exclusive commentary from Barron’s and MarketWatch writers.

Bond yields are rising again so far in 2022. The U.S. stock market seems vulnerable to a bona fide correction. But what can you really tell from a mere two weeks into a new year? Not much and quite a lot.

One thing feels assured: the days of making easy money are over in the pandemic era. Benchmark interest rates are headed higher and bond yields, which have been anchored at historically low levels, are destined to rise in tandem.

Read: Weekend reads: How to invest amid higher inflation and as interest rates rise

It seemed as if Federal Reserve members couldn’t make that point any clearer this past week, ahead of the traditional media blackout that precedes the central bank’s first policy meeting of the year on Jan. 25-26.

The U.S. consumer-price and producer-price index releases this week have only cemented the market’s expectations of a more aggressive or hawkish monetary policy from the Fed.

The only real question is how many interest-rate increases will the Federal Open Market Committee dole out in 2022. JPMorgan Chase & Co.

JPM,

-6.15%

CEO Jamie Dimon intimated that seven might be the number to beat, with market-based projections pointing to the potential for three increases to the federal funds rate in the coming months.

Check out: Here’s how the Federal Reserve may shrink its $8.77 trillion balance sheet to combat high inflation

Meanwhile, yields for the 10-year Treasury note yielded 1.771% Friday afternoon, which means that yields have climbed by about 26 basis points in the first 10 trading days to start a calendar year, which would be the briskest such rise since 1992, according to Dow Jones Market Data. Back 30 years ago, the 10-year rose 32 basis points to around 7% to start that year.

The 2-year note

TMUBMUSD02Y,

0.960%,

which tends to be more sensitive to the Fed’s interest rate moves, is knocking on the door of 1%, up 24 basis points so far this year, FactSet data show.

But do interest rate increases translate into a weaker stock market?

As it turns out, during so-called rate-hike cycles, which we seem set to enter into as early as March, the market tends to perform strongly, not poorly.

In fact, during a Fed rate-hike cycle the average return for the Dow Jones Industrial Average

DJIA,

-0.56%

is nearly 55%, that of the S&P 500

SPX,

+0.08%

is a gain of 62.9% and the Nasdaq Composite

COMP,

+0.59%

has averaged a positive return of 102.7%, according to Dow Jones, using data going back to 1989 (see attached table). Fed interest rate cuts, perhaps unsurprisingly, also yield strong gains, with the Dow up 23%, the S&P 500 gaining 21% and the Nasdaq rising 32%, on average during a Fed rate hike cycle.

Dow Jones Market Data

Interest rate cuts tend to occur during periods when the economy is weak and rate hikes when the economy is viewed as too hot by some measure, which may account for the disparity in stock market performance during periods when interest-rate reductions occur.

To be sure, it is harder to see the market producing outperformance during a period in which the economy experiences 1970s-style inflation. Right now, it feels unlikely that bullish investors will get a whiff of double-digit returns based on the way stocks are shaping up so far in 2022. The Dow is down 1.2%, the S&P 500 is off 2.2%, while the Nasdaq Composite is down a whopping 4.8% thus far in January.

Read: Worried about a bubble? Why you should overweight U.S. equities this year, according to Goldman

What’s working?

So far this year, winning stock market trades have been in energy, with the S&P 500’s energy sector

SP500.10,

+2.44%

XLE,

+2.35%

looking at a 16.4% advance so far in 2022, while financials

SP500.40,

-1.01%

XLF,

-1.04%

are running a distant second, up 4.4%. The other nine sectors of the S&P 500 are either flat or lower.

Meanwhile, value themes are making a more pronounced comeback, eking out a 0.1% weekly gain last week, as measured by the iShares S&P 500 Value ETF

IVE,

-0.14%,

but month to date the return is 1.2%.

See: These 3 ETFs let you play the hot semiconductor sector, where Nvidia, Micron, AMD and others are growing sales rapidly

What’s not working?

Growth factors are getting hammered thus far as bond yields rise because a rapid rise in yields makes their future cash flows less valuable. Higher interest rates also hinder technology companies’ ability to fund stock buy backs. The popular iShares S&P 500 Growth ETF

IVW,

+0.28%

is down 0.6% on the week and down 5.1% in January so far.

What’s really not working?

Biotech stocks are getting shellacked, with the iShares Biotechnology ETF

IBB,

+0.65%

down 1.1% on the week and 9% on the month so far.

And a popular retail-oriented ETF, the SPDR S&P Retail ETF

XRT,

-2.10%

tumbled 4.1% last week, contributing to a 7.4% decline in the month to date.

And Cathie Wood’s flagship ARK Innovation ETF

ARKK,

+0.33%

finished the week down nearly 5% for a 15.2% decline in the first two weeks of January. Other funds in the complex, including ARK Genomic Revolution ETF

ARKG,

+1.04%

and ARK Fintech Innovation ETF

ARKF,

-0.99%

are similarly woebegone.

And popular meme names also are getting hammered, with GameStop Corp.

GME,

-4.76%

down 17% last week and off over 21% in January, while AMC Entertainment Holdings

AMC,

-0.44%

sank nearly 11% on the week and more than 24% in the month to date.

Gray swan?

MarketWatch’s Bill Watts writes that fears of a Russian invasion of Ukraine are on the rise, and prompting analysts and traders to weigh the potential financial-market shock waves. Here’s what his reporting says about geopolitical risk factors and their longer-term impact on markets.

Week ahead

U.S. markets are closed in observance of the Martin Luther King Jr. holiday on Monday.

Read: Is the stock market open on Monday? Here are the trading hours on Martin Luther King Jr. Day

Notable U.S. corporate earnings

(Dow components in bold) TUESDAY:

Goldman Sachs Group

GS,

-2.52%,

Truist Financial Corp.

TFC,

+0.96%,

Signature Bank

SBNY,

+0.07%,

PNC Financial

PNC,

-1.33%,

J.B. Hunt Transport Services

JBHT,

-1.04%,

Interactive Brokers Group Inc.

IBKR,

-1.22%

WEDNESDAY:

Morgan Stanley

MS,

-3.58%,

Bank of America

BAC,

-1.74%,

U.S. Bancorp.

USB,

+0.09%,

State Street Corp.

STT,

+0.32%, UnitedHealth Group Inc.

UNH,

+0.27%, Procter & Gamble

PG,

+0.96%,

Kinder Morgan

KMI,

+1.82%,

Fastenal Co.

FAST,

-2.55%

THURSDAY:

Netflix

NFLX,

+1.25%,

United Airlines Holdings

UAL,

-2.97%,

American Airlines

AAL,

-4.40%,

Baker Hughes

BKR,

+4.53%,

Discover Financial Services

DFS,

-1.44%,

CSX Corp.

CSX,

-0.82%,

Union Pacific Corp.

UNP,

-0.55%, The Travelers Cos. Inc. TRV, Intuitive Surgical Inc. ISRG, KeyCorp.

KEY,

+1.16%

FRIDAY:

Schlumberger

SLB,

+4.53%,

Huntington Bancshares Inc.

HBAN,

+1.73%

U.S. economic reports

Tuesday

Empire State manufacturing index for January due at 8:30 a.m. ET

NAHB home builders index for January at 10 a.m.

Wednesday

Building permits and starts for December at 8:30 a.m.

Philly Fed Index for January at 8:30 a.m.

Thursday

Initial jobless claims for the week ended Jan. 15 (and continuing claims for Jan. 8) at 8:30 a.m.

Existing home sales for December at 10 a.m.

Friday

Leading economic indicators for December at 10 a.m.

Technology stocks tumbled on Monday as government bond yields continued to rise, signaling that investors expect the Federal Reserve to move quickly in raising interest rates.

The tech-heavy Nasdaq Composite Index slid 2.6%. The benchmark last week posted its biggest one-week percentage decline since February, as rising bond yields punctured tech valuations. The S&P 500 was down 1.9% in Monday trading, while the Dow Jones Industrial Average fell 1.6%, or 578 points.

Chip maker

Nvidia,

one of 2021’s best-performing stocks, slumped 5%. Google parent Alphabet,

Apple

and

Microsoft

all declined more than 2%.

The tech losses came as the yield on benchmark 10-year Treasury notes—which moves inversely to their price—rose to 1.798% Monday from 1.769% Friday. Friday’s closing level was the highest since January 2020, before yields tumbled at the start of the pandemic.

Rising yields at the start of 2022 have sent a shudder through tech stocks. By selling bonds and sending yields higher, investors are indicating that they believe the Fed could raise short-term interest rates in March and begin to shrink its holdings of bonds and other assets soon afterward.

Low rates helped fuel a huge rally in tech stocks last year, by making it less attractive for investors to hold bonds and encouraging them to buy risky assets. But as the Fed has pivoted to fighting inflation in recent weeks, tech stocks have lost some of their luster.

U.S. inflation data due Wednesday will be keenly watched as investors seek to predict when the Fed will begin to raise borrowing costs. Monthly consumer prices are expected to have risen more than 7% from a year earlier, for the first time since 1982.

Traders at the New York Stock Exchange on Friday.

Photo:

Spencer Platt/Getty Images

Earnings season kicks off at major U.S. financial firms later this week, with JPMorgan Chase,

Citigroup,

Wells Fargo and

BlackRock

due to file results for the final quarter of 2021. Many investors have been pushing money into bank stocks, figuring they stand to profit from a rise in interest rates.

Among them is

Hani Redha,

a multiasset fund manager at PineBridge Investments. He said the New York-based investment firm has cut its ownership of tech stocks and Treasurys while boosting cash holdings and exposure to financial companies.

“Equities are down and bonds are down too,” Mr. Redha said. “At least for a while, even cash is better than owning risk assets.”

In individual stocks,

Take-Two Interactive

fell 14% after the videogame maker agreed to buy

Zynga

in an $11-billion deal. Zynga rose more than 40%.

Lululemon

declined 5.8% after saying fourth-quarter earnings would fall toward the low end of forecasts.

GameStop,

a favorite among individual traders, lost 14%, having jumped last week after The Wall Street Journal reported that it planned to enter the nonfungible tokens and cryptocurrency markets.

In commodities, U.S. natural-gas prices rose 4.1% to $3.88 per million British thermal units. Cold weather in the Midwest and eastern U.S. early this week will likely boost demand for the fuel, according to analysts at NatGas Weather.

The U.S. dollar last year saw its largest increase in value since 2015. That’s good for many American consumers, but it could also put a dent in stocks and the U.S. economy. WSJ’s Dion Rabouin explains. Photo illustration: Sebastian Vega/WSJ

Overseas stock markets were mixed. The Stoxx Europe 600 fell 1.4%, weighed down by shares of real estate and tech companies.

In Asia, the Shanghai Composite Index added 0.4% and Hong Kong’s Hang Seng rose 1.1%. Japanese markets were closed for a public holiday.

Mark Andersen, head of asset allocation at UBS Global Wealth Management’s Chief Investment Office, said he favors European and Japanese stocks and shares of energy and financial companies.

“It’s clear the Fed wants to tighten financial conditions and the means to do that is obviously to get interest rates higher,” he said.

U.S. stock futures wavered after the monthly jobs report missed expectations.

Futures tied to the S&P 500 slipped around 0.3% , after the broad-market index closed down 0.1% in Thursday’s choppy session. Nasdaq-100 futures slipped 0.8% and Dow Jones Industrial Average futures edged down around 0.2%.

The yield on the benchmark 10-year Treasury note hovered at 1.760%, after four consecutive days of rises. Yields increase as bond prices decline.

The latest monthly jobs report showed that the U.S. added 199,000 jobs in December, below the 422,000 expected. Still, 2021 concluded with the U.S. adding a record number of jobs last year and the jobless rate fell to 3.9%.

Stocks came under pressure this week after the Federal Reserve’s minutes confirmed its intention to pull back stimulus and suggested it might do so sooner and faster than previously planned, due to high inflation. The S&P 500 is down 1.5% this week, on track for the worst weekly performance since mid-December.

Meme stock

GameStop

surged around 18% in premarket trading after The Wall Street Journal reported the company was planning to enter the cryptocurrency and nonfungible token markets.

AMC Entertainment,

another company popular with retail traders, advanced 5%.

Government bonds have sold off as markets price in the possibility of earlier interest rate increases and the Fed shrinking its portfolio of bonds in the near future.

Stocks have been under pressure since the release of the Federal Reserve’s policy meeting minutes.

Photo:

BRENDAN MCDERMID/REUTERS

“Everything happening in markets this week was about expectations on how fast the Fed is going to tighten policy,” said Fahad Kamal, chief investment officer at Kleinwort Hambros. “This is a transition year where we go from record policy support toward actual tightening. There will be huge volatility as we figure out how to work in this paradigm.”

Fed officials have said labor market health is a crucial factor in their monetary policy decisions. Investors will be scrutinizing the report closely to see if it is consistent with the Fed’s plans outlined in the minutes and whether wages are continuing to increase, which could mean more sustained inflation.

“If the data shows the labor market is still running pretty hot, it strengthens the case for hawks that the Fed needs to get on and tighten policy,” said Sebastian Mackay, a multiasset fund manager at Invesco.

Oil prices edged up. Global benchmark Brent crude rose 0.8% to $82.63 a barrel in recent trading, the highest level in over eight weeks. Oil supply could potentially be lower due to cold weather in North Dakota and Alberta, Canada and if protests in crude producer Kazakhstan affect output, according to analysts at ING.

Protests first triggered by rising fuel prices in Kazakhstan have turned violent, prompting a Russian-led military coalition to send troops to the oil-rich country. Video shows government buildings and streets in several cities being stormed by demonstrators. Photo: Mariya Gordeyeva/Reuters

Overseas, the pan-continental Stoxx Europe 600 ticked down 0.3%.

European government bond yields rose, with the 10-year German bund yield climbing to minus 0.1%. If it surpasses 0, it will be in positive territory for the first time since 2019.

In Asia, major stock benchmarks were mixed. The Shanghai Composite Index fell 0.2%, while Hong Kong’s Hang Seng Index rose 1.8%, led by gains in technology stocks. E-commerce giants Alibaba rose 6.5% and

JD.com

gained 4.8%. South Korea’s Kospi Index rose 1.2%.

—Gunjan Banerji contributed to this article.

Write to Anna Hirtenstein at anna.hirtenstein@wsj.com

Corrections & Amplifications GameStop rallied premarket. An earlier version of this article incorrectly referred to GameStop as GameStock. (Corrected on Jan. 7.)

Blame it on an obscure rule. For the first time in a decade, there will be no U.S. stock-market closure in observance of New Year’s Day which falls on a Saturday.

U.S. markets will be open on Friday Dec. 31, which is New Year’s Eve, and operators of the New York Stock Exchange are not designating Jan. 3, the first Monday in 2022, as a holiday in lieu of New Year’s Day either.

The last time this sort of calendar event transpired was on New Year’s Eve in 2010.

How rare is this calendar event? Assuming that it was applied since 1928, it would have occurred 13 times from 1928.

Dow Jones Market Data

The lack of a New Year’s Day respite for stock traders is the result of NYSE Rule 7.2, which stipulates that the exchange will be closed either Friday or the following Monday if the holiday falls on a weekend, unless “unusual business conditions exist, such as the ending of a monthly or yearly accounting period.”

In this case, the last day of December is a trifecta of accounting dates, including month-, quarter- and year-end dates, and comes as markets have experienced a year end rally.

Although U.S. bond markets also will be open on Friday, the trading body that oversees fixed-income trading, The Securities Industry and Financial Markets Association recommends a 2 p.m. close for trading in bonds, such as the 10-year Treasury note

TMUBMUSD10Y,

1.514%

an hour earlier.

For its part, the U.S. stock market this year has seen its best start to a Santa Claus rally, usually defined as trading during the last five sessions of the year and the first two days of the new year, in a couple of decades.

Investors have essentially dismissed concerns about the economic impact of the omicron variant of COVID. The Dow Jones Industrial Average

DJIA,

+0.12%

and the S&P 500

SPX,

+0.04%

were on track for gains of about 5% or better in December and have risen by at least 1.5% on the week, while the Nasdaq Composite

COMP,

-0.26%

was looking at a gain of about 2% on the month and 1% on the week, as of Thursday afternoon.

A downturn in global stocks appears to be spilling over into the nascent crypto market, with a bout of weekend selling erupting into a mini-flash crash in prices of bitcoin and other notable digital assets.

At last check Saturday afternoon New York time, bitcoin

BTCUSD,

-21.43%

was changing hands at $48,186.96 on CoinDesk, down 12% over the past 24 hours, but the overnight descent, in the early hours of Saturday morning, had been even more harrowing. Bitcoin’s slump to around $42,000 on some exchanges meant that it had tumbled nearly 30% peak to trough on a 24-hour basis.

NYDIG, a technology and financial services firm dedicated to Bitcoin, said that the decline was even more severe for some offshore platforms such as Huobi, where bitcoin briefly touched a 24-hour nadir at $28,800.

That is a gut-wrenching fall, that may even leave some veteran crypto bulls feeling a touch queasy.

The drop also meant that the total market value of the crypto universe, as tracked by CoinMarketCap.com, shed nearly $400 billion to around $2 trillion, before recovering to around $2.2 trillion.

Source: CoinMarketCap.com

So what precipitated the drop? It isn’t 100% clear.

The analysts at CoinDesk blamed at least some of the downturn on trading in crypto derivatives, amplified by growing concerns about the prospects for tighter financial conditions that is forcing a repricing of assets that are sensitive to potentially rising borrowing costs.

“The decline was likely in part technically-driven, exacerbated by the derivatives market, and not helped by the downside momentum behind high-growth stocks on Friday, to which bitcoin has been positively correlated,” wrote Katie Stockton of Fairlead Strategies, in a Saturday morning note.

NYDIG estimates that $1.1 billion of leveraged bitcoin positions and $2.5 billion of crypto leveraged positions (including bitcoin) have been liquidated in the past 24 hours, representing the largest such notional liquidation since Sept. 7.

Bitcoin ‘s values have been softening for weeks but declines for other risky assets have been accelerating with the Federal Reserve indicating it might increase the pace at which it is withdrawing the market support provided in the past 18 months during the coronavirus pandemic as it turns its attention to restraining inflation. This so-called “tapering” of bond purchases has investors believing that interest-rates hikes are next on the central bank’s agenda in 2022.

Some believe that bitcoin and other digital assets aren’t correlated with the prices of other assets, which has been heralded as one of the more appealing features of bitcoin and its ilk. However, crypto has been trading more in step with traditional stocks and bonds recently partly because of the prevailing low interest-rate environment and if that changes then the values of a host of assets, also factoring in inflation, must be reassessed.

Put another way, the value of an asset is its future income, discounted to the present using interest rates, plus a “risk premium”—the extra return you expect for owning something riskier than a government bond. A rising interest rate diminishes the present value of that future income.

In traditional markets, that repricing has seen technology shares underperform as they are the most sensitive to shifts in rates. The tech-laden Nasdaq Composite Index

COMP,

-1.92%

stands 6% from its Nov. 19 peak, with declines gathering steam over the past week, amid fears about the economic impact of the coronavirus omicron variant and concerns about the Fed’s monetary policy plans.

Meanwhile, the Dow Jones Industrial Average

DJIA,

-0.17%,

is half way toward a correction, and is off more than 5% from its Nov. 8 record close, and the S&P 500 index

SPX,

-0.84%

is 3.5% from its all-time high close put in on Nov. 18, while the small-capitalization Russell 2000 index fell into correction, commonly defined as a fall of at least 10% from a recent peak, on Thursday.

On Twitter, Michael Novogratz, founder and Chief Executive of crypto firm Galaxy Digital, tweeted that the backdrop in markets was a “perfect storm,” perhaps referring to the tumble in broader markets, omicron fears and hawkish comments from the Federal Reserve.

Fairlead’s Stockton says that if the downturn persists, after bitcoin broke through an area of support at around $53,000, it would qualify as a more troubling technical breakdown of the uptrend in the asset’s price.

“ Momentum has weakened to the extent that there is a pending weekly MACD ‘sell’ signal that would be solidified upon a confirmed breakdown tomorrow, she wrote, referring to the Moving Average Convergence/Divergence, used by technical analysts as a gauge of momentum in an asset.

However, NYDIG suggested that they are seeing positive trends for bitcoin and crypto: “On our desk, we have seen two-way flows today with 84% of the flows being buys on our trading desk excluding tax loss harvesting trades,” the company wrote in a note on Saturday.

In other crypto, Ether

ETHUSD,

-16.54%

on the Ethereum blockchain was trading down 6% but holding above $4,000 at 4,050.85, at last check Saturday afternoon. It had been as low as around $3,500 overnight.

To be sure, crypto is one of the more volatile assets and is still in the phase of gaining credibility as a bona fide alternative asset.

Some crypto bulls, known for holding the investment long-term despite its tendency for wild swings, were making light of the Saturday slump such as this tweet from the Twitter account associated with Billy Markus, one of the founders of dogecoin

DOGEUSD,

-33.22%,

which has become such a popular meme asset that it has been duplicated by other tokens such as Shiba Inu

SHIBUSD, .

made an overdue interest payment to international bondholders, the state-owned Securities Times reported Friday, an unexpected move that allows the property company to stave off a default.

The Chinese real-estate developer on Thursday sent $83.5 million to the trustee for the dollar bonds, and that financial institution will in turn pay bondholders, the Securities Times reported. The financial paper is run by the Communist Party’s flagship People’s Daily newspaper.

Evergrande was nearing the end of a 30-day grace period before bondholders could send a notice of default to the company after it failed to make the interest payment on about $2.03 billion of dollar bonds on Sept. 23.

A default on those bonds would likely have spiraled into the biggest corporate default in Asia, by enabling creditors to declare defaults on some of Evergrande’s other debts. The company is one of China’s biggest developers, and its most indebted. It had the equivalent of more than $300 billion in total liabilities, including some $89 billion in interest-bearing debt, as of the end of June.

Many international bondholders had expected Evergrande to fail to make its dollar bond payments before the end of the grace period. The company has also skipped other coupon payments in the past few weeks, and has outstanding dollar debt with a total face value of about $20 billion. Advisers to international bondholders said this month they had made little progress in their efforts to engage with Evergrande.

On Wednesday, however, the Shenzhen-based group said in a regulatory filing that it will “use its best effort to negotiate for the renewal or extension of its borrowings or other alternative arrangements with its creditors.”

Evergrande has been trying to raise funds by disposing of assets such as stakes in subsidiaries and a Hong Kong office building that it owns. Last month, it agreed to sell most of its ownership in a Chinese commercial bank to a state-owned enterprise for the equivalent of $1.55 billion. The company had also planned to sell a majority holding in its property-management unit for the equivalent of about $2.6 billion to a smaller rival, but said this week that it had terminated that deal.

Evergrande’s Hong Kong-listed stock has crashed more than 80% this year and its dollar bonds are trading far below face value, indicating skepticism among investors that they will be repaid in full. On Friday, the shares rose 5% in early trading, while its bonds were still at deeply distressed levels that indicate investors still expect the company to ultimately default.

A $4.7 billion, 8.75% Evergrande bond due 2025 was quoted at just 21.75 cents on the dollar Friday morning in Hong Kong, according to Tradeweb, up from 20.5 cents late Thursday.

The developer is the highest-profile casualty of a campaign by Chinese authorities to tame the housing market, in part by tamping down on excessive corporate borrowing through limits on bank lending and restrictions on developers’ leverage known as the “three red lines.”

But the sector as a whole has run up huge debts—more than $5 trillion, including cash raised from home buyers through presales of still-uncompleted apartments, according to economists at Nomura—and is smarting under the new regime.

Contracted sales, which reflect new contracts signed with home buyers, at many developers fell more than 20% or 30% year-over-year in September, and official government statistics show nationwide new-home prices fell slightly last month for the first time since 2015.

Evergrande’s own contracted sales have plunged even more; the developer said this week that its contracted sales “for the month of September 2021 and up till now” totaled the equivalent of just $572 million, far below the $28.5 billion worth of contracted sales it reported in the full two months of September and October 2020.

Several smaller developers, such as Fantasia Holdings Group Co., have recently either defaulted on their debts or demanded investors wait longer for repayment, and prices for the bonds of many developers are trading at deeply distressed levels.

—Frances Yoon contributed to this article.

China Evergrande Group: Stalled Construction, Massive Debts

Write to Elaine Yu at elaine.yu@wsj.com and Quentin Webb at quentin.webb@wsj.com

As China enters what many economists say is the final stage of one of the largest real-estate booms in history, it is confronting a staggering bill: More than $5 trillion in debt that developers took on when times were good, according to economists at

Nomura Holdings Inc.

That debt is nearly double what it was at the end of 2016 and is more than the entire economic output of Japan, the world’s third-largest economy, last year.

Global markets are braced for a possible wave of defaults, with warning signs flashing over the debt of about two-fifths of development companies that have borrowed from international bond investors.

Chinese leaders are getting serious about addressing the debt, with a series of moves meant to curb excessive borrowing. But doing so without torpedoing the property market, crippling more developers and derailing the country’s economy is quickly turning into one of the biggest economic challenges Chinese leaders have faced in years, and one that could reverberate globally if mismanaged.

Luxury developer

Fantasia Holdings Group Co.

failed to repay $206 million in dollar bonds that matured Oct. 4. In late September, Evergrande, which has more than $300 billion in obligations, missed two interest-payment deadlines for bonds.

Asia’s junk-bond markets suffered a wave of selling last week. On Friday, bonds from 24 of the 59 Chinese development companies in an ICE BofA index of Asian corporate dollar bonds were trading at yields of above 20%, levels that indicate high risk of default.

Some prospective home buyers are balking, forcing the companies to cut prices to raise cash, and potentially accelerating their slide if the trend continues.

The Evergrande Fairyland complex in Lu’An, China, with towers under construction. Evergrande recently missed two bond-interest deadlines.

Photo:

Raul Ariano for The Wall Street Journal

Total sales among China’s 100 largest developers were down by 36% in September from a year earlier, according to data from CRIC, a research unit of property services firm

e-House (China) Enterprise Holdings Ltd.

It showed that the 10 biggest developers, including China Evergrande,

Country Garden Holdings Co.

and

China Vanke Co.

, saw sales down 44% from a year ago.

Economists say that most Chinese developers remain relatively healthy. Beijing also has the firepower and tight control of the financial system needed to prevent a so-called Lehman moment in which a corporate collapse snowballs into a financial crisis, they say.

In late September, The Wall Street Journal reported that China had asked local governments to prepare for problems potentially intensifying at Evergrande.

But many economists, investors and analysts agree that even for healthy ventures, the underlying business model—in which developers use debt to fund a steady churn of new construction despite demographics becoming less favorable for new housing—is likely to change. Some developers might not survive the transition, they say.

Of particular concern is some developers’ practice of relying heavily on “presales,” in which buyers pay in advance for still-uncompleted apartments.

The practice, more common in China than the U.S., means developers are in effect borrowing interest-free from millions of households, making it easier to continue expanding but potentially leaving buyers without finished apartments should the developers fail.

Presales and similar deals were the sector’s biggest funding source this year through August, according to the National Bureau of Statistics of China.

A model of a residential compound by China Vanke, a large developer, at its showroom in Dongguan, China.

Photo:

china stringer network/Reuters

“There is no return to the previous growth model for China’s real-estate market,” said

Houze Song,

a research fellow at the Paulson Institute, a Chicago think tank focused on U.S.-China relations. He said China is likely to keep in place a set of limits on corporate borrowing it imposed last year, known as the “three red lines,” which helped trigger the recent distress at some developers, though he said China might ease some other curbs.

While Beijing has avoided clear public statements on its plans for dealing with the most indebted developers, many economists believe leaders have no choice but to keep the pressure on them.

Policy makers appear determined to revamp a model driven by debt and speculation as part of President

Xi Jinping’s

broader efforts to defuse hidden risks that could destabilize society, especially ahead of important Communist Party meetings next year. Mr. Xi is widely expected then to break with precedent and extend his rule into a third term.

Beijing is worried that after years of rapid home-price gains, some people may be unable to get on the housing ladder, potentially fueling social discontent as wealth gaps widen, economists say. Young couples in large cities are beginning to get priced out, making it harder for them to start families. The median apartment in Beijing or Shenzhen now costs more than 40 times the median family annual disposable income, according to J.P. Morgan Asset Management.

Authorities have said they are worried about the property market posing risks to the financial system. Reining in the developers’ business models and limiting debt, however, is almost certain to slow investment and cause at least some downturn in the property market, which is one of the biggest drivers of China’s growth.

The real-estate and construction industries account for a large part of China’s economy. A 2020 paper by researchers

Kenneth S. Rogoff

and

Yuanchen Yang

estimated that the industries, broadly construed, accounted for 29% of China’s economic activity, far more than in many other countries. Slower growth in housing could spill into other parts of the economy, affecting consumer spending and employment.

Government statistics show about 1.6 million acres of residential floor space was under construction at the end of last year. That was equal to about 21,000 towers with the floor area of the Burj Khalifa in Dubai, the world’s tallest building.

As restrictions on borrowing imposed last year kicked in, housing construction tumbled in August to 13.6% below its pre-pandemic level, calculations by Oxford Economics show.

The revenue local governments earn by selling land to developers fell by 17.5% in August from a year earlier. Local governments, which are also heavily indebted, count on land sales for much of their revenue.

The Luwan 68 development by Fantasia Holdings Group in Shanghai. The luxury developer failed to repay $206 million of dollar bonds that matured on Oct. 4.

Photo:

Qilai Shen/Bloomberg News

A further slowdown also would risk exposing banks to more bad loans. Outstanding property loans—primarily mortgages, but also loans to developers—accounted for 27% of China’s total $28.8 trillion in bank loans at the end of June, according to Moody’s Analytics.

As pressure on housing mounts, several research houses and banks have cut China’s growth outlook. Oxford Economics on Wednesday lowered its forecast for China’s third quarter year-on-year gross domestic product growth to 3.6% from 5% previously. It trimmed its 2022 growth forecast for China to 5.4% from 5.8%.

As recently as the 1990s, most of China’s city residents lived in drab dwellings provided by state-owned employers. When market reforms started transforming the country and more people moved to cities, China needed a massive new supply of higher-quality apartments. Private developers stepped in.

Over the years, they added millions of new units in modern, well-maintained high-rises. In 2019, new homes made up more than three-quarters of home sales in China, versus less than 12% in the U.S., according to data cited by Chinese property broker

KE Holdings Inc.

in a listing prospectus last year.

In the process, the developers became much bigger than anything seen in the U.S. The largest U.S. home builder by revenue,

D.R. Horton Inc.,

reported $21.8 billion of assets at the end of June. Evergrande had some $369 billion. Its assets included vast land reserves and 345,000 unsold parking spaces.

For much of the boom, the developers were filling a need. In more recent years, policy makers and economists began to fret that much of the market was driven by speculation.

Chinese households are restricted from investing abroad, and domestic bank deposits offer low returns. Many people are wary of the country’s boom-and-bust stock markets. So some have poured money into housing, in some cases buying three or four units without any intention of living in them or renting them out.

As developers bought more locations to build on, land sales pumped up national growth statistics. Dozens of entrepreneurs who had founded development companies showed up in lists of Chinese billionaires. Ten of the 16 soccer clubs in the Chinese Super League are wholly or partly owned by developers.

Residential skyscrapers being built in Shanghai, in November 2016.

Photo:

Johannes EISELE/AFP via Getty Images

The real-estate giants have borrowed not only from banks but also from shadow-banking outfits known as trust companies and from individuals who put their savings into investments called wealth-management products. Abroad, they became a mainstay of international junk-bond markets, offering juicy yields to get deals done.

One builder,

Kaisa Group Holdings Ltd.

, defaulted on its debt in 2015, yet was able to keep borrowing and expanding afterward. Two years later it spent the equivalent of $2.1 billion to buy 25 land parcels, and in 2020 spent $7.3 billion for land. This summer, Kaisa sold $200 million of short-term bonds yielding 8.65%.

Nomura estimated that as of June, Chinese developers had racked up debts of $5.2 trillion. It said the biggest share, 46%, was in bank loans. Bond markets accounted for about 10%, including the equivalent of $217 billion of dollar bonds, many of them junk-rated.

By last year, Chinese policy makers had had enough. In August 2020, they introduced the three-red-lines rules limiting how much borrowing developers could do. Some companies with short-term obligations they couldn’t pay without new funding had to start discounting apartments to raise money.

Authorities have tried to curb demand in some places by slowing mortgage lending. They have put caps on existing-home prices in about a dozen cities to tame speculation, according to state media reports.

When old-fashioned funding sources like bank loans grew harder to access, developers became more reliant on presales of unfinished apartments. These made up 26% of the debt in Nomura’s tally.

Presales are often recorded as contract liabilities, an item that shows up on the balance sheets of sector heavyweights such as Evergrande, Country Garden, China Vanke,

Sunac China Holdings Ltd.

and

China Resources Land Ltd.

For these five combined, contract liabilities have jumped 42% in the past three years to the equivalent of $341 billion as of the end of June, FactSet data show.

Developers have also made more use of other liabilities that, like presales, don’t strictly count as debt, such as borrowing more from business partners by taking longer to pay contractors or suppliers.

The construction site of a Vanke residential building in Dalian, China, in 2019.

Photo:

Reuters

Goldman Sachs Group Inc.

analysts recently estimated Evergrande had the equivalent of $156 billion of off-balance-sheet debt and contingent liabilities, including mortgage guarantees to help home buyers get loans.

Share Your Thoughts

Can China cool developers’ borrowing binge without torpedoing the property market and hurting the economy? Join the conversation below.

The other problem for developers, and for China’s property market overall, is the way some of the trends that fueled the boom are reversing.

China’s population is aging. Its workforce has been shrinking since 2012, and official forecasts last year predicted the total population would peak in 2027.

Homeownership is already over 90% for urban households in China, among the highest in the world, according to Mr. Rogoff and Ms. Yang. They cited earlier Chinese research saying that as of late 2018, 87% of home purchases were by buyers who already had at least one dwelling.

Julian Evans-Pritchard,

an economist at Capital Economics, said his firm has looked at developers’ ability to meet their obligations from cash holdings and doesn’t think most are on the brink of default. But, citing changing demographics and reduced internal migration, he said “we’re now at a turning point where actually demand for new urban housing is going to decline over the coming decade. So they’re going to be fighting over a shrinking pie.”

Deng Lin,

a 33-year-old lawyer in Shanghai, planned to sell two properties she owns to buy a bigger one after she gave birth to twins this summer. The government’s clampdown on debt risks derailing her plan of upgrading to a three-bedroom, which she estimates could cost up to $1.86 million.

Tightened mortgage rules means she would have to pay 80% upfront. Banks have been slow to approve her loan application.

“There’s simply too much uncertainty in the market,” she said.

—Anniek Bao contributed to this article.

Write to Quentin Webb at quentin.webb@wsj.com and Stella Yifan Xie at stella.xie@wsj.com

As the clock ticked down on the debt-ceiling standoff in Washington, Wall Street firms parked a record $1.605 trillion of cash overnight in the Federal Reserve’s popular reverse repo program.

Congress Thursday afternoon approved a temporary funding measure to extend government spending through Dec. 3, while averting a partial shutdown hours before a midnight deadline, but the federal debt ceiling has yet to be lifted.

See: What happens if the U.S. defaults on its debt?

As the drama played out on Capitol Hill, a total of 92 firms took part in the Fed’s Thursday reverse repo operation. The program, run out of the Federal Reserve Bank of New York, allows banks, government sponsored enterprises and some of the world’s largest investment firms a short-term haven to park cash, while earning 5 basis points overnight.

Earlier in September, the Fed doubled the cap each counterparty can pledge to the overnight facility to $160 billion each. The program has grown in popularity in recent months as trillions worth of fiscal and monetary stimulus course through the U.S. economy and financial markets.

The latest uptick in demand was not unexpected, however, with some Wall Street analysts forecasting in early August the surge, due to the shrinking Treasury-bill market, the typically volatile year-end period and rancor in Washington over government spending.

U.S. stocks sold off sharply Thursday, the last day of September and the quarter, with the Dow Jones Industrial Average

DJIA,

-1.59%

shedding 456 points, or 1.6%, while booking its worst monthly loss since October 2020.