Realtors, mortgage brokers, and appraisers across the US are bracing for widespread job cuts as home sales plummet amid rising interest rates.

For those who work in and around the housing market, the effect of aggressive moves by the Federal Reserve to reduce inflation has been swift and severe.

“It went from feast to famine, from everybody buying to turtle slow,” said Linda McCoy, board president of the National Association of Mortgage Brokers.

Realtors, mortgage brokers, appraisers, and construction groups say they have lost as much as 80 per cent of their revenue since the Fed started raising rates in March. Rates for a 30-year fixed mortgage — at 6.66 per cent — have nearly doubled since and are now at their highest level since 2008.

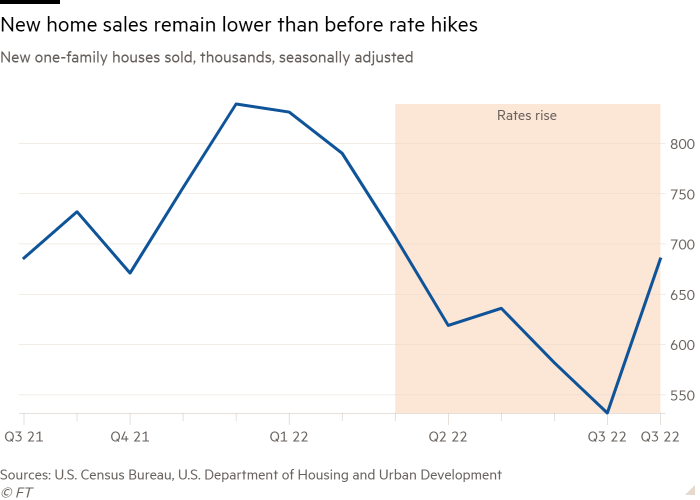

Home sales quickly plunged as higher borrowing costs and recession fears discouraged buyers. Nearly 20 per cent fewer homes were sold this August than during the same month last year, according to the National Association of Realtors. For realtors and mortgage brokers, who mostly work on commission, the changing market has decimated their livelihoods and pushed others out of the field altogether.

“There’s going to be a major shakeout,” said Ken Johnson, a real estate economist at Florida Atlantic University who is also a former broker. “There are roughly 1.5mn realtors, but that number will be down 20 per cent within 24 months. And those aren’t the only members of the real estate industry that are very dependent on the volume of transactions. There are these tertiary jobs like the appraisers, the mortgage lenders, all the way down to termite inspectors.”

Mortgage lenders were among the first to eliminate staff. In April, Wells Fargo, which originates more mortgages than any other US bank, laid off nearly 200 loan processors and their managers, blaming “cyclical changes in the broader home-lending environment”. USAA, Citigroup and JPMorgan Chase later announced cuts to their own home lending workforces.

Other independent lenders, including Sprout Mortgage and First Guaranty Mortgage Corp, have gone out of business.

Some brokers did almost a third of their business refinancing existing mortgages as rates hovered near record lows in recent years, but applications for refinancing fell 80 per cent over the past year, according to the Mortgage Bankers Association. New mortgage applications dropped 29 per cent in the same period.

“The way these rates have risen so fast is almost catastrophic to the industry,” McCoy said.

A record 1.5mn Americans worked as real estate agents during the height of the market last year. Getting a real estate licence is easier than entering other industries with high earning potential, requiring only a high school diploma and three to six months of training leading up to an exam. Thousands of new workers rushed in as home prices accelerated during the Covid pandemic, hoping to take advantage of flexible working hours and sky-high profits. Some 156,000 people joined the National Association of Realtors in 2020 and 2021 alone. That is 60 per cent more than in the two years before.

“That growth was much stronger than the home sales opportunities that were available,” said Lawrence Yun, the chief economist for the National Association of Realtors. “The reality is that not everyone’s going to survive.”

In June, Redfin and Compass laid off hundreds of employees. Redfin chief executive Glenn Kelman told staff that he feared “years, not months, of fewer home sales”. Compass said its lay-offs were “due to the clear signals of slowing economic growth”, before eliminating more jobs last month.

Though lay-off rates tracked by the labour department showed that the number of real estate workers whose jobs were eliminated are little changed at 16,000 in August, Johnson said that most agents work as independent contractors and are not counted in jobs data. Many will pivot their business models or take on second jobs to supplement their income, he predicted.

Shane Skelly, a real estate agent and home flipper in San Diego, “froze” his business’s house flipping arm in June as potential buyers disappeared. His company, Left Coast Realtors, is now focusing on facilitating renovations for past clients.

“It wasn’t extreme to begin with, over the last couple of months it’s really accelerated,” Skelly said. “It’s a little bit more significant of a correction than I thought it was going to be.”

Mike Pappas, the chief executive of Florida-based brokerage The Keyes Company, said he is considering scaling back overhead costs on offices and marketing in the hopes of avoiding having to lay off any of his firm’s 3,300 agents.

“We have to respond dramatically to adjust to the new normal,” Pappas said.

But for many, falling home sales could push them out of business entirely, said Johnson at Florida Atlantic University.

“Most that are in business today have never sold in a 7 per cent 30-year mortgage rate environment,” he said. “That mortgage rate got too high and I think a lot of people are looking around saying: ‘you know, what’s next?’”